SESAMm Selected by ENGIE to Enhance ESG and Reputation Monitoring

September 30, 2025

•

5 mins read

SESAMm, the leading provider of controversy data, is pleased to announce that ENGIE has chosen SESAMm to strengthen its ESG risks monitoring of subsidiaries, including positive impact news.

SESAMm delivers real-time controversy data on millions of private and public companies, leveraging multilingual large language models to analyze content from more than 4 million sources in 100+ languages. This enables SESAMm to surface potential red flags such as human rights violations, corruption, and environmental breaches, even in hard-to-assess, non-listed firms, while also highlighting positive impact events.

With SESAMm’s AI-powered platform, ENGIE will supplement its ESG analysis tools for its global operations. This includes early detection of controversies, benchmarking against industry peers, and surfacing positive achievements that reinforce ENGIE’s role in the energy transition.

“We’re proud to support ENGIE in monitoring both risks and opportunities,” said Sylvain Forté, CEO and co-founder of SESAMm. “Our AI-driven insights will help their teams anticipate challenges, benchmark effectively, and showcase progress in building a more sustainable future.”

About ENGIE

ENGIE is a major player in the energy transition, whose purpose is to accelerate the transition towards a carbon-neutral economy. With 98,000 employees in 30 countries, the Group covers the entire energy value chain, from production to infrastructure and sales. ENGIE combines complementary activities: renewable electricity and green gas production, flexibility assets (notably batteries), gas and electricity transmission and distribution networks, local energy infrastructures (heating and cooling networks), and the supply of energy to individuals, local authorities, and businesses. Every year, ENGIE invests more than €10 billion to drive forward the energy transition and achieve its net-zero carbon goal by 2045. Learn more at www.engie.com.

About SESAMm

SESAMm is a global leader in controversy data, leveraging advanced large language models and generative AI to uncover ESG, reputational, and supplier risks in seconds. Our AI-powered platform surfaces real-time insights, even in low-disclosure markets, on millions of companies and infrastructure projects, supporting more informed decisions, enhanced due diligence, and regulatory alignment at scale. We work with leading firms, including Carlyle, Warburg, Natixis, RBI, Sustainable Fitch, Oddo, and others. SESAMm has raised $50M from renowned investors and operates across four continents. Learn more at www.sesamm.com.

SESAMm’s AI Technology Reveals ESG Insights

Discover unparalleled insights into ESG controversies, risks, and opportunities across industries. Learn more about how SESAMm can help you analyze millions of private and public companies using AI-powered text analysis tools.

SESAMm, the leading provider of controversy data, is pleased to announce that ENGIE has chosen SESAMm to strengthen its ESG risks monitoring of subsidiaries, including positive impact news.

SESAMm delivers real-time controversy data on millions of private and public companies, leveraging multilingual large language models to analyze content from more than 4 million sources in 100+ languages. This enables SESAMm to surface potential red flags such as human rights violations, corruption, and environmental breaches, even in hard-to-assess, non-listed firms, while also highlighting positive impact events.

With SESAMm’s AI-powered platform, ENGIE will supplement its ESG analysis tools for its global operations. This includes early detection of controversies, benchmarking against industry peers, and surfacing positive achievements that reinforce ENGIE’s role in the energy transition.

“We’re proud to support ENGIE in monitoring both risks and opportunities,” said Sylvain Forté, CEO and co-founder of SESAMm. “Our AI-driven insights will help their teams anticipate challenges, benchmark effectively, and showcase progress in building a more sustainable future.”

About ENGIE

ENGIE is a major player in the energy transition, whose purpose is to accelerate the transition towards a carbon-neutral economy. With 98,000 employees in 30 countries, the Group covers the entire energy value chain, from production to infrastructure and sales. ENGIE combines complementary activities: renewable electricity and green gas production, flexibility assets (notably batteries), gas and electricity transmission and distribution networks, local energy infrastructures (heating and cooling networks), and the supply of energy to individuals, local authorities, and businesses. Every year, ENGIE invests more than €10 billion to drive forward the energy transition and achieve its net-zero carbon goal by 2045. Learn more at www.engie.com.

About SESAMm

SESAMm is a global leader in controversy data, leveraging advanced large language models and generative AI to uncover ESG, reputational, and supplier risks in seconds. Our AI-powered platform surfaces real-time insights, even in low-disclosure markets, on millions of companies and infrastructure projects, supporting more informed decisions, enhanced due diligence, and regulatory alignment at scale. We work with leading firms, including Carlyle, Warburg, Natixis, RBI, Sustainable Fitch, Oddo, and others. SESAMm has raised $50M from renowned investors and operates across four continents. Learn more at www.sesamm.com.

SESAMm’s AI Technology Reveals ESG Insights

Discover unparalleled insights into ESG controversies, risks, and opportunities across industries. Learn more about how SESAMm can help you analyze millions of private and public companies using AI-powered text analysis tools.

A single number is a powerful thing. It can summarise months of reporting across dozens of sources into something a risk team can act on in seconds. It can also hide more than it reveals, if no one explains how it was built. When the same company receives very different ESG scores from different providers, the usual reason is not bad data. It is undisclosed method.

SESAMm has published the full methodology behind its Controversy Exposure Score, free to access, following the entry into force of the EU ESG Rating Regulation on 2 July 2026. This article walks through what the score measures, how it is constructed, and the two design choices that most distinguish it.

What the Score Measures

The Controversy Exposure Score, or CES, runs on an absolute scale from 0 to 100 and is grouped into five risk bands, from Very Low to Very High. It has a single, deliberately narrow objective: to measure an entity's exposure to ESG controversies, meaning adverse events and conduct attributed to that entity as reported in public sources.

Three points define its scope from the outset. The CES is an impact-materiality measure. It looks at the negative footprint of an entity's activities on people and the environment, not the financial effect of ESG issues on the company itself. It is backward-looking. It reflects controversies that have already been reported, over a rolling 24-month window, rather than forecasts or transition pathways. And it is built only from public and licensed public-domain information, never from private, confidential or self-reported data.

From Millions of Articles to a Single Case

Before any score can exist, raw coverage has to become structured information. This is where most of the engineering sits.

SESAMm's pipeline first attributes each document to the right entity and screens it for genuine ESG relevance against a multilingual taxonomy, removing low-quality, duplicate or non-editorial content. It then addresses a problem familiar to anyone who monitors the news: media echo. A single real-world incident can generate dozens of near-identical articles. To prevent that from inflating the picture, related documents are grouped into Events, and related Events into Cases, so that a controversy unfolding over time is tracked as one continuous case rather than many separate items.

A validation step then confirms that each candidate event is a genuine ESG controversy concerning the entity, acting as a control against false positives before anything enters the score. Only after this sequence does scoring begin.

Design Choice One: Severity Before Volume

The most important question about any controversy is not how many articles it generated. It is how serious it is. SESAMm assesses severity first, through a feature called Event Intensity, scored on a 1 to 5 scale.

Severity is judged on two axes. The first is reversibility, the permanence of the harm, from a procedural or technical breach at the low end to irreversible damage such as fatalities or permanent ecosystem destruction at the high end. The second is reach, the scale of the impact, from an effect confined to a single facility up to systemic or national-level harm.

Two principles govern how these combine, drawn from the UN Guiding Principles approach to identifying severe impacts. Permanence takes priority over breadth, so an irreversible harm weighs more than a widespread but remediable one. And grave, irreversible events are designed not to slip into low-severity tiers simply because their reach was limited, so that isolated but serious events stay visible. The structured severity is then adjusted for the entity's actual responsibility, from direct involvement through its own operations to indirect involvement through its value chain.

Media coverage does play a role, but a disciplined one. The level of coverage contributes to the score as a signal of salience, and it is rebased against each entity's own historical media baseline rather than counted in absolute terms. This stops high-profile companies from looking riskier simply because they attract more press, and it keeps the engine sensitive to genuine spikes at less-covered entities.

Design Choice Two: Worst-Of, Not Average

The second defining choice is how the pillars combine. Most ESG scores apply percentage weights to Environmental, Social and Governance factors and blend them into a weighted average. SESAMm deliberately does not.

The reason is a structural flaw the company calls dilution bias, or data masking. When pillars are averaged, strong administrative compliance in one area can mathematically conceal a catastrophic breach in another. A company with excellent governance disclosures could see a severe environmental controversy diluted into a comfortable middle score.

Instead, the CES uses a rule-based maximum-severity, or worst-of, logic. The entity's most serious controversy drives the score, regardless of which pillar it sits in, and it cannot be watered down by stable metrics or an absence of alerts elsewhere. The five bands that result are fixed in absolute terms rather than calculated relative to a peer group, so a company's score is not flattered or punished by the behaviour of its sector. A score above 80 reflects critical, often irreversible breaches. A score of 20 or below reflects negligible or minor isolated issues.

A Number You Can Interrogate

Taken together, these choices produce a score with a clear logic behind every point on the scale. Severity is assessed before volume. The gravest event leads. Coverage is normalised so it informs rather than distorts. And the bands mean the same thing for every entity, in every sector, anywhere in the world.

None of this requires a user to take the result on faith. The objective, the taxonomy of 44 sub-risks, the severity model, the aggregation rule and the interpretation of each band are all set out in the public methodology. A score is only as useful as the method that produced it, and that method is now open to read.

To see exactly how the Controversy Exposure Score is constructed, visit sesamm.com/methodology.

The European Union stands at the forefront of global efforts to promote environmental, social, and governance (ESG) accountability. As the world becomes increasingly ESG-aware, the EU has developed a comprehensive regulatory framework designed to ensure transparency and accountability across all sectors.

These regulations represent the EU's commitment to sustainable development and responsible business practices. However, the regulatory landscape is evolving, with the February 2025 EU Omnibus Proposal introducing potential modifications aimed at reducing the regulatory burden on businesses. However, these proposals come at the risk of substantially undercutting the impact of the regulations.

This article recaps the current ESG regulatory framework in the EU, explores the changes proposed by the Omnibus, analyzes the potential impacts of these modifications, and discusses how financial institutions can navigate this evolving landscape while maintaining compliance.

The ESG Regulatory Landscape in the EU

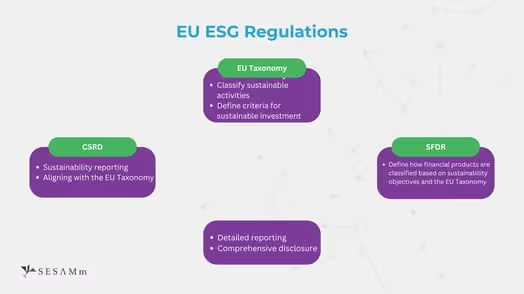

The EU is advancing sustainability through a framework of regulations that enhance corporate accountability and reporting on ESG impacts. These measures aim to promote genuine sustainable practices and address international trade and emissions challenges. Though comprehensive, these regulations are also, at times, confusing in the way they overlap and impact each other. To get started, let’s examine the EU Taxonomy, SFDR, and CSRD—a triad of interconnected regulations designed to streamline and strengthen sustainable investing practices.

EU Taxonomy

The EU Taxonomy provides a classification system for environmentally sustainable economic activities, offering clear criteria to determine whether an economic activity can be considered "green."

Key Aspects of the EU Taxonomy

Defines criteria for environmentally sustainable economic activities

Requires companies subject to CSRD to report on Taxonomy alignment

The Taxonomy helps channel investment toward genuinely sustainable projects and businesses by creating a common language for sustainable activities.

Status

The EU Taxonomy has been operational since January 2022 with phased implementation. As of March 2025, companies subject to CSRD must disclose their taxonomy alignment percentages.

Sustainable Finance Disclosure Regulation (SFDR)

The SFDR focuses specifically on the financial sector, requiring financial market participants to disclose how they integrate ESG risks into their investment decisions and the sustainability impact of their financial products.

Key Aspects of SFDR

Requires disclosure of ESG risks in investment processes

Classifies financial products based on their sustainability characteristics

Aligns with EU Taxonomy criteria for sustainable investments

Aims to prevent greenwashing in financial products

The SFDR plays a crucial role in bringing transparency to the rapidly growing sustainable investment market.

Status

Fully implemented since March 2021, with enhanced Level 2 requirements since January 2023. All EU financial market participants must classify products under Articles 6, 8, or 9. Current market data shows that 28% of EU funds are compliant with Article 8 and 5% with Article 9, with a significant trend of reclassification from Article 9 to 8 due to stricter interpretations.

The CSRD stands as a cornerstone of the EU's ESG regulatory framework, requiring companies to report comprehensively on their environmental, social, and governance impacts. This directive mandates alignment with the EU Taxonomy, ensuring standardized reporting of sustainability metrics.

Key Aspects of CSRD

Requires detailed reporting on ESG impacts

Aligns with EU Taxonomy criteria for sustainability

Currently applies to companies with 250+ employees

Enhances corporate transparency on sustainability issues

The CSRD represents a significant step forward in standardizing sustainability reporting across the EU, providing investors, consumers, and regulators with comparable information on corporate sustainability performance.

Status

The CSRD, adopted in November 2022, replaces the Non-Financial Reporting Directive (NFRD). The transition to CSRD reporting was originally slated to begin in 2025 and would expand the number of companies subject to reporting requirements to 49,000 (vs 11,700 under NFRD). However, as we’ll see later, the Omnibus may push back the timing of CSRD.

Outside of the EU Taxonomy, SFDR, and CSRD, the Omnibus Proposal highlights two other key ESG regulations: CSDDD and CBAM. These regulations relate to corporate accountability for supply chains and to limiting carbon leakage.

Corporate Sustainability Due Diligence Directive (CSDDD)

The CSDDD focuses on corporate accountability throughout global supply chains, requiring companies to identify, prevent, and mitigate human rights and environmental risks associated with their operations.

Key Aspects of CSDDD

Requires companies to identify and mitigate human rights and environmental risks

Applies to full supply chains, ensuring comprehensive oversight

Applies to EU companies with 1,000+ employees and €450 million+ global turnover and non-EU companies with over €450 million EU turnover

Mandates regular monitoring and reporting on due diligence efforts

Strengthens corporate accountability for sustainability across operations

This directive acknowledges that a company's sustainability impact extends beyond its direct operations, encompassing its entire value chain.

Status

CSDDD was adopted in April 2024. Its phased implementation is slated to start in June 2026 and be completed by June 2028. The timing and scope of CSDDD is subject to change following the Omnibus Proposal.

Carbon Border Adjustment Mechanism (CBAM)

The CBAM is an innovative approach to preventing carbon leakage. It levies a carbon tax on imports to ensure that the EU's ambitious climate policies do not simply shift carbon-intensive production outside its borders.

Key Aspects of CBAM

Imposes a carbon tax on imported goods

Requires importers to report emissions data

Ensures payment for embedded carbon costs in imported products

Aims to prevent carbon leakage to regions with weaker climate policies

This mechanism aims to create a level playing field for EU producers subject to carbon pricing while encouraging global partners to implement similar carbon pricing mechanisms.

Status

The transitional phase for CBAM began in October 2023, with full implementation scheduled for January 2026. It currently covers cement, iron and steel, aluminum, fertilizers, electricity, and hydrogen. The certificate requirements will phase in gradually from 30% in 2026 to 100% by 2034. It’s expected to apply to 1.8 million EU importers and generate €5-14 billion in annual revenue when fully implemented.

The February 2025 EU Omnibus Proposal

Purpose and Goals

The EU Omnibus Proposal represents a significant recalibration of the EU's regulatory approach, seeking to balance sustainability ambitions with business competitiveness concerns.

The primary objectives of the Omnibus focus on alleviating regulatory burdens faced by businesses, simplifying compliance requirements, and streamlining reporting obligations. These efforts aim to enhance business competitiveness while addressing regulatory complexity concerns. By minimizing these challenges, the goal is to create a more favorable environment for businesses to thrive. However, this push for simplification could come at the expense of transparency and accountability, especially in sectors where regulation plays a protective role.

Impact Analysis: How the Omnibus Changes ESG Compliance

Below, we’ll take a closer look at each regulation and the changes proposed by the Omnibus Proposal.

EU Taxonomy Modifications and Implications

The Omnibus Proposal suggests a Level 2 modification to the application of the EU Taxonomy, reducing the number of companies required to report taxonomy alignment.

Key Changes:

Taxonomy alignment reporting is limited to companies subject to CSDDD

Voluntary reporting option for companies not required to comply

Possible Implications:

Reduced availability of standardized sustainability data

Increased difficulty in verifying "green" business claims

Higher risk of greenwashing in financial markets

Less reliable information for sustainable investors

These modifications would potentially undermine the Taxonomy's role in creating a common language for sustainable activities.

CSRD Modifications and Implications

The Omnibus Proposal significantly narrows the scope of the CSRD, reducing the number of companies required to report on ESG impacts.

Key Changes:

Threshold increase from 250+ to 1,000+ employees

Optional reporting for SMEs

A two-year delay in reporting obligations for some companies

Possible Implications:

80% reduction in companies required to report

Decreased transparency in corporate sustainability performance

Fewer sustainability data available to investors and regulators

Potential challenges in tracking sustainability progress

These modifications would substantially reduce the regulatory burden on smaller companies but raise concerns about the availability of comprehensive sustainability data.

CSDDD Modifications and Implications

The Omnibus includes significant modifications to CSDDD, with a narrowed scope and reduced monitoring requirements.

Key Changes:

Due diligence is limited to direct suppliers with over 500 employees, not full supply chains

Monitoring frequency reduced from annual to every 5 years

Delayed enforcement for one year for the first batch (Companies with 1.5 billion in turnover and 5000 employees)

Possible Implications:

Weakened corporate accountability for supply chain sustainability

Increased risk of undetected human rights and environmental violations

Reduced monitoring of global supply chain impacts

Extended timeline before full implementation

These changes would significantly reduce companies' compliance burdens but come at the risk of removing the essence of the directive, which is eliminating child labor, forced labor, etc.

SFDR Modifications and Implications

While not directly modified, changes to other regulations, particularly the EU Taxonomy, indirectly affect the SFDR.

Indirect Impacts:

Reduced availability of reliable ESG data

Challenges in differentiating truly sustainable investments

Potential increase in greenwashing risk

These indirect effects could undermine the SFDR's effectiveness in bringing transparency to sustainable investment products.

CBAM Modifications and Implications

The Omnibus Proposal simplifies CBAM compliance, particularly for smaller importers.

Key Changes:

Small importers (under 50 metric tons/year) are exempted

Reduced reporting burden for over 182,000 businesses

Possible Implications:

Simplified compliance for small businesses

Potential loophole risk if companies split shipments to stay under the threshold

Maintained coverage of 99% of emissions despite exemptions

These modifications would maintain the CBAM's effectiveness while reducing the administrative burden on smaller importers.

The Debate: Perspectives on the Omnibus Proposal

Arguments in Favor

Proponents of the Omnibus Proposal emphasize its benefits for business competitiveness and regulatory efficiency. They highlight the reduced administrative burden, especially for small and medium-sized enterprises (SMEs), which often struggle with complex regulations. Additionally, the changes aim to simplify compliance requirements, making it easier for businesses to adhere to regulations. By aligning with global standards, the proposal helps maintain the EU's economic competitiveness while promoting a more efficient allocation of resources across industries. Together, these factors create a more streamlined and supportive environment for businesses to thrive.

As BusinessEurope Director General Markus J. Beyrer stated: "Doing better with fewer and clearer norms is what European companies of all sizes are asking for. By reducing unnecessary reporting and regulatory burdens, the first Omnibus will allow companies to contribute more effectively to the EU's sustainability objectives while also preserving the EU economy's competitiveness."

European Commission President Ursula von der Leyen also expressed support for the proposal, stating: "EU companies will benefit from streamlined rules. This will make life easier for our businesses while ensuring we stay firmly on course toward our decarbonization goals."

Criticisms and Concerns

Critics raise significant concerns about the potential undermining of the EU's sustainability ambitions. They argue that the Omnibus Proposal may lead to unintended consequences, including reduced transparency in corporate sustainability performance, weakened supply chain accountability, and regulatory uncertainty during transition periods. Additionally, it could undermine sustainability objectives and increase the risk of greenwashing. As Mariana Ferreira from WWF European Policy Office commented:

"The Commission's sudden urge to destroy laws that are crucial for the achievement of the EU Green Deal is a perilous approach that is forcing Europe into a time of regulatory uncertainty. Under the guise of 'simplification,' the Commission put forward a proposal that will hinder economic and business success."

"The Omnibus proposal erodes EU's corporate accountability commitments and slashes human rights and environmental protections."

While the European Parliament debates the Omnibus Proposal, the fact remains that even if the regulations are delayed or loosened, the need for risk management remains unchanged. Investors require transparency, and companies must manage supplier risk effectively.

Navigating ESG Risks with SESAMm

SESAMm’s cutting-edge AI solutions empower investors, financial institutions, and corporations to navigate the complexities of ESG compliance with confidence. Leveraging an industry-leading data lake and state-of-the-art AI, SESAMm uncovers hidden risks in supply chains and target companies, providing real-time insights that drive proactive decision-making. By transforming regulatory challenges into opportunities for responsible and sustainable growth, SESAMm helps businesses stay ahead of evolving ESG requirements while mitigating risk and enhancing transparency.

SESAMm’s AI Technology Reveals ESG Insights

Discover unparalleled insights into ESG controversies, risks, and opportunities across industries. Learn more about how SESAMm can help you analyze millions of private and public companies using AI-powered text analysis tools.

Stay ahead with the latest in ESG and AI intelligence

Join our mailing list to receive new reports, event invites, and updates from SESAMm directly to your inbox.

.avif)

.png)