A single number is a powerful thing. It can summarise months of reporting across dozens of sources into something a risk team can act on in seconds. It can also hide more than it reveals, if no one explains how it was built. When the same company receives very different ESG scores from different providers, the usual reason is not bad data. It is undisclosed method.

SESAMm has published the full methodology behind its Controversy Exposure Score, free to access, following the entry into force of the EU ESG Rating Regulation on 2 July 2026. This article walks through what the score measures, how it is constructed, and the two design choices that most distinguish it.

What the Score Measures

The Controversy Exposure Score, or CES, runs on an absolute scale from 0 to 100 and is grouped into five risk bands, from Very Low to Very High. It has a single, deliberately narrow objective: to measure an entity's exposure to ESG controversies, meaning adverse events and conduct attributed to that entity as reported in public sources.

Three points define its scope from the outset. The CES is an impact-materiality measure. It looks at the negative footprint of an entity's activities on people and the environment, not the financial effect of ESG issues on the company itself. It is backward-looking. It reflects controversies that have already been reported, over a rolling 24-month window, rather than forecasts or transition pathways. And it is built only from public and licensed public-domain information, never from private, confidential or self-reported data.

From Millions of Articles to a Single Case

Before any score can exist, raw coverage has to become structured information. This is where most of the engineering sits.

SESAMm's pipeline first attributes each document to the right entity and screens it for genuine ESG relevance against a multilingual taxonomy, removing low-quality, duplicate or non-editorial content. It then addresses a problem familiar to anyone who monitors the news: media echo. A single real-world incident can generate dozens of near-identical articles. To prevent that from inflating the picture, related documents are grouped into Events, and related Events into Cases, so that a controversy unfolding over time is tracked as one continuous case rather than many separate items.

A validation step then confirms that each candidate event is a genuine ESG controversy concerning the entity, acting as a control against false positives before anything enters the score. Only after this sequence does scoring begin.

Design Choice One: Severity Before Volume

The most important question about any controversy is not how many articles it generated. It is how serious it is. SESAMm assesses severity first, through a feature called Event Intensity, scored on a 1 to 5 scale.

Severity is judged on two axes. The first is reversibility, the permanence of the harm, from a procedural or technical breach at the low end to irreversible damage such as fatalities or permanent ecosystem destruction at the high end. The second is reach, the scale of the impact, from an effect confined to a single facility up to systemic or national-level harm.

Two principles govern how these combine, drawn from the UN Guiding Principles approach to identifying severe impacts. Permanence takes priority over breadth, so an irreversible harm weighs more than a widespread but remediable one. And grave, irreversible events are designed not to slip into low-severity tiers simply because their reach was limited, so that isolated but serious events stay visible. The structured severity is then adjusted for the entity's actual responsibility, from direct involvement through its own operations to indirect involvement through its value chain.

Media coverage does play a role, but a disciplined one. The level of coverage contributes to the score as a signal of salience, and it is rebased against each entity's own historical media baseline rather than counted in absolute terms. This stops high-profile companies from looking riskier simply because they attract more press, and it keeps the engine sensitive to genuine spikes at less-covered entities.

Design Choice Two: Worst-Of, Not Average

The second defining choice is how the pillars combine. Most ESG scores apply percentage weights to Environmental, Social and Governance factors and blend them into a weighted average. SESAMm deliberately does not.

The reason is a structural flaw the company calls dilution bias, or data masking. When pillars are averaged, strong administrative compliance in one area can mathematically conceal a catastrophic breach in another. A company with excellent governance disclosures could see a severe environmental controversy diluted into a comfortable middle score.

Instead, the CES uses a rule-based maximum-severity, or worst-of, logic. The entity's most serious controversy drives the score, regardless of which pillar it sits in, and it cannot be watered down by stable metrics or an absence of alerts elsewhere. The five bands that result are fixed in absolute terms rather than calculated relative to a peer group, so a company's score is not flattered or punished by the behaviour of its sector. A score above 80 reflects critical, often irreversible breaches. A score of 20 or below reflects negligible or minor isolated issues.

A Number You Can Interrogate

Taken together, these choices produce a score with a clear logic behind every point on the scale. Severity is assessed before volume. The gravest event leads. Coverage is normalised so it informs rather than distorts. And the bands mean the same thing for every entity, in every sector, anywhere in the world.

None of this requires a user to take the result on faith. The objective, the taxonomy of 44 sub-risks, the severity model, the aggregation rule and the interpretation of each band are all set out in the public methodology. A score is only as useful as the method that produced it, and that method is now open to read.

To see exactly how the Controversy Exposure Score is constructed, visit sesamm.com/methodology.

A familiar debate has followed ESG data for years. One camp argues that the field generates too much information for any human team to handle, so the work should be left to machines. The other argues that ESG judgments are too consequential to automate, so humans should review everything. Both positions contain a real concern. Neither describes how a credible rating is actually produced.

With the publication of its full Controversy Exposure Score methodology, now public and free to access following the entry into force of the EU ESG Rating Regulation on 2 July 2026, SESAMm is making the answer explicit. A trustworthy rating is not a choice between artificial intelligence and human expertise. It is the disciplined combination of the two, with each doing the part of the work it does best.

The Scale Problem Is Real

Teams that monitor ESG controversies rarely suffer from too little information. They suffer from too much. A single incident can generate dozens of articles within days, in multiple languages, across outlets of very different quality. Multiply that by a global investment universe and the volume becomes impossible to track by hand.

This is the part of the problem that machines are built for. SESAMm's pipeline ingests more than 10 million documents a day, drawn from an input layer of over 30 billion documents that includes licensed global news, public web and media feeds, NGO publications, and public regulatory and judicial filings. It screens controversies for millions of public and private companies, alongside infrastructure projects, state-owned entities and sovereigns. No analyst team could read at that scale, and none should try. Asking people to do machine work is how important signals get missed.

So artificial intelligence carries the load. Natural language processing and machine learning models, including large language models, attribute documents to the right entity, filter for genuine ESG relevance, and group related articles into discrete events and events into continuous cases. This is what allows a controversy that unfolds over weeks to be tracked as one developing story rather than a hundred disconnected headlines.

Why Scale Alone Is Not Trust

A system that reads everything will also, inevitably, misread some of it. SESAMm is direct about this in its methodology, because pretending otherwise would be the opposite of transparency.

Probabilistic language models can misinterpret a historical or hypothetical reference as an active controversy. Automated clustering can occasionally merge two distinct incidents or split one prolonged crisis into fragments. Model accuracy varies across languages, and lower-resource languages or heavily idiomatic content raise the risk of misclassification. These are structural properties of statistical systems, not bugs to be wished away.

This is precisely where scale stops being enough and human expertise becomes indispensable. A number that informs how capital is allocated cannot rest on automation alone.

Where Human Judgment Enters

SESAMm operates a dual-layer human quality-assurance process, and it runs every day.

At the first layer, a dedicated Research and Analytics quality-assurance team reviews data accuracy, both reactively, when a question is raised about a case, a score or a classification, and proactively, by reviewing generated alerts. Where an issue is confirmed, the correction, whether a reattributed entity, a corrected sub-risk tag or the removal of an irrelevant event, is applied at the source, logged, and the affected scores are recomputed on the standard daily cycle.

At the second layer, complex cases and recurring structural issues are escalated to the Methodology Lead, who can update the underlying training corpus so that a category of error becomes less likely in future. This is the detail that matters most. Human review is not a final rubber stamp on top of the machine. It is a feedback loop that teaches the system, so that today's corrections improve tomorrow's automated output.

The same expertise sits at the front of the process, not only the end. Analysts define the 44 ESG sub-risks, design how severity is assessed, and fine-tune the models. The methodology is a human construction that machines then apply consistently at scale.

A Division of Labor, Not a Contest

Seen this way, the old debate dissolves. The question was never whether AI or people should produce ESG ratings. The question is which part of the work belongs to which.

Machines provide reach, consistency and speed. They apply the same rules to every entity, every day, without fatigue or favor.

People provide judgment, correction and improvement. They decide what the system should look for, they catch what it gets wrong, and they raise the standard of the model over time.

The result is a rating that is both broad enough to cover the real world and rigorous enough to be relied upon. Scale without rigor is noise. Rigor without scale never reaches most of the companies an investor actually holds. The value is in the combination.

What This Means Going Forward

The EU ESG Rating Regulation asks providers to disclose how their ratings are built. SESAMm has chosen to disclose the full pipeline, including the role of AI, the points where it can fail, and the human controls that contain it. The aim is not to claim the technology is flawless. It is to show, in detail, why the output can be trusted anyway.

As artificial intelligence becomes more capable, the temptation to remove the human layer will grow. SESAMm's position is the opposite. The more powerful the models become, the more valuable the people who direct them, check them and teach them become. That is the architecture of a rating worth trusting, and it is now open for anyone to read.

To explore the full methodology behind the Controversy Exposure Score, visit sesamm.com/methodology.

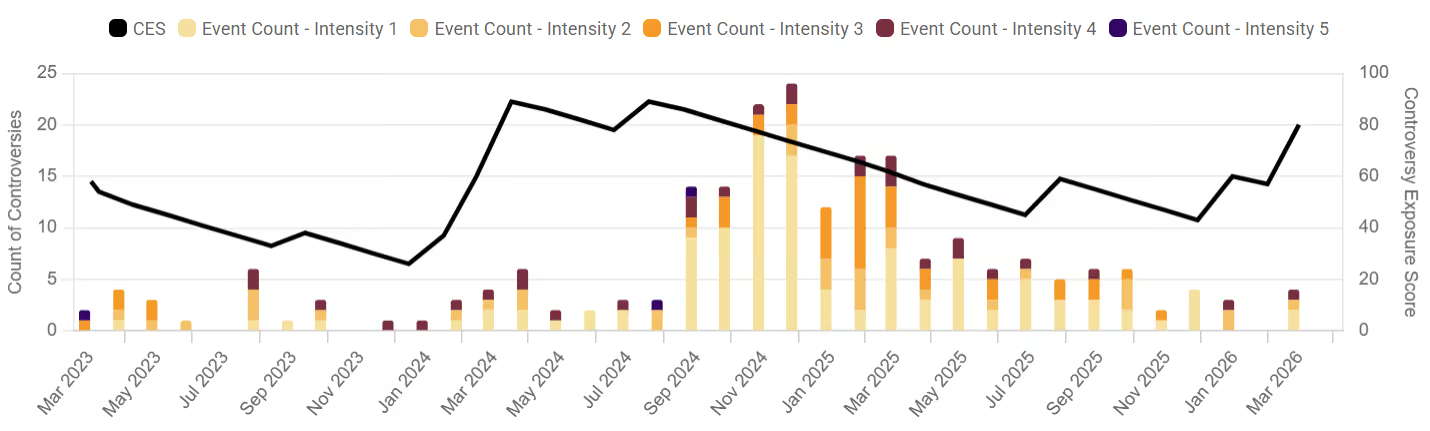

SESAMm's ESG data shows FIFA's Controversy Exposure Score has stayed High to Very High since 2020. See why continuous monitoring beats the four-year cycle.

With the 2026 World Cup now underway, FIFA is back in the global spotlight, and its risk profile is once again being narrated in four-year cycles, as though controversy arrives with the tournament and recedes with the closing ceremony. The data points to a different pattern. Across the period from January 2020 to June 2026, the large majority of FIFA's most serious controversies were recorded outside any World Cup window. Tournaments concentrate global attention on FIFA's existing liabilities, but the evidence suggests they do not drive the underlying volume. Many of the substantive events, including court verdicts, regulator rulings, fund decisions, and bid matters, occur in the periods between tournaments.

For investors, sponsors, and anyone screening exposure to football's governing body, this distinction matters. If controversy were cyclical, it could be assessed around the calendar. Because the data indicates it is closer to continuous, it is better suited to ongoing monitoring. To examine this, the analysis below draws on SESAMm's controversy data, which captures and classifies FIFA's reputational, regulatory, and operational controversies.

Context: How FIFA's Structure Shapes Its Risk

Controversy Exposure Over Time

*Unsolicited ratings - produced from public sources, not commissioned by the rated company. For more information, visit here.

It helps to start with how FIFA is organized, because its governance structure has a direct bearing on the type of risk it carries. As a Swiss-law association, FIFA answers to a membership rather than to shareholders or a securities regulator, and its decision-making body, the FIFA Council, is composed of representatives from the regional confederations whose commercial interests the Council also oversees. This means the regulatory functions of sanctioning, eligibility, and integrity sit close to the commercial function of awarding and selling tournaments. Arrangements of this kind tend to produce a steady stream of governance-related questions as part of normal operations, which is consistent with SESAMm’s controversy data.

One useful illustration is procedural rather than criminal. The Blatter and Platini proceedings span the entire time period without reaching a clear resolution, running from a 2020 complaint through a fraud indictment, an acquittal, a prosecutorial appeal, and a second acquittal, before Platini opened a fresh action against FIFA and Infantino in June 2026. As a corruption narrative, the sequence is inconclusive. As a governance observation, it illustrates a broader dynamic in which matters are litigated and re-litigated over long periods, in part because resolution often depends on external courts operating on their own timelines. The result is a long-running procedural footprint rather than discrete, time-bound events.

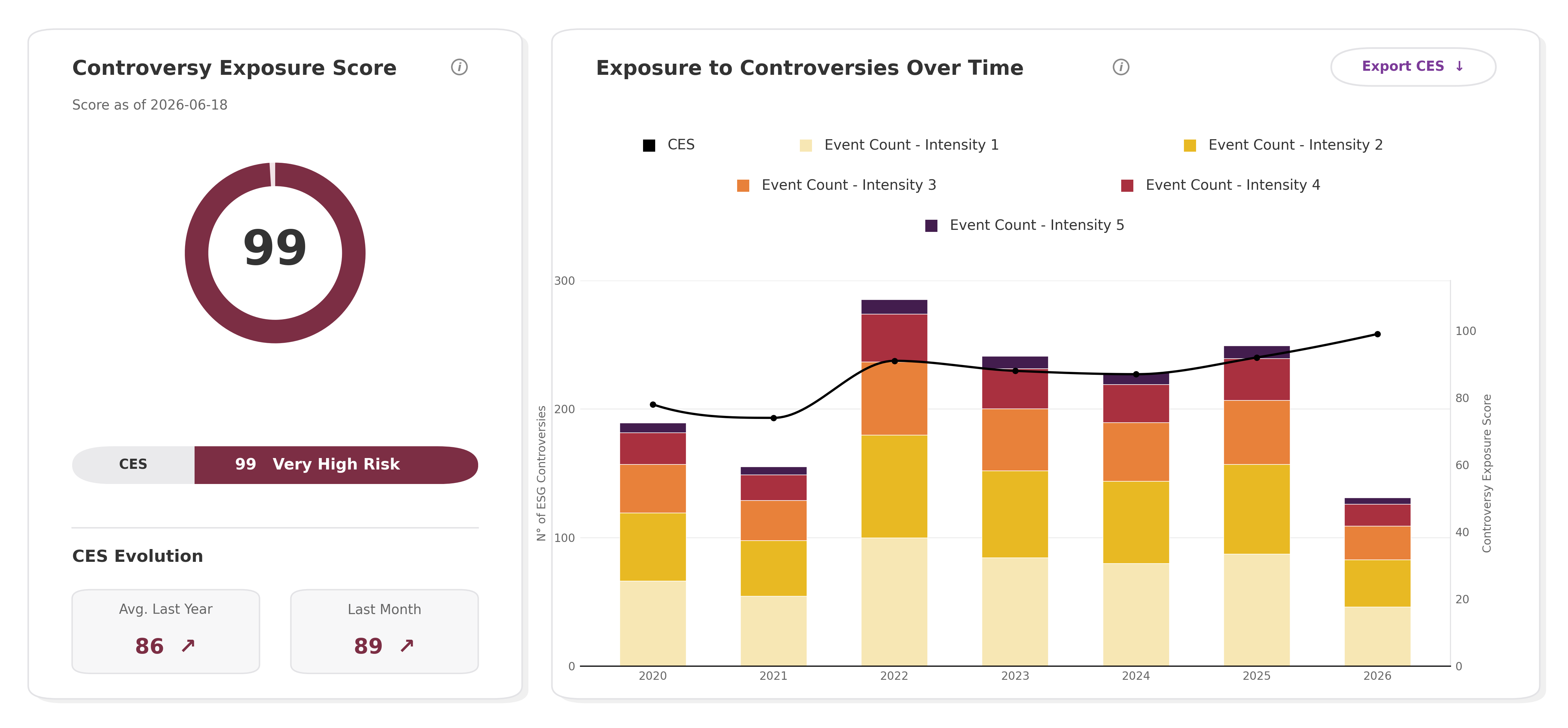

The CES is an aggregate, entity-level score (0–100) that measures an entity's overall exposure to ESG controversies over time. It's built from individual ESG events and their intensities, synthesizing both event volume and severity into a single trackable figure. The intensity score, by contrast, operates one level down: it's applied at the event level, measuring how severe or important each individual ESG event is on a scale from 1 (least severe) to 5 (most severe). In short, the CES tells you how exposed an entity is overall, while the intensity score tells you how serious each underlying event is.

ESG Risk Over Time

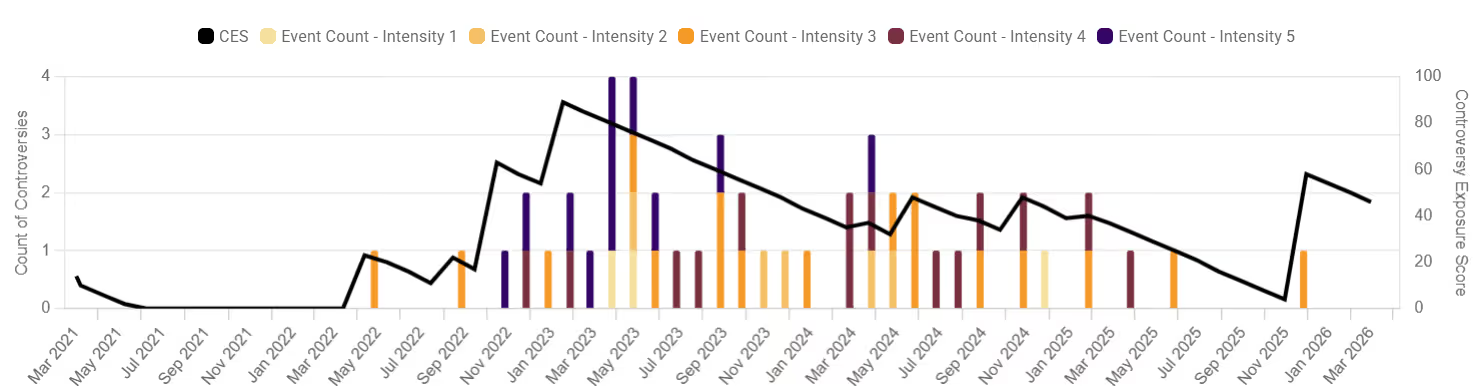

This chart tracks FIFA's ESG controversies per year from 2020 to 2026, stacked by risk pillar. Governance dominates every bar, with social forming a secondary band and environmental barely visible. Volume climbs from a governance-heavy opening year to a clear peak in 2022, then holds at a stable plateau through 2025 before the short 2026 bar. The shape is driven by a handful of major events. The 2020 corruption investigations kept the opening-year baseline elevated and were almost purely governance-related, following a US DOJ indictment unsealed that April, which alleged bribes were paid for the votes that awarded Russia and Qatar the 2018 and 2022 World Cups.

The 2022 Qatar World Cup marked the clear inflection point, drawing sportswashing accusations and pushing total controversies to their peak, while migrant-worker conditions and human-rights coverage around Qatar thickened the social band into a permanent quarter-to-third of each bar from 2022 onward. Rather than reverting, controversies settled into a post-2022 "new normal," plateauing well above the pre-tournament level.

Underneath it all, corruption-and-bribery and legal/investigative exposure account for the bulk of total risk across 2020 to 2026, while environmental risk stays statistically negligible throughout.

ESG Risk by Type

Environmental Risks

Environmental risk accounts for a small share of FIFA's total controversy volume, but that low frequency masks cases of genuine severity. The Swiss Fairness Commission ruled against FIFA's Qatar 2022 carbon-neutrality marketing, turning a greenwashing accusation into a formal regulatory matter still active in June 2026. Related controversies extend the theme, including criticism of the Saudi Aramco and Coca-Cola sponsorships, the cooling and water-use controversies at Qatar, and the animal-welfare outcry over stray-dog culling ahead of Morocco's 2030 hosting.

Beyond these, FIFA has drawn criticism over its marketing and communications, notably branding the 2022 Qatar World Cup as "carbon neutral," and has dealt with fraud and embezzlement, exemplified by the case of former FIFA and CONCACAF official Chuck Blazer. Issues tied to its board and senior management leadership round out the picture, though the overall pattern is one of an organization reacting to the weight of its legal and ethical past rather than getting ahead of it.

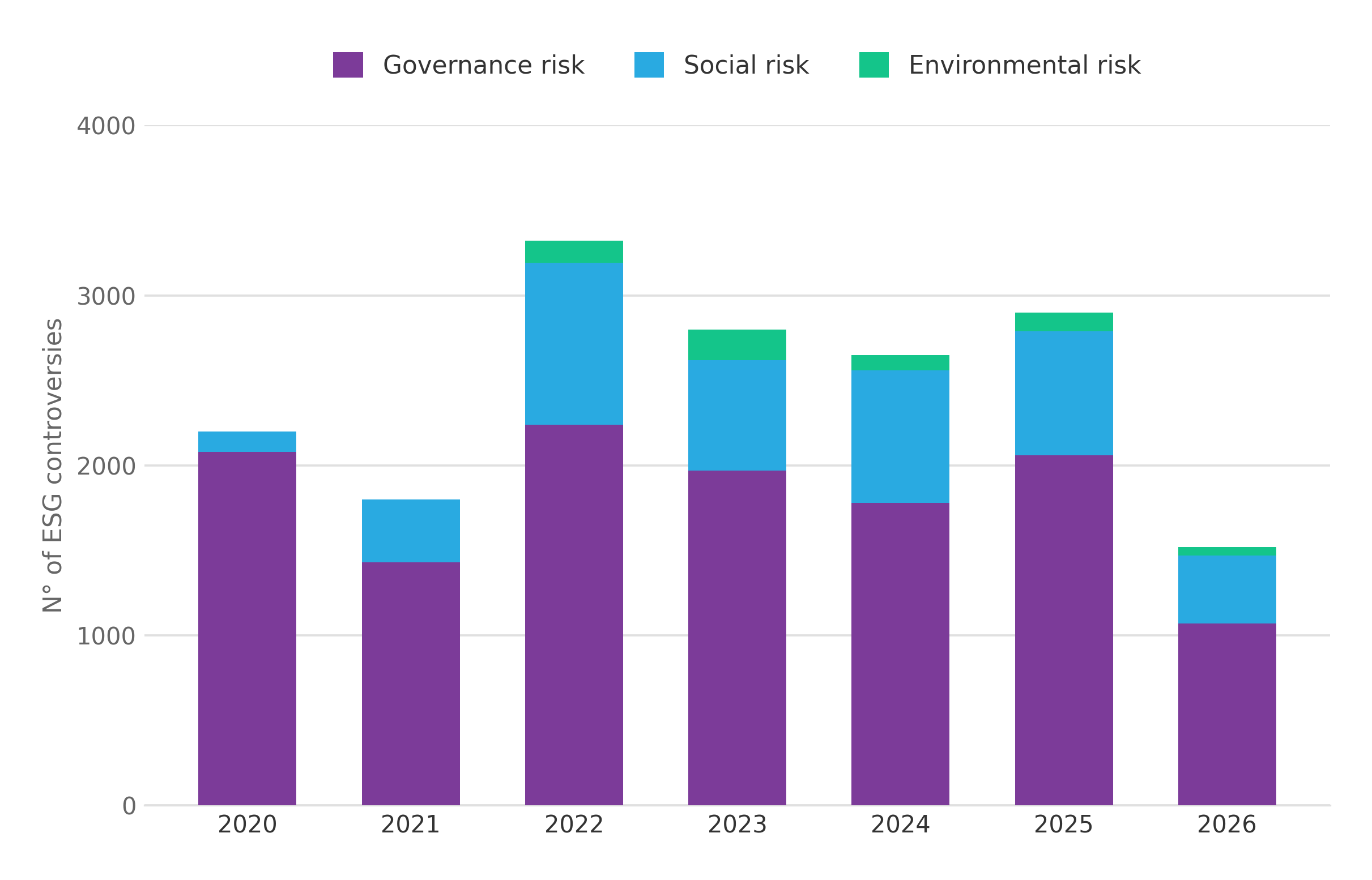

As the breakdown above shows, the overwhelming majority of FIFA's screened ESG events fall into the low-risk tier (1,294, or 88.1%), with 165 (11.2%) on the watchlist and 9 (0.6%) classified as Violator, the highest-risk tier under SESAMm's UN Global Compact screening. That tier is assigned only where there is clear evidence of a breach, such as formal sanctions, court findings, or regulatory condemnations, rather than unresolved allegations. For investors with SFDR Article 8 or 9 obligations, or internal exclusion policies tied to UNGC compliance, a Violator flag on a core holding or counterparty is a material signal rather than a monitoring note, which is why the profile is best read as governance-led: the nine Violator events reflect adjudicated breaches concentrated in FIFA's governance history, not the live controversies surrounding the current tournament.

The composition that emerges is a governance core of long-running legal cases, a Qatar-rooted social overlay that has proven durable, and a small but genuinely high-severity environmental tail now being contested through formal channels.

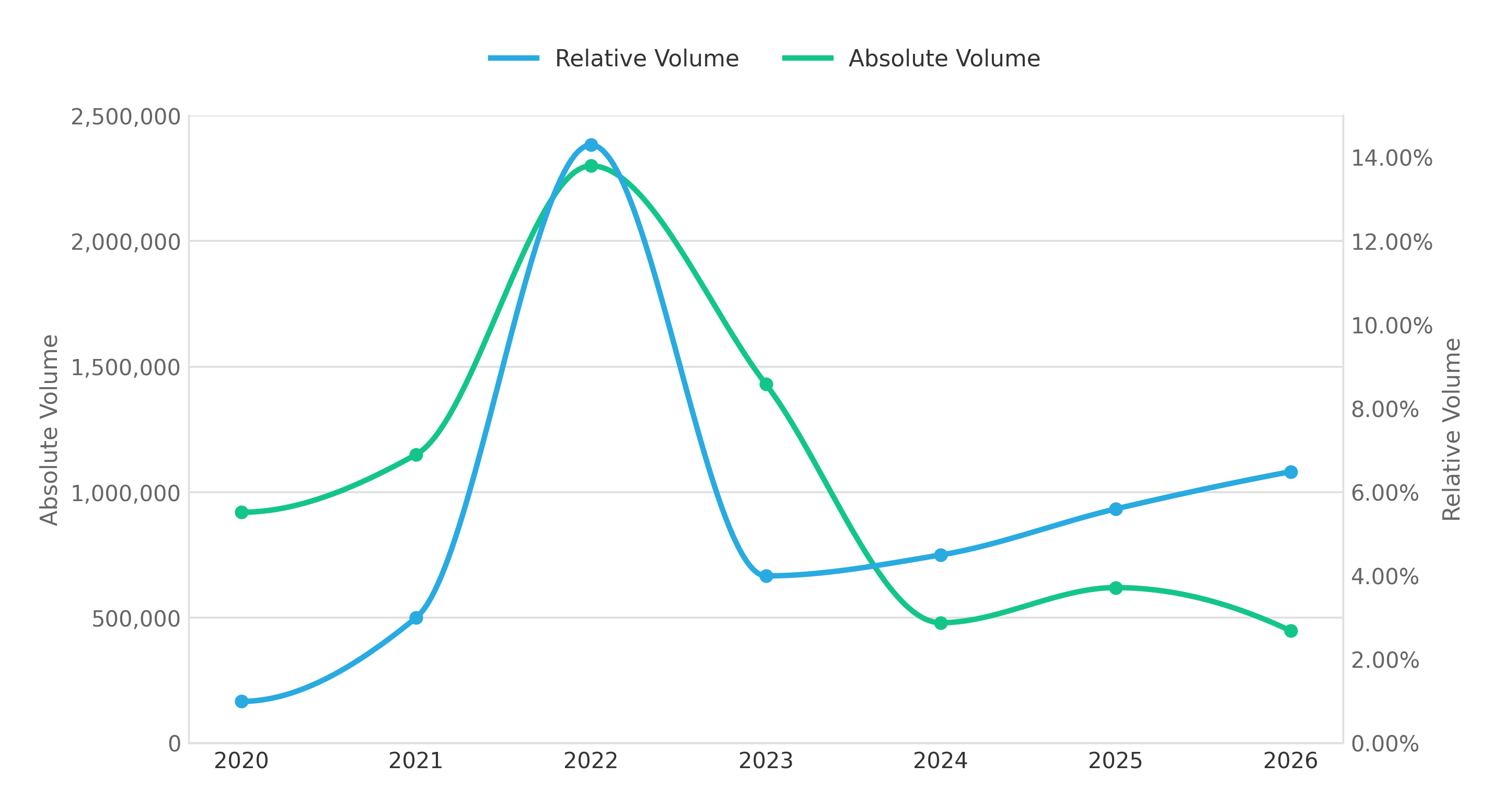

Both lines explode together, but unevenly: absolute volume roughly doubles while the relative share more than quadruples, briefly making Qatar roughly one in seven of all FIFA-related items, because nearly every controversy fires at once. The spike packs in wider labor abuses, and the jailing of whistleblower Abdullah Ibhais; the OneLove armband ban and Qatar's criminalization of same-sex relations and the broader sportswashing and carbon-neutral greenwashing charges; and the unresolved bribery allegations over the 2010 hosting vote. On its own, this acute cluster would suggest a controversy that lives and dies with the tournament.

Phase 3: Off-Season Accumulation (2023–2026)

This is where the two lines part ways, and the accumulation shows itself. After the tournament, the relative share deflates sharply in 2023, the acute spike clearing, but it never returns to baseline; instead, it grinds steadily upward every subsequent year, ending in 2026 at roughly four-and-a-half times its pre-tournament level. Over the same stretch, the absolute volume collapses, from 1.43M in 2023 to around 448K in 2026, under a fifth of the 2022 peak. The two movements together are the key finding: even as total FIFA coverage shrank dramatically, the Qatar migrant-worker case captured a larger and larger share of what remained. Driving that residual are post-tournament findings: The non-payment of the migrant workers during the 2022 World Cup, the campaign for a migrant-worker compensation and remedy fund, and Amnesty's continued push for FIFA to fund remediation.A storyline that merely echoes the event would fade with the falling volume; one that accumulates does the opposite. The controversy is no longer powered by the match calendar but by its own momentum.

The Case Underneath

Underneath that residual sits the report's single heaviest case: the human-rights strand of 135 events running from 2020 to 2026, the longest-running and most densely populated case in the dataset. What stops it fading is that each turn of the hosting cycle reactivates it: the 2026 uptick to 6.49%, the highest reading outside the tournament year itself, coincides with the 2026 World Cup now underway in North America, which revives retrospective scrutiny of Qatar, and the emerging human-rights questions around Saudi Arabia's 2034 tournament, which carries the same migrant-labour lens straight to the next host. The case is not simply failing to fade; it is being actively topped up by each new host, which is why the social exposure reads as structural rather than event-bound.

Key Takeaways

Taken together, the data describes a profile that is primarily governance-related, with the most severe and persistent cases concerning legal exposure, corruption, and bribery, supported by a durable Qatar-rooted social overlay and a small but high-severity environmental tail. All three pillars reach maximum case intensity, so severity is not confined to any single dimension.

The most consistent feature is persistence. FIFA's Controversy Exposure Score has remained in the High-to-Very-High band throughout the period and sits at 99 today. The largest cases run continuously from 2020 to 2026, and a significant share of binding decisions occur outside tournament windows. None of this reduces the significance of the World Cup, which clearly concentrates attention and scrutiny. But the underlying controversy is produced across the quarters between tournaments, and several of FIFA's most consequential outcomes are set during lower-attention periods. For those screening FIFA, the practical implication is that continuous monitoring suits this profile better than event-triggered review, because much of the relevant activity occurs between tournaments rather than during them.

The data suggests that for an entity like FIFA, a four-year review cycle misses most of what matters. Request a demo to see how SESAMm supports the kind of ongoing monitoring this profile requires.

*The Controversy Exposure Score (CES) is a continuous score from 0 to 100 measuring a company's exposure to ESG controversies over time, based on the severity of incidents and their media volume. This is an unsolicited rating: it is not commissioned by the rated company. The company is notified before its score is first issued, does not take part in the rating, and SESAMm has no access to its management or non-public documents. Ratings are produced only from public and licensed sources. The methodology is available here.

Teams that monitor ESG controversies usually have the opposite of an information shortage. A single incident can generate dozens of articles within a few days, each covering the same underlying event, often repeating the same facts with a few new details. At a certain point, the sheer number of articles makes it hard to tell which developments are material and which are just the same story told again.

The volume is the part that breaks traditional approaches. Millions of articles are written every day across hundreds of languages, more than any team of analysts could read, let alone reconcile into a clear timeline of an evolving controversy. This is not a problem you solve by adding more people; the scale is on a different order of magnitude from human reading speed.

What changed is that language models can now read, categorize, and evaluate. They cover that volume in every language, judging whether two articles describe the same incident, whether one marks a new development, and how incidents link into a single controversy over time. Leveraging the latest AI models is the only way to structure this much material and generate daily updates.

SESAMm runs this across the ten million documents it ingests each day, from more than four million sources in over 100 languages, including premium news wires, NGO bulletins, company communications, and discussion forums. The result is ESG controversies organized into three layers: articles, events, and cases.

From Articles to Events to Cases

Each layer builds on the one below it, and each answers a different question an analyst needs answered.

Articles are individual news articles or documents: the raw material.

Events group the articles that describe the same specific incident or development. When forty outlets cover the same supplier labor issue, those forty articles become a single event, with the underlying coverage attached. Articles published close together in time and describing the same development are grouped; an article describing a genuinely new development, even on the same broader topic, forms a separate event. A strike in 2022 and a similar strike in 2024 at the same supplier are recorded as two events, because they are distinct incidents rather than a continuation of one.

Cases sit above events. A case ties together the events that belong to the same underlying controversy as it unfolds, with no fixed time limit. An oil spill, the regulatory investigation that follows it, and the settlement that closes it months or years later are three separate events but one case.

Articles tell you what was written, events tell you what happened, and cases tell you how a controversy is developing. All three sit in the same view: one entry per controversy, with the chronology of events nested inside it and the source articles a click below that.

Why the Underlying Data Matters

A three-layer structure is only as good as the data underneath it. To capture a controversy from start to finish, that data has to include the early signals that appear in regional press, NGO bulletins, or non-English sources before larger outlets report them, sometimes days later.

SESAMm's coverage spans more than 100 languages and extends well beyond mainstream news wires, so its cases are built on a wider base than most monitoring platforms screen. A controversy that starts in a local-language outlet, moves through regional media, and reaches the international press is captured as a single continuous case, rather than surfacing as disconnected alerts or being missed altogether in its early stages.

What Does This Change in Practice?

Three things change in day-to-day work.

The count starts to mean something. A rise in the number of cases reflects new controversies emerging, not an old one being picked up by more outlets.

Trajectories become visible. As a case accumulates new events over the months, the progression from complaint to investigation to hearing to settlement is easy to follow, rather than being buried in hundreds or even thousands of articles.

Analysts spend their time differently. Less of it goes to clearing duplicate headlines, and more to the important judgment calls.

What This Looks Like in the SESAMm Dashboard

In the dashboard, a company appears as a single entity with its related cases listed beneath it. Each case includes a controversy summary, an ESG risk classification, and an intensity score, with related events nested underneath and the original source articles just a click away. A case that draws on hundreds of articles becomes a short, readable list instead of hundreds of separate incidents.

Every case is fully traceable. Analysts can drill from a case down to its events, and from any event to the articles that produced it. The time period is set from the top of the dashboard, so older incidents do not crowd the view when the focus is on recent activity.

Reducing Noise in Adverse Media Monitoring

In practice, those forty articles collapse into one event, and that event sits inside a single case that is still developing, caught early and drawn from sources most platforms never see.

Grouping articles into events removes duplication caused when many outlets cover the same incident. Grouping events into cases keeps a controversy intact as it develops, rather than scattering it across months of separate alerts. Because this runs across ten million documents a day in more than a hundred languages, it holds up even for controversies that start far from the mainstream press.

The result is a view where the numbers carry meaning, the direction of an issue is clear, and the underlying articles stay one click away for full validation.

The dominant story about responsible investment in 2026 is one of retreat. ESG funds are losing assets, regulatory frameworks are under review, and political pressure has reshaped how firms talk about sustainability. The word "backlash" has done a lot of work over the past two years.

In a recent webinar, “Responsible Investment in the Nordics: What Comes After ESG Leadership?” Sylvain Forté and Magnus Billing argued for a different framing. If you look past the headlines, at how institutional capital actually behaves and what European asset owners are actually building, a different picture emerges. What is taking place is not a reversal. It is a calibration, and the direction of travel has not changed.

Two stories, told as one

Much of the confusion stems from conflating the United States and Europe into a single "ESG retreat" narrative. In reality, the two markets are doing different things for different reasons.

In the United States, for example, the political environment has shifted, and parts of the industry have adjusted accordingly in response. The picture, however, is more nuanced than the headlines suggest. According to Malk Partners' State of ESG 2026 report, most of the recalibration in the US has centered on DEI programming, as firms navigate a more complex legal landscape. Other dimensions of ESG, including climate, governance, and ESG policy frameworks, have largely held their ground. On the LP side, support for ESG continues to set the tone of the market, and ESG diligence remains an important consideration for many large institutional investors when evaluating GPs.

Europe's story is different. The current cycle of regulatory revision is best understood as the maturation of a framework that grew faster than the data and definitions underneath it could support. The European Action Plan on Sustainable Finance set the right ambition, but the early implementation accumulated disclosure requirements faster than they could be reconciled. For a period, the cost of compliance threatened to crowd out the substance of what responsible investing was meant to deliver.

What is unfolding now is a recalibration. The Commission's proposed SFDR 2.0, the EU Omnibus Directive easing certain CSRD requirements, ESMA's incoming rules on ESG ratings providers, parallel work at the FCA in the UK, and progress in Switzerland all point in the same direction. The frameworks are being simplified, not dismantled. The ambition has not changed. The execution is finding its level.

What the data actually shows

The structural evidence for continued European commitment is clear. European GPs overwhelmingly report that the business case for ESG has either held steady or grown stronger over the past year, and almost none describe a weakened case. European firms continue to do more ESG diligence, more portfolio-level data collection, and more sell-side review than their U.S. counterparts, and European portfolio companies are far likelier to see ESG as a source of financial value. Even where regulation has eased, as with the Omnibus simplifications, demand for ESG data from customers and investors has barely shifted. The drivers were never primarily regulatory.

This makes sense once you look at what actually shapes institutional behavior. Pension funds and life insurers hold long-duration liabilities, which forces a horizon measured in decades rather than quarters. Climate risk has not become less material because the definition was simplified. Reputational risk has not slowed either; if anything, social media and AI-generated content have accelerated the speed at which controversies can damage a portfolio company's standing. And supply-chain exposures to geopolitical events, from the Strait of Hormuz to Red Sea shipping to Xinjiang, have become more central to risk management, not less.

In other words, the institutional case for responsible investment was never entirely about regulation. It was about durable risk and durable opportunity, and both are still very much present.

The pressures shaping how the work gets done

Alongside this calibration, three challenges are changing how responsible investment is practiced day-to-day. None of them is brand new, but they are slowly reshaping what investment teams actually have to do.

Speed: Reputational damage can now compound within hours rather than weeks, accelerated by social media and the velocity of AI-generated content. Traditional ESG ratings, designed for long review cycles, were not built for that tempo. The pressure to detect and respond to emerging issues in something close to real time has become harder to ignore.

Scope: Institutional allocations to private markets and infrastructure have grown steadily, yet the data coverage for those asset classes has historically been thin. The same gap exists across deep supply chains and local-language sources. The expectation that ESG analysis can stop at the boundaries of public equities, in English, on a quarterly cadence, simply no longer holds.

Cost of analysis: Some of the frustration that fed the "ESG retreat" narrative was that too much was being spent producing reports and too little on acting on what they said. As compliance overhead is rationalized under the new generation of frameworks, the question becomes how to redirect that capacity toward the parts of the work that actually move investment decisions.

What does it mean going forward?

For institutions thinking about the next five years, a few principles stand out.

The first is to treat responsible investing as a risk management discipline rather than a separate function, so that the data, the workflows, and the governance sit alongside the rest of the investment process. The second is to expect the data perimeter to keep expanding, given that local-language coverage, private assets, infrastructure, supply chains, and the way brands appear inside AI-generated answers are all part of a frontier that widens every quarter. The third is to keep humans in the loop by design, because while AI is closing coverage gaps and accelerating analysis, it is not, and should not be, making the final call.

The retreat narrative will keep drawing headlines. The capital, and the institutional commitment behind it, are telling a different story. As Magnus put it: "I object a little bit to the word backlash. In the European context, the word is calibration rather than backlash. The direction of travel is the same."

ESG, in other words, is not going away. It is settling into a more honest, more operational version of itself, and the institutions that recognize that early will be the ones best positioned for what comes next.

Northvolt was Europe's flagship battery champion, backed by Volkswagen, Goldman Sachs, BMW, and BlackRock, and capitalized with over $13 billion in debt and equity. Yet between 2022 and 2025, it became the largest industrial bankruptcy in modern Swedish history, shocking the industry and investors alike. We took a look back at SESAM’s controversy data to see if there were any early warning signals.

The Warning Signs

In September 2022, the first public reports of production delays emerged at Northvolt's Skellefteå gigafactory. By the end of 2023, less than 1% of the planned 16 GWh capacity for 2024 had been delivered. Then came the fatal workplace accidents linked to electrical experiments, and in June 2024, BMW canceled a €2 billion contract. By September, 1,600 employees had been laid off, the cathode expansion was abandoned, and the CFO was replaced.

The Fallout

The consequences were swift. A Chapter 11 filing in the U.S. in November 2024. The resignation of founder and CEO Peter Carlsson. Over 5,000 jobs lost. Major write-downs across the cap table, from sovereign-backed pension funds to global automakers. In March 2025, Northvolt filed for bankruptcy in Sweden, the largest industrial failure in the country's modern history. The reputational damage extended well beyond the company itself, reaching investors, suppliers, and the broader European battery ambition.

The private markets secondaries space has entered a new chapter. What was once a niche corner of alternative investments, used primarily by limited partners (LPs) seeking early exits from fund commitments, has grown into one of the most dynamic segments of global private capital. The market has tripled in size since 2019 and grown by approximately 50% between 2024 and 2025 alone, reaching an estimated $230 billion in annual transaction volume and now representing around 5% of all global private equity assets under management.

This piece examines the forces behind that expansion, the structural shifts redefining the market, and the operational and regulatory challenges participants will need to navigate as the asset class continues to scale.

Market Growth and Shifting Deal Dynamics

Several converging factors have driven the secondaries market to its current size. A prolonged slowdown in IPO activity and traditional exits has created a liquidity bottleneck across private markets, leaving many LPs over-allocated to alternatives and constrained in their ability to make new commitments. The secondary market has become a primary mechanism for these investors to rebalance portfolios and free up capital.

Deal structuring has grown more sophisticated in step with market volumes. Ropes & Gray has observed a continued expansion in the use of purchase price deferrals and earnouts, and more recently, the introduction of deal-specific funding caps, limits on how much capital a buyer can be called to deploy before a specified date. These mechanisms allow sellers to achieve higher reference-date pricing while enabling buyers to manage capital deployment pacing and portfolio composition. In Q1 2026 alone, institutions initiated new secondary sales processes totaling north of $20 billion, some linked to denominator effect concerns as declines in public market portfolios pushed private allocations above target levels. Whether this proves a sustained driver of supply will depend on how institutional portfolios weather current market conditions.

The Three Transaction Types

Secondary transactions fall into three main categories:

LP-led transactions, the original form, involve an LP selling existing fund interests, sometimes across a broad portfolio of hundreds of positions, typically through competitive auction processes with tight timelines.

GP-led continuation funds, the fastest-growing segment, involve a sponsor transferring select assets into a new vehicle, giving existing LPs the option to cash out or roll forward. As of 2025, GP-led and LP-led volumes are roughly evenly split at around $115 billion each. GP-led buyout fund volume grew 39% year-over-year, while private credit secondaries saw nearly 300% year-over-year growth in GP-led activity.

The third category, structured solutions, provides capital to a GP collateralized by existing fund assets and can take a wide variety of bespoke forms.

What Are the Operational and ESG Challenges in the Market?

One of the defining challenges in secondaries is the speed and scale of due diligence required, particularly in LP-led transactions. Buyers may need to evaluate hundreds, or in private credit secondaries, over a thousand, underlying positions with limited information and within windows of 24 to 48 hours. As Jessica Huang, Managing Director and ESG lead for private equity and secondaries at Ares Management, noted in a recent webinar:

Against this backdrop, LP expectations around ESG integration have risen sharply. LPs are now holding secondaries to a standard closer to that applied to direct investments, with requests for Article 8-classified funds, look-through exclusion lists, and UN Global Compact compliance screening becoming more common. Main exclusion categories include fossil fuels, controversial weapons, tobacco, and gambling, though definitions and revenue thresholds vary significantly across mandates. SFDR 2.0, currently in draft form, may introduce additional mandatory exclusion categories that managers are monitoring closely. In LP-led deals where buyers are inheriting a broad portfolio of assets, highly granular opt-outs can mean missing certain large transactions, a trade-off that must be clearly communicated to LPs.

The Role of Technology and AI

Technology has become central to the scaling of secondaries operations. AI tools are now applied across controversy screening, ESG data analysis, and emissions estimation, where direct disclosures are unavailable. A particular challenge in the asset class is coverage: many underlying companies are small or mid-market private businesses not captured in conventional databases.

Market participants consistently emphasize that AI outputs serve as inputs to human judgment, not as replacements for it. At Ares, screening results are reviewed by ESG specialists before being passed to deal teams for final decisions.

What the Future Holds

Transaction volumes are forecast to continue rising as both the seller and buyer universes expand. Private credit, infrastructure, and structured secondaries all represent areas of growing specialization and regional expansion, particularly in Asia, where secondary activity has been limited but is expected to grow as investment programs mature, broadening the market further. Capital supply dynamics bear watching: while dry powder remains substantial, deal volume growth has outpaced fundraising since 2023, which could create pricing or capital constraints. The entry of retail investors through evergreen vehicles adds a meaningful new source of capital but brings different liquidity expectations and regulatory considerations.

On the operational side, the sophistication of deal terms, the complexity of ESG compliance, and the volume of data processed per transaction are all increasing. Firms that can integrate technology into their diligence and monitoring workflows, while preserving the human judgment layer, will be best positioned to manage market growth. Secondaries are no longer a supplementary liquidity tool; they have become a structural feature of how private markets operate.

Forced labor is often assumed to be a problem of distant supply chains. The case of Packers Sanitation Services Inc. (PSSI) dismantles that assumption entirely.

PSSI was a leading U.S. industrial cleaning contractor, servicing major meatpacking plants and backed by a top-tier private equity firm. Yet between 2022 and 2024, it became the center of one of the most significant child labor scandals in the U.S., one that had been quietly signaling its risks for years. SESAMm's controversy monitoring platform captured those early signals long before regulators intervened.

The Scandal

In November 2022, the U.S. Department of Labor discovered that PSSI had employed minors as young as 13 in hazardous overnight roles across 13 locations in 8 states. A federal investigation confirmed 102 children had been illegally employed, many handling dangerous chemicals and machinery. Three years earlier, in 2019, PSSI had already been sued for wage violations. The signal was there. It went unheeded.

The Fallout

The consequences were swift. A $1.5 million DOL fine. Contract terminations by Cargill and JBS. A DHS trafficking investigation. A replaced CEO. By late 2024, PSSI had shut its corporate office entirely. Even the private equity owner, Blackstone, faced direct scrutiny from pension funds, a reminder that labor violations travel up the ownership chain.

The Lesson

Every warning sign in this case was publicly visible before the crisis broke out. Wage lawsuits, labor complaints, and media coverage are all available in the public domain. Real-time controversy monitoring can surface these signals early, giving companies and investors the chance to act before exposure becomes unavoidable.

Forced labor is not only a humanitarian crisis. It is a material risk that demands better data, earlier detection, and stronger accountability.

Download the full case study infographic to see the complete timeline of events and key takeaways

The physical infrastructure powering the AI boom (the data centers that house it, and the hardware that runs it) has become one of the most ESG-exposed sectors in the global economy. As demand for computing accelerates, so does the scrutiny on the companies enabling it.

This scorecard examines three major players across the AI infrastructure stack: Equinix and Digital Realty, two of the world's largest data center operators, and Supermicro, a leading manufacturer of high-performance AI server hardware. Despite their different roles, all three are navigating the same storm: a convergence of governance failures, environmental friction, and national security risk that is reshaping how investors, regulators, and communities assess the sector.

Our analysis reveals three defining pressure points: governance failures spanning accounting manipulation, board instability, and fraud; environmental and social friction from community opposition, resource strain, and safety violations; and national security exposure through data breaches, export control violations, and supply chain risk.

Together, these risks represent a fundamental shift for the sector. ESG in AI infrastructure is no longer about carbon reporting - it is about fiduciary integrity, operational transparency, and the social license to keep building.

With a controversy exposure score (CES) of 80/100, Supermicro’s ESG profile is dominated by extreme governance risks centered on systemic accounting failures and geopolitical compliance breaches. The company is currently battling a U.S. Justice Department probe, Nasdaq delisting threats, and a series of securities fraud lawsuits following a 2024 accounting scandal that forced the search for a new CFO and echoed a prior $17.5 million SEC fine from 2020.

Beyond financial integrity, the firm faces severe national security scrutiny over the alleged smuggling of restricted Nvidia AI chips to China, alongside 2025 investigations into "spy chips," unremovable motherboard malware, and multiple patent infringement claims from competitors like AMD and Lenovo. Socially, the company’s risk is compounded by a 2025 whistleblower retaliation suit and labor rights violations involving Filipino workers at its semiconductor supply chain partners, as well as multiple OSHA safety penalties for workplace hazards.

Equinix: Accounting Manipulation & the AI Infrastructure Backlash

Similarly, Equinix’s CES of 79/100 is defined by a volatile combination of intensifying community opposition, environmental resource strain, and severe governance scrutiny. Socially and environmentally, the company faces a "Global AI Arms Race" backlash, where massive 340-acre proposals on local farmland in Minooka and "green belt" developments in South Mimms have sparked significant resident opposition over air pollution and traffic, while regulators in Dublin have begun blocking gas-powered facilities that violate national climate targets. These operational hurdles are compounded by a lack of transparency regarding massive water consumption and a series of high-profile safety and security failures, including data center fires in São Paulo and Madrid and a recurring "cybersecurity blind spot" in building systems. On the governance front, Equinix is navigating a severe trust deficit following a $41.5 million settlement over allegations of "major accounting manipulations" and the systematic over-selling of power capacity.

Digital Realty: Board Instability, Gas Leaks & Cybersecurity Breaches

Although it has a lower CES of 48/100, Digital Realty’s ESG profile is defined by governance instability and intensifying environmental friction in key urban hubs. The abrupt 2022 termination of its CEO and the 2023 resignation of its Chairman, who alleged bias against female directors, highlight deep-seated board-level conflicts, further exacerbated by 2026 investigations into director bias and a $3.4 million loss of tax breaks in Hillsboro.

Environmentally, the company faces formal legal notices in Marseille over fluorinated gas leaks and "imminent dangers to health," as well as noise complaints in Chicago and a 2024 fire in Singapore. Socially, the firm is navigating a Biometric Information Privacy Act (BIPA) lawsuit over scanning workers' fingerprints without consent, a major 2025 "Salt Typhoon" hacking breach, and mounting federal scrutiny over the industry's role in driving up local electricity and water costs.

The ESG challenges facing AI infrastructure operators are no longer peripheral concerns; they have become central to the sector's long-term viability. As the cases of Equinix, Supermicro, and Digital Realty illustrate, the consequences of their unchecked growth range from community backlash and environmental violations to governance failures and national security breaches. The AI infrastructure industry stands at an inflection point: continued expansion without proportional investment in transparency, accountability, and sustainability risks eroding stakeholder trust, inviting heavier regulation, and ultimately undermining the very infrastructure it seeks to build.

Discussions around nuclear weapons and defense have recently highlighted how differently investors interpret weapons exclusions. In particular, Russia’s invasion of Ukraine has brought security considerations back into focus across Europe and prompted some investors to revisit long-standing exclusion policies.

At the same time, regulatory frameworks such as the Sustainable Finance Disclosure Regulation (SFDR) encourage investors to screen portfolios for controversial activities and disclose how those risks are managed. However, these frameworks do not impose a single global definition of weapons exposure. As a result, policies can vary widely between institutions.

Controversial Weapons

What Do We Mean by Controversial Weapons?

In responsible investment policies, the term “controversial weapons” has a relatively clear meaning. It refers to weapons that are prohibited or heavily restricted under international conventions because of their indiscriminate or humanitarian impacts. Typical examples include:

cluster munitions

anti-personnel landmines

chemical weapons

biological weapons

nuclear warheads

Because these weapons are banned or widely condemned under international treaties, investors usually apply strict zero-tolerance exclusions. Any company involved in producing these weapons, or supplying critical components for them, is typically excluded from ESG-focused portfolios.

What Counts as Weapons Exposure?

The broader category of weapons exposure is more complex and is where investor interpretations often begin to diverge. Recent discussions across Europe’s sustainable finance community have focused on whether defense companies should remain excluded from ESG portfolios, particularly in light of renewed security concerns following Russia’s invasion of Ukraine.

Many exclusion frameworks distinguish between controversial weapons and other forms of military-related activity. Companies may be involved in conventional weapons manufacturing, such as firearms, missiles, bombs, or military electronics. Others produce defense systems and equipment, including radar, communications technology, or aircraft components. Civilian firearms are also frequently treated as a separate category within exclusion policies.

In these cases, investors often rely on revenue thresholds rather than absolute bans. A company may be excluded if more than five to ten percent of its revenue comes from weapons manufacturing, while smaller or indirect exposure may still be permitted depending on the investor’s mandate.

A key challenge in these screenings is that a company’s weapons exposure is not always obvious from its core business description. A firm may supply components, software, or materials used in weapons systems or operate as part of a broader defense supply chain. This is particularly difficult to identify in private markets, where companies are not required to disclose detailed segment revenues or defense-related contracts.

As a result, defining and detecting weapons exposure requires clear policy definitions and structured screening logic. What counts as weapons involvement, and where the exclusion threshold lies, ultimately depends on each investor’s mandate and risk tolerance.

What's Different Now?

These questions are no longer abstract. Since Russia's invasion of Ukraine, major asset managers have visibly shifted their positions. Allianz Global Investors, for instance, updated its Article 8 fund policies in 2025 to allow defense companies. Global Trading UBS and Franklin Templeton made similar moves, each removing revenue-based weapons thresholds that had been standard practice for years. At the regulatory level, Hortense Bioy, Head of Sustainable Investing Research at Morningstar Sustainalytics, noted that "since the start of the war in Ukraine in 2022, it has become increasingly clear that geopolitics plays a more significant role in shaping the boundaries of sustainable investing than ethics." What these shifts share is a common thread: the thresholds and definitions that once felt settled are now being redrawn, which is precisely why screening frameworks need to be flexible enough to reflect each investor's current policy, whatever that may be.

Customizable Screening

Because exclusion policies are defined at different levels, it’s rarely as simple as establishing a generic exclusion list. Limited partners often impose their own restrictions or revenue thresholds, which general partners must apply alongside the fund’s internal ESG policy and regulatory restraints. In some cases, LP requirements may further restrict or override the fund’s baseline approach.

As a result, acceptable levels of exposure to activities such as conventional weapons can vary significantly across portfolios.

Screening frameworks, therefore, need to adapt to the investor’s policy rather than forcing the policy to adapt to the tool.

In this case, SESAMm’s AI-generated exclusion screening report can be customized to match each investor’s requirements. Threshold-based classifications help identify different levels of involvement, allowing investors to distinguish between companies with no exposure, limited exposure, or significant involvement in controversial activities. Each classification is supported by underlying evidence and source documentation, allowing analysts to verify the reasoning behind the flag.

This approach makes it possible to apply a consistent methodology across both public and private companies while remaining aligned with the investor’s specific exclusion framework.

Discussions around defense and responsible investment will continue to evolve as geopolitical and regulatory contexts shift. Recent debates around nuclear deterrence and defense participation illustrate how differently investors can interpret weapons exclusions, even when they operate under the same regulatory frameworks.

For investors, the challenge is therefore not only defining exclusion policies but ensuring that those policies can be applied consistently and transparently across portfolios. As definitions of weapons exposure vary, and as supply chains and private market structures add further complexity, screening frameworks must be capable of translating policy into clear, operational rules.

.png)

-converti-depuis-png.avif)

-converti-depuis-png.avif)

.png)