Responsible Investment in the Nordics: What Comes After ESG Leadership?

•

5 mins read

The Nordics have long been global leaders in responsible investment. Nordic banks, pension funds, and asset managers were among the first to integrate ESG considerations into portfolio management and stewardship practices.

But the landscape is changing. Investors now face new types of risks that go beyond traditional ESG frameworks, including geopolitical tensions, supply chain controversies, and fast-moving reputational crises. At the same time, new technologies such as artificial intelligence are transforming how investors detect and interpret these signals.

Watch this replay to hear Magnus Billings, SESAMm Advisor, and Sylvain Forté, SESAMm CEO, explore how Nordic investors are adapting their responsible investment strategies and what the next decade of risk monitoring may look like.

May 2, 2022. The S&P 500 ousts Tesla, Inc. from the S&P 500 ESG Index. Tesla is widely recognized as the firm that ushered electric vehicle making into the mainstream. So the index’s move seems unreasonable or possibly made in error to many, raising some interesting questions:

How does an environmentally-friendly corporation like Tesla get dropped from an ESG index?

Why does a potentially non-environment-friendly company like Exxon make the ESG index and remain on it?

What do these moves mean about the integrity and validity of ESG scores and ratings?

Global industry group peers pushed Tesla’s S&P DJI ESG Score further down the ranks in the GICS industry group: Automobiles & Components.

A decline in criteria level scores related to Tesla’s low carbon strategy and codes of business conduct contributed to its 2021 S&P DJI ESG Score.

A media and stakeholder analysis identified "two separate events centered around claims of racial discrimination and poor working conditions at Tesla’s Fremont factory."

The analysis also highlights "the handling of the NHTSA investigation after multiple deaths and injuries were linked to its autopilot vehicles, affecting the company’s S&P DJI ESG Score at the criteria level, and its overall score."

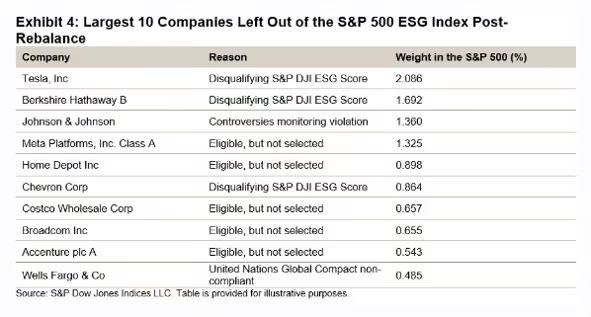

Companies, including Tesla, left out of the S&P 500 ESG Index post-rebalance. Image courtesy of Indexology Blog.

The S&P blog post summarizes their case about dropping Tesla, "While Tesla may be playing its part in taking fuel-powered cars off the road, it has fallen behind its peers when examined through a wider ESG lens." And in this statement lies the crux of why the index dropped Tesla and why others are still on.

Analyzing Tesla’s web data

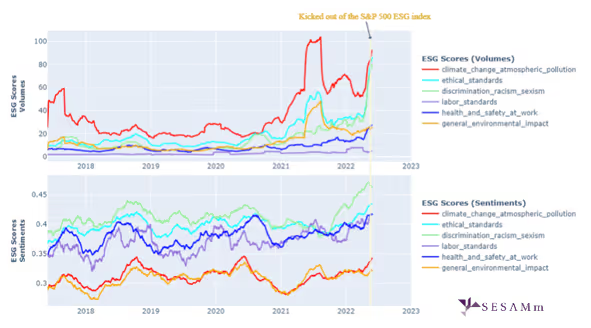

SESAMm’s TextReveal® insights suggest that the S&P 500’s decision to remove Tesla could be justified based on increasing controversy levels concerning discrimination, ethical standards, and work health and safety. By analyzing text related to ESG topics across the web, we picked up trends for the following subtopics:

climate_change_atmospheric_pollution

ethical_standards

discrimination_racism_sexism

labor_standards

health_and_safety_at_work

general_environmental_impact

Tesla’s ESG scores (six subtopics)

Figure 1: Tesla ESG scores for volumes and sentiments (1-year moving average), all source types.

Regarding the volume features (Figure 1), we observed a significant increase in the scores related to ethical standards, discrimination, and atmospheric pollution for Tesla before the controversy. The conclusions are mostly the same for ESG sentiment (negative) scores. An interesting note is that the negative score of health and safety at work slightly increased in the months before the removal of Tesla from the index.

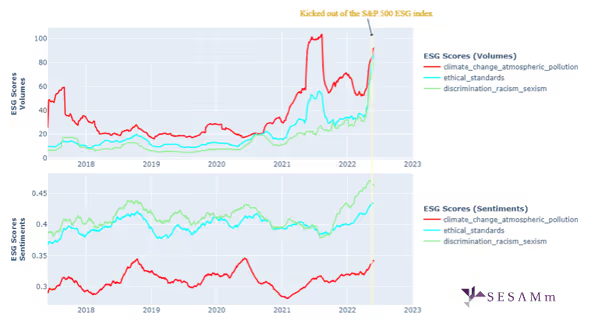

Figure 2: Tesla ESG scores for volumes and sentiments (1-year moving average), all source types, select subtopics.

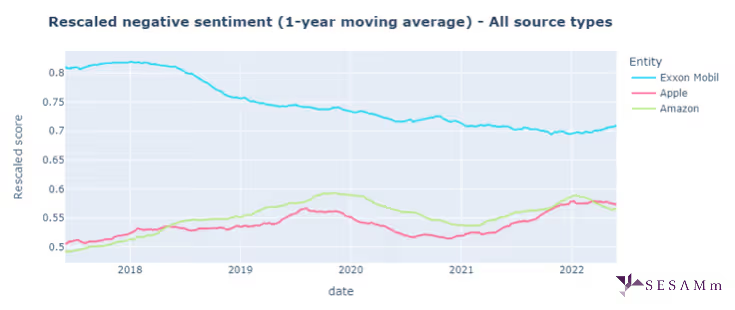

Comparing Tesla’s sentiment with other S&P 500 ESG Index companies

To see how Tesla’s ESG sentiment scores compared with other companies, we must rescale them with respect to a large universe of companies. This process means that for a given company, we use percentiles of the distribution of each subtopic’s ESG score to do a rescaling to the S&P 500 ESG constituents list after the 2022 rebalancing. Rescaling allows us to compare the companies with each other because the rescaled score indicates how bad the company is compared to the others, according to a specific ESG subtopic.

The following graphs show different sets of subtopics, plotting the mean of the respective rescaled scores if several topics are considered. Here are the companies considered.

Companies removed from the index:

Tesla

Delta Air Lines

Chevron Corporation

Companies that joined the index after the 2022 rebalancing:

American International Group

Expedia Group

Companies still part of the index:

Exxon Mobil

Apple

Amazon

Tesla, Delta, Chevron, AIG, and Expedia compared

Figure 3: Six-subtopic rescaled scores for Tesla, Delta, Chevron, AIG, and Expedia.

Apple, Amazon, and Exxon compared

Figure 4: Six-subtopic rescaled scores for Apple, Amazon, and Exxon.

The S&P 500’s choice is reasonable

Our analysis shows that the S&P 500’s decision to oust Tesla from the ESG index is reasonable. We found significant subtopic volumes and negative sentiment that support the S&P 500’s claims of racial discrimination, poor working conditions, and other controversies.

Thanks for reading this quick analysis. For a more detailed report, including Chevron’s and Delta’s ESG scores, reach out to a representative today.

SESAMm’s ready-to-use alternative data

Leverage our alternative data streams to incorporate systematic insights into your alpha signals or risk monitoring your entire portfolio. From tracking global sentiment to analyzing retail communities like WallStreetBets and integrating ESG alternative data into your systems, our solutions will make generating value from web insights easy.

In a significant policy reversal, Britain has officially abandoned its plans to develop a "taxonomy" for green investments, marking a notable shift in the country's approach to sustainable finance regulation. The decision, announced by the UK Treasury on July 15, 2025, signals growing concerns about the practical implementation of ESG frameworks and reflects broader challenges in sustainable finance regulation.

The Abandoned Framework

The UK's green taxonomy, first proposed in 2020, was designed to provide clear definitions of environmentally sustainable economic activities. Similar to the EU's taxonomy, it aimed to create standardized criteria to help investors identify genuine green investments and combat greenwashing. However, after extensive consultation, the Treasury concluded that the taxonomy "would not be the most effective tool to deliver the green transition."

Following a comprehensive review process, HM Treasury determined that alternative approaches would be more suitable for advancing the UK's green finance objectives. The decision represents a departure from the EU model and highlights the ongoing challenges in developing effective sustainability frameworks.

Market Implications

The abandonment of the taxonomy creates immediate challenges for investors and financial institutions operating in the UK. Without standardized official definitions, financial institutions must navigate a more complex landscape of varying private sector standards and frameworks.

For asset managers, the absence of official guidance means continued reliance on existing voluntary standards and third-party frameworks. This fragmentation could complicate investment decision-making, particularly for institutions operating across multiple jurisdictions with different regulatory requirements.

The decision may also impact the UK's position in global sustainable finance markets, where standardized taxonomies are increasingly seen as important tools for directing capital toward environmentally beneficial activities.

Industry Response

The decision has generated significant discussion within the financial sector. The UK Sustainable Investment and Finance Association (UKSIF) expressed disappointment with the announcement. Oscar Warwick Thompson, Head of Policy and Regulatory Affairs at UKSIF, called for "swift delivery of commitments on transition plans and sustainability reporting standards" as alternative measures to support the green transition.

Industry stakeholders have emphasized the need for clarity on what alternative approaches the government will pursue to support sustainable investment and address greenwashing concerns in the absence of the taxonomy.

Regulatory Context

The UK's decision reflects broader challenges facing regulators worldwide in developing effective sustainability frameworks. Creating standardized criteria that can effectively span multiple economic sectors while remaining practical for implementation has proven complex across various jurisdictions.

Key implementation challenges that have influenced regulatory approaches include:

Compliance costs and administrative burden for businesses

The technical complexity of standardizing criteria across diverse economic activities

Ensuring frameworks drive meaningful environmental outcomes rather than just compliance

Balancing comprehensiveness with practical usability

Future Direction

While stepping back from the taxonomy approach, the UK government has indicated its continued commitment to supporting sustainable finance through alternative mechanisms. The Treasury has suggested that other policy tools may be more effective in driving the green transition, though specific details of these alternative approaches have not yet been fully outlined.

For companies and investors, this development underscores the importance of developing robust internal ESG assessment capabilities and maintaining familiarity with multiple sustainability frameworks. It also highlights the continued role of market-led initiatives and private sector standards in establishing credible sustainability criteria.

The decision may prompt other jurisdictions to reassess their own approaches to sustainable finance regulation, particularly as questions about the effectiveness and implementation of various frameworks continue to evolve.

As the sustainable finance landscape continues to develop, finding the optimal balance between regulatory guidance and market flexibility remains an ongoing challenge for policymakers and financial sector participants worldwide.

SESAMm’s AI Technology Reveals ESG Insights

Discover unparalleled insights into ESG controversies, risks, and opportunities across industries. Learn more about how SESAMm can help you analyze millions of private and public companies using AI-powered text analysis tools.

The private markets secondaries space has entered a new chapter. What was once a niche corner of alternative investments, used primarily by limited partners (LPs) seeking early exits from fund commitments, has grown into one of the most dynamic segments of global private capital. The market has tripled in size since 2019 and grown by approximately 50% between 2024 and 2025 alone, reaching an estimated $230 billion in annual transaction volume and now representing around 5% of all global private equity assets under management.

This piece examines the forces behind that expansion, the structural shifts redefining the market, and the operational and regulatory challenges participants will need to navigate as the asset class continues to scale.

Market Growth and Shifting Deal Dynamics

Several converging factors have driven the secondaries market to its current size. A prolonged slowdown in IPO activity and traditional exits has created a liquidity bottleneck across private markets, leaving many LPs over-allocated to alternatives and constrained in their ability to make new commitments. The secondary market has become a primary mechanism for these investors to rebalance portfolios and free up capital.

Deal structuring has grown more sophisticated in step with market volumes. Ropes & Gray has observed a continued expansion in the use of purchase price deferrals and earnouts, and more recently, the introduction of deal-specific funding caps, limits on how much capital a buyer can be called to deploy before a specified date. These mechanisms allow sellers to achieve higher reference-date pricing while enabling buyers to manage capital deployment pacing and portfolio composition. In Q1 2026 alone, institutions initiated new secondary sales processes totaling north of $20 billion, some linked to denominator effect concerns as declines in public market portfolios pushed private allocations above target levels. Whether this proves a sustained driver of supply will depend on how institutional portfolios weather current market conditions.

The Three Transaction Types

Secondary transactions fall into three main categories:

LP-led transactions, the original form, involve an LP selling existing fund interests, sometimes across a broad portfolio of hundreds of positions, typically through competitive auction processes with tight timelines.

GP-led continuation funds, the fastest-growing segment, involve a sponsor transferring select assets into a new vehicle, giving existing LPs the option to cash out or roll forward. As of 2025, GP-led and LP-led volumes are roughly evenly split at around $115 billion each. GP-led buyout fund volume grew 39% year-over-year, while private credit secondaries saw nearly 300% year-over-year growth in GP-led activity.

The third category, structured solutions, provides capital to a GP collateralized by existing fund assets and can take a wide variety of bespoke forms.

What Are the Operational and ESG Challenges in the Market?

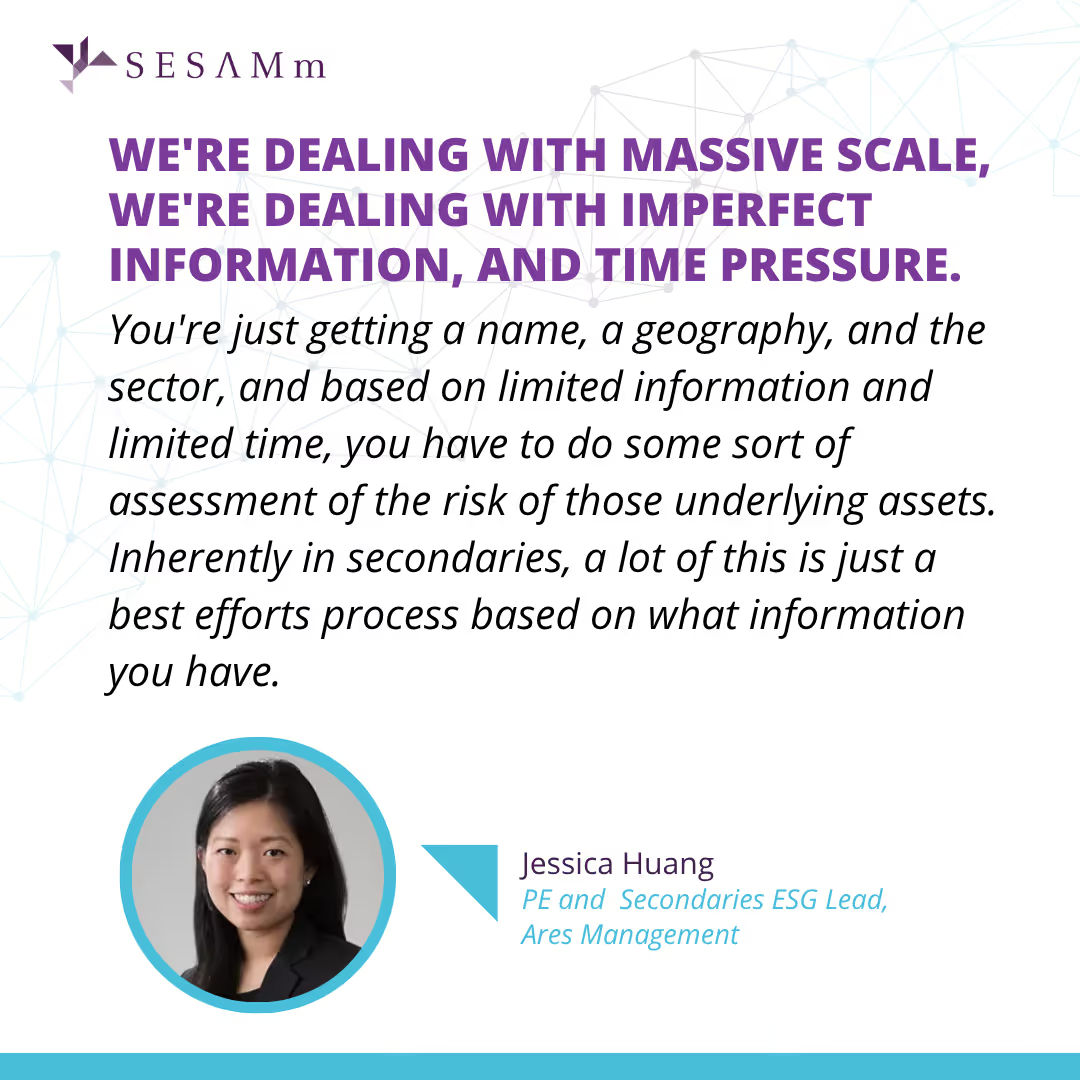

One of the defining challenges in secondaries is the speed and scale of due diligence required, particularly in LP-led transactions. Buyers may need to evaluate hundreds, or in private credit secondaries, over a thousand, underlying positions with limited information and within windows of 24 to 48 hours. As Jessica Huang, Managing Director and ESG lead for private equity and secondaries at Ares Management, noted in a recent webinar:

Against this backdrop, LP expectations around ESG integration have risen sharply. LPs are now holding secondaries to a standard closer to that applied to direct investments, with requests for Article 8-classified funds, look-through exclusion lists, and UN Global Compact compliance screening becoming more common. Main exclusion categories include fossil fuels, controversial weapons, tobacco, and gambling, though definitions and revenue thresholds vary significantly across mandates. SFDR 2.0, currently in draft form, may introduce additional mandatory exclusion categories that managers are monitoring closely. In LP-led deals where buyers are inheriting a broad portfolio of assets, highly granular opt-outs can mean missing certain large transactions, a trade-off that must be clearly communicated to LPs.

The Role of Technology and AI

Technology has become central to the scaling of secondaries operations. AI tools are now applied across controversy screening, ESG data analysis, and emissions estimation, where direct disclosures are unavailable. A particular challenge in the asset class is coverage: many underlying companies are small or mid-market private businesses not captured in conventional databases.

Market participants consistently emphasize that AI outputs serve as inputs to human judgment, not as replacements for it. At Ares, screening results are reviewed by ESG specialists before being passed to deal teams for final decisions.

What the Future Holds

Transaction volumes are forecast to continue rising as both the seller and buyer universes expand. Private credit, infrastructure, and structured secondaries all represent areas of growing specialization and regional expansion, particularly in Asia, where secondary activity has been limited but is expected to grow as investment programs mature, broadening the market further. Capital supply dynamics bear watching: while dry powder remains substantial, deal volume growth has outpaced fundraising since 2023, which could create pricing or capital constraints. The entry of retail investors through evergreen vehicles adds a meaningful new source of capital but brings different liquidity expectations and regulatory considerations.

On the operational side, the sophistication of deal terms, the complexity of ESG compliance, and the volume of data processed per transaction are all increasing. Firms that can integrate technology into their diligence and monitoring workflows, while preserving the human judgment layer, will be best positioned to manage market growth. Secondaries are no longer a supplementary liquidity tool; they have become a structural feature of how private markets operate.

Stay ahead with the latest in ESG and AI intelligence

Join our mailing list to receive new reports, event invites, and updates from SESAMm directly to your inbox.

.png)