The ESG Scorecard: A Deep Dive into Infrastructure Projects: Mines

September 4, 2025

•

5 mins read

Mining projects around the world often promise development and economic growth, yet their legacies reveal a far more complicated story. Sites like Cerrejón in Colombia, Córrego do Feijão and Samarco in Brazil show how environmental, social, and human rights risks can ripple through communities for decades. Rivers are poisoned, soils contaminated, and ecosystems devastated, while thousands of residents face health crises, displacement, and loss of livelihoods. Legal actions, class lawsuits, and ongoing remediation efforts illustrate that the consequences of these operations do not end when production stops. Communities continue to grapple with the aftermath, from toxic waste and tailings spills to the psychological scars of displacement and conflict.

What are the most pressing ESG challenges currently facing the mining sector? Read on to find out.

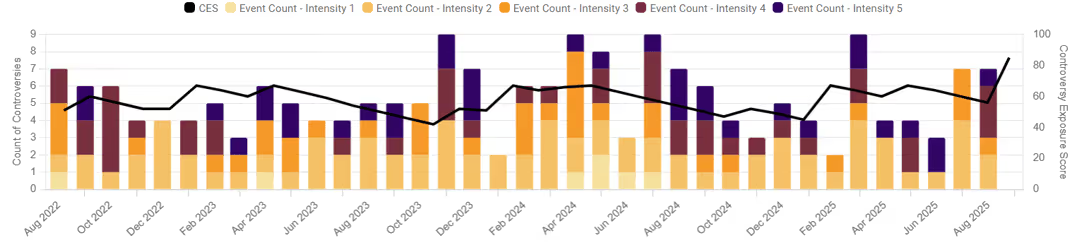

Córrego do Feijão Mine: ESG Challenges and Ongoing Controversies

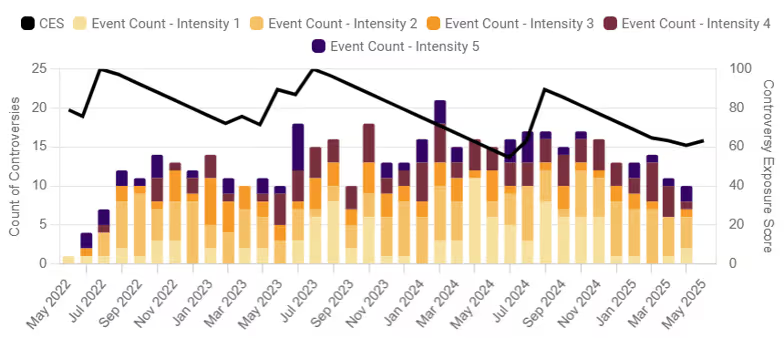

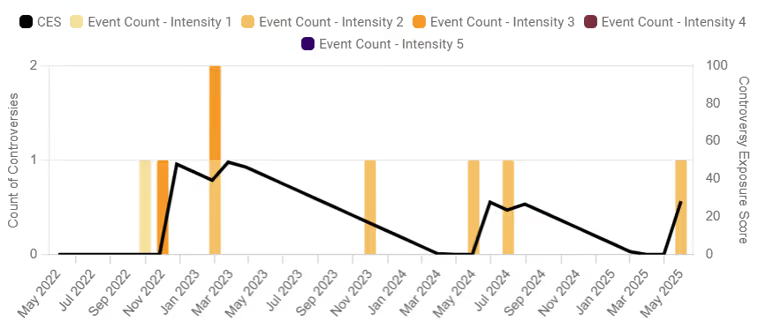

The Córrego do Feijão Mine is facing serious ESG controversies following a dam collapse that resulted in 270 fatalities and contamination of the Paraopeba River. Indigenous villagers still lack safe land and access to clean water and food. The operating company, Vale, is dealing with ongoing legal challenges, including fines and criminal charges for negligence and bribery. Environmental and social impacts persist, with continued monitoring of water quality and safety risks from existing dams. Governance issues remain significant, highlighted by employee arrests and scrutiny over manipulated audits, prompting calls from local and international NGOs for improved remediation efforts and oversight of the mine’s operations.

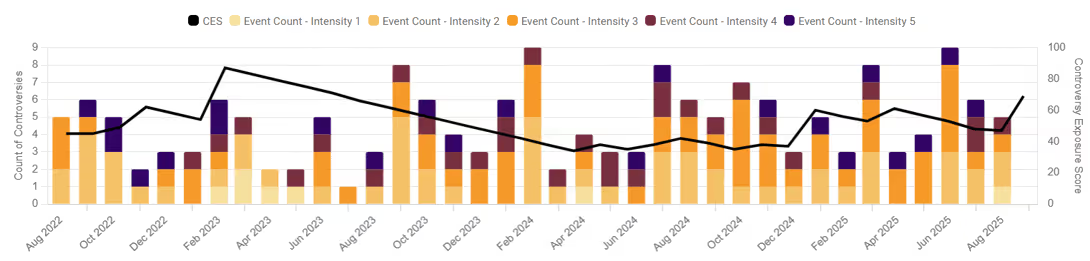

Cerrejon Mine: Human Rights, Health, and Environmental Impacts

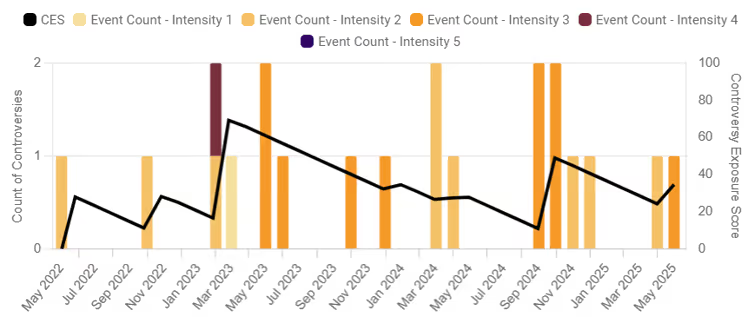

Cerrejón Mine faces significant ESG issues, particularly in environmental and social areas. Its expansion has displaced over 20,000 indigenous people, especially from the Wayúu community, leading to severe health problems and the deaths of 5,000 children. Environmental concerns include the diversion of the Bruno Stream, excessive water use during droughts, and significant air and water pollution. Labor unrest persists, with over 4,600 unionized workers striking over job cuts and unsafe conditions. The mine continues to face international criticism for violating local community rights and harming regional ecosystems.

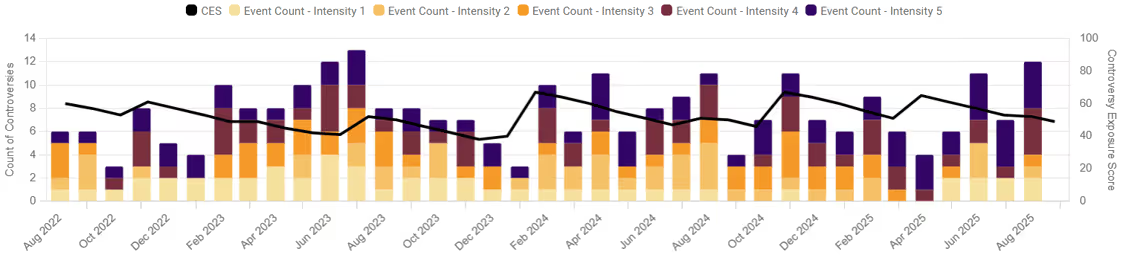

Samarco Mine: Escalating ESG Challenges and Corporate Accountability

Samarco Mine faces intense ESG scrutiny nearly a decade after the 2015 Fundão dam collapse, with over 700,000 claimants in a $44 billion lawsuit for contaminated water and pollution. The operator risks bankruptcy due to environmental liabilities and failed debt restructuring, exacerbating financial instability. Ongoing issues include heavy metal contamination in wildlife and dust pollution exceeding health standards, prompting NGOs to demand the operator's removal from the UN Global Compact. Governance concerns have risen with employee arrests linked to safety protocol violations and falsified audits, raising questions about corporate accountability.

The ongoing ESG challenges in the mining sector highlight significant environmental, social, and governance failures that profoundly impact affected communities. The cases of Córrego do Feijão, Cerrejón, and Samarco reveal the dire consequences of prioritizing profit over sustainability. Mining companies must embrace accountability, transparency, and community engagement to rebuild trust and ensure a positive impact.

Reach out to SESAMm

TextReveal’s web data analysis of over five million public and private companies is essential for keeping tabs on ESG investment risks. To learn more about how you can analyze web data or to request a demo, reach out to one of our representatives.

Infrastructure is no longer a niche allocation. It sits at the center of energy transition strategies, industrial policy, and long-term portfolio construction. For investors, banks, and insurers, exposure to infrastructure projects also means exposure to complex, evolving ESG and reputational risks.

More than 250,000 infrastructure projects worldwide are monitored on the SESAMm platform. This coverage continues to expand, with new projects added regularly, including in response to client requests.

“Infrastructure projects generate vast amounts of fragmented information across local media, regulatory sources, and public reporting. Our goal is to transform that information into structured intelligence. With more than 250,000 projects covered globally, SESAMm provides investors and financial institutions with the visibility needed to monitor infrastructure risks at scale,” commented Sylvain Forté, CEO & Co-Founder, SESAMm.

A Truly Global View of Infrastructure Risk

SESAMm analyzes sources in more than 100 languages and provides global visibility into infrastructure assets, including in emerging markets and jurisdictions with limited public disclosure. Through multilingual AI analysis, SESAMm monitors projects in their local information environments, detecting controversies, regulatory actions, environmental incidents, corruption cases, and governance failures as they emerge.

Whether a project is located in Europe, Southeast Asia, Sub-Saharan Africa, or Latin America, clients gain access to:

Local-language media monitoring

Structured ESG event detection

Clear visibility into how events evolve over time

Severity and exposure scoring

Infrastructure risk is rarely static. It evolves during permitting, construction, operation, and financing, and SESAMm’s monitoring reflects that reality.

Coverage Across Key Infrastructure Categories

SESAMm’s infrastructure coverage includes a wide range of asset types, such as:

Solar Stations

Airports

Waste Management Facilities

Wind Stations

Dams

Coal Mines

Oil & Gas Plants

Hydropower Stations

Coal Power Stations

Steel Plants

Bioenergy Stations

Nuclear Stations

Coal Terminals

Geothermal Stations

This breadth enables clients to assess risks across both legacy and transition-aligned infrastructure.

Why Infrastructure Monitoring Matters Now

Infrastructure projects concentrate risk. They involve long timelines, large capital commitments, public scrutiny, regulatory complexity, and significant community impact.

For investors and lenders, point-in-time due diligence is no longer sufficient. A project cleared at financial close can face protests, litigation, environmental incidents, corruption allegations, or regulatory breaches years later.

Continuous monitoring is becoming essential for:

Pre-investment screening

Ongoing portfolio oversight

Secondaries transactions

Infrastructure debt underwriting

Insurance risk assessment

Sustainability and SFDR reporting

Our expanded coverage supports these workflows with structured, real-time intelligence.

On-Demand Expansion: Coverage That Grows With You

Beyond the projects already included in the dataset, SESAMm adds new infrastructure assets upon client request. This allows coverage to align directly with a pipeline of acquisition targets, a lender’s financing book, an insurer’s underwriting portfolio, or a fund’s watchlist. Rather than forcing clients to adapt to a fixed database, SESAMm’s infrastructure coverage scales dynamically to meet their needs.

With more than 250,000 assets included, SESAMm delivers one of the most comprehensive and scalable datasets for infrastructure risk monitoring. Together, this expanded infrastructure dataset and SESAMm’s AI reporting capabilities provide financial institutions with a scalable way to identify and monitor risks across infrastructure portfolios worldwide.

The European Union stands at the forefront of global efforts to promote environmental, social, and governance (ESG) accountability. As the world becomes increasingly ESG-aware, the EU has developed a comprehensive regulatory framework designed to ensure transparency and accountability across all sectors.

These regulations represent the EU's commitment to sustainable development and responsible business practices. However, the regulatory landscape is evolving, with the February 2025 EU Omnibus Proposal introducing potential modifications aimed at reducing the regulatory burden on businesses. However, these proposals come at the risk of substantially undercutting the impact of the regulations.

This article recaps the current ESG regulatory framework in the EU, explores the changes proposed by the Omnibus, analyzes the potential impacts of these modifications, and discusses how financial institutions can navigate this evolving landscape while maintaining compliance.

The ESG Regulatory Landscape in the EU

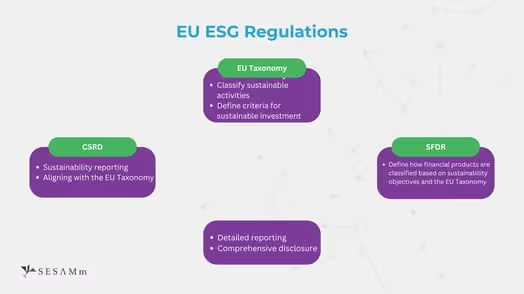

The EU is advancing sustainability through a framework of regulations that enhance corporate accountability and reporting on ESG impacts. These measures aim to promote genuine sustainable practices and address international trade and emissions challenges. Though comprehensive, these regulations are also, at times, confusing in the way they overlap and impact each other. To get started, let’s examine the EU Taxonomy, SFDR, and CSRD—a triad of interconnected regulations designed to streamline and strengthen sustainable investing practices.

EU Taxonomy

The EU Taxonomy provides a classification system for environmentally sustainable economic activities, offering clear criteria to determine whether an economic activity can be considered "green."

Key Aspects of the EU Taxonomy

Defines criteria for environmentally sustainable economic activities

Requires companies subject to CSRD to report on Taxonomy alignment

The Taxonomy helps channel investment toward genuinely sustainable projects and businesses by creating a common language for sustainable activities.

Status

The EU Taxonomy has been operational since January 2022 with phased implementation. As of March 2025, companies subject to CSRD must disclose their taxonomy alignment percentages.

Sustainable Finance Disclosure Regulation (SFDR)

The SFDR focuses specifically on the financial sector, requiring financial market participants to disclose how they integrate ESG risks into their investment decisions and the sustainability impact of their financial products.

Key Aspects of SFDR

Requires disclosure of ESG risks in investment processes

Classifies financial products based on their sustainability characteristics

Aligns with EU Taxonomy criteria for sustainable investments

Aims to prevent greenwashing in financial products

The SFDR plays a crucial role in bringing transparency to the rapidly growing sustainable investment market.

Status

Fully implemented since March 2021, with enhanced Level 2 requirements since January 2023. All EU financial market participants must classify products under Articles 6, 8, or 9. Current market data shows that 28% of EU funds are compliant with Article 8 and 5% with Article 9, with a significant trend of reclassification from Article 9 to 8 due to stricter interpretations.

The CSRD stands as a cornerstone of the EU's ESG regulatory framework, requiring companies to report comprehensively on their environmental, social, and governance impacts. This directive mandates alignment with the EU Taxonomy, ensuring standardized reporting of sustainability metrics.

Key Aspects of CSRD

Requires detailed reporting on ESG impacts

Aligns with EU Taxonomy criteria for sustainability

Currently applies to companies with 250+ employees

Enhances corporate transparency on sustainability issues

The CSRD represents a significant step forward in standardizing sustainability reporting across the EU, providing investors, consumers, and regulators with comparable information on corporate sustainability performance.

Status

The CSRD, adopted in November 2022, replaces the Non-Financial Reporting Directive (NFRD). The transition to CSRD reporting was originally slated to begin in 2025 and would expand the number of companies subject to reporting requirements to 49,000 (vs 11,700 under NFRD). However, as we’ll see later, the Omnibus may push back the timing of CSRD.

Outside of the EU Taxonomy, SFDR, and CSRD, the Omnibus Proposal highlights two other key ESG regulations: CSDDD and CBAM. These regulations relate to corporate accountability for supply chains and to limiting carbon leakage.

Corporate Sustainability Due Diligence Directive (CSDDD)

The CSDDD focuses on corporate accountability throughout global supply chains, requiring companies to identify, prevent, and mitigate human rights and environmental risks associated with their operations.

Key Aspects of CSDDD

Requires companies to identify and mitigate human rights and environmental risks

Applies to full supply chains, ensuring comprehensive oversight

Applies to EU companies with 1,000+ employees and €450 million+ global turnover and non-EU companies with over €450 million EU turnover

Mandates regular monitoring and reporting on due diligence efforts

Strengthens corporate accountability for sustainability across operations

This directive acknowledges that a company's sustainability impact extends beyond its direct operations, encompassing its entire value chain.

Status

CSDDD was adopted in April 2024. Its phased implementation is slated to start in June 2026 and be completed by June 2028. The timing and scope of CSDDD is subject to change following the Omnibus Proposal.

Carbon Border Adjustment Mechanism (CBAM)

The CBAM is an innovative approach to preventing carbon leakage. It levies a carbon tax on imports to ensure that the EU's ambitious climate policies do not simply shift carbon-intensive production outside its borders.

Key Aspects of CBAM

Imposes a carbon tax on imported goods

Requires importers to report emissions data

Ensures payment for embedded carbon costs in imported products

Aims to prevent carbon leakage to regions with weaker climate policies

This mechanism aims to create a level playing field for EU producers subject to carbon pricing while encouraging global partners to implement similar carbon pricing mechanisms.

Status

The transitional phase for CBAM began in October 2023, with full implementation scheduled for January 2026. It currently covers cement, iron and steel, aluminum, fertilizers, electricity, and hydrogen. The certificate requirements will phase in gradually from 30% in 2026 to 100% by 2034. It’s expected to apply to 1.8 million EU importers and generate €5-14 billion in annual revenue when fully implemented.

The February 2025 EU Omnibus Proposal

Purpose and Goals

The EU Omnibus Proposal represents a significant recalibration of the EU's regulatory approach, seeking to balance sustainability ambitions with business competitiveness concerns.

The primary objectives of the Omnibus focus on alleviating regulatory burdens faced by businesses, simplifying compliance requirements, and streamlining reporting obligations. These efforts aim to enhance business competitiveness while addressing regulatory complexity concerns. By minimizing these challenges, the goal is to create a more favorable environment for businesses to thrive. However, this push for simplification could come at the expense of transparency and accountability, especially in sectors where regulation plays a protective role.

Impact Analysis: How the Omnibus Changes ESG Compliance

Below, we’ll take a closer look at each regulation and the changes proposed by the Omnibus Proposal.

EU Taxonomy Modifications and Implications

The Omnibus Proposal suggests a Level 2 modification to the application of the EU Taxonomy, reducing the number of companies required to report taxonomy alignment.

Key Changes:

Taxonomy alignment reporting is limited to companies subject to CSDDD

Voluntary reporting option for companies not required to comply

Possible Implications:

Reduced availability of standardized sustainability data

Increased difficulty in verifying "green" business claims

Higher risk of greenwashing in financial markets

Less reliable information for sustainable investors

These modifications would potentially undermine the Taxonomy's role in creating a common language for sustainable activities.

CSRD Modifications and Implications

The Omnibus Proposal significantly narrows the scope of the CSRD, reducing the number of companies required to report on ESG impacts.

Key Changes:

Threshold increase from 250+ to 1,000+ employees

Optional reporting for SMEs

A two-year delay in reporting obligations for some companies

Possible Implications:

80% reduction in companies required to report

Decreased transparency in corporate sustainability performance

Fewer sustainability data available to investors and regulators

Potential challenges in tracking sustainability progress

These modifications would substantially reduce the regulatory burden on smaller companies but raise concerns about the availability of comprehensive sustainability data.

CSDDD Modifications and Implications

The Omnibus includes significant modifications to CSDDD, with a narrowed scope and reduced monitoring requirements.

Key Changes:

Due diligence is limited to direct suppliers with over 500 employees, not full supply chains

Monitoring frequency reduced from annual to every 5 years

Delayed enforcement for one year for the first batch (Companies with 1.5 billion in turnover and 5000 employees)

Possible Implications:

Weakened corporate accountability for supply chain sustainability

Increased risk of undetected human rights and environmental violations

Reduced monitoring of global supply chain impacts

Extended timeline before full implementation

These changes would significantly reduce companies' compliance burdens but come at the risk of removing the essence of the directive, which is eliminating child labor, forced labor, etc.

SFDR Modifications and Implications

While not directly modified, changes to other regulations, particularly the EU Taxonomy, indirectly affect the SFDR.

Indirect Impacts:

Reduced availability of reliable ESG data

Challenges in differentiating truly sustainable investments

Potential increase in greenwashing risk

These indirect effects could undermine the SFDR's effectiveness in bringing transparency to sustainable investment products.

CBAM Modifications and Implications

The Omnibus Proposal simplifies CBAM compliance, particularly for smaller importers.

Key Changes:

Small importers (under 50 metric tons/year) are exempted

Reduced reporting burden for over 182,000 businesses

Possible Implications:

Simplified compliance for small businesses

Potential loophole risk if companies split shipments to stay under the threshold

Maintained coverage of 99% of emissions despite exemptions

These modifications would maintain the CBAM's effectiveness while reducing the administrative burden on smaller importers.

The Debate: Perspectives on the Omnibus Proposal

Arguments in Favor

Proponents of the Omnibus Proposal emphasize its benefits for business competitiveness and regulatory efficiency. They highlight the reduced administrative burden, especially for small and medium-sized enterprises (SMEs), which often struggle with complex regulations. Additionally, the changes aim to simplify compliance requirements, making it easier for businesses to adhere to regulations. By aligning with global standards, the proposal helps maintain the EU's economic competitiveness while promoting a more efficient allocation of resources across industries. Together, these factors create a more streamlined and supportive environment for businesses to thrive.

As BusinessEurope Director General Markus J. Beyrer stated: "Doing better with fewer and clearer norms is what European companies of all sizes are asking for. By reducing unnecessary reporting and regulatory burdens, the first Omnibus will allow companies to contribute more effectively to the EU's sustainability objectives while also preserving the EU economy's competitiveness."

European Commission President Ursula von der Leyen also expressed support for the proposal, stating: "EU companies will benefit from streamlined rules. This will make life easier for our businesses while ensuring we stay firmly on course toward our decarbonization goals."

Criticisms and Concerns

Critics raise significant concerns about the potential undermining of the EU's sustainability ambitions. They argue that the Omnibus Proposal may lead to unintended consequences, including reduced transparency in corporate sustainability performance, weakened supply chain accountability, and regulatory uncertainty during transition periods. Additionally, it could undermine sustainability objectives and increase the risk of greenwashing. As Mariana Ferreira from WWF European Policy Office commented:

"The Commission's sudden urge to destroy laws that are crucial for the achievement of the EU Green Deal is a perilous approach that is forcing Europe into a time of regulatory uncertainty. Under the guise of 'simplification,' the Commission put forward a proposal that will hinder economic and business success."

"The Omnibus proposal erodes EU's corporate accountability commitments and slashes human rights and environmental protections."

While the European Parliament debates the Omnibus Proposal, the fact remains that even if the regulations are delayed or loosened, the need for risk management remains unchanged. Investors require transparency, and companies must manage supplier risk effectively.

Navigating ESG Risks with SESAMm

SESAMm’s cutting-edge AI solutions empower investors, financial institutions, and corporations to navigate the complexities of ESG compliance with confidence. Leveraging an industry-leading data lake and state-of-the-art AI, SESAMm uncovers hidden risks in supply chains and target companies, providing real-time insights that drive proactive decision-making. By transforming regulatory challenges into opportunities for responsible and sustainable growth, SESAMm helps businesses stay ahead of evolving ESG requirements while mitigating risk and enhancing transparency.

SESAMm’s AI Technology Reveals ESG Insights

Discover unparalleled insights into ESG controversies, risks, and opportunities across industries. Learn more about how SESAMm can help you analyze millions of private and public companies using AI-powered text analysis tools.

The educational technology (EdTech) sector, including companies like Udemy, Coursera, and Byju's, has grown rapidly but faces major social and governance challenges. Key issues include costly legal battles over privacy violations and deceptive practices, which raise investor concerns. Financial instability is also prevalent, with layoffs and bankruptcies highlighting doubts about workforce rights and sustainable business models. While some companies manage ESG issues better, operational inefficiencies remain a concern for long-term stability. What are the most pressing ESG challenges currently facing the EdTech sector? Read to find out.

BYJU’S: Treading Turbulent Waters Amidst Financial and Regulatory Challenges

Byju’s, an EdTech startup in India, has faced significant challenges since 2022. The company has dealt with controversies, including data breaches, financial mismanagement, and regulatory investigations. Key issues include the shutdown of its Kerala office, mass layoffs, allegations of Goods and Services Tax evasion, and defaults on loan payments. In 2023 and 2024, Byju's continued to struggle with layoffs, money laundering investigations, and the resignation of executives. As of 2024, the company is at risk of insolvency, with ongoing bankruptcy proceedings and regulatory action against its leadership, highlighting its financial instability after years of rapid growth.

Udemy: Battling Legal and Ethical Challenges in the E-Learning Landscape

Udemy, a leading e-learning platform, has encountered increasing legal, financial, and operational challenges. These include a settlement over deceptive pricing practices, antitrust issues leading to a board member's resignation, and multiple lawsuits related to Facebook data sharing and video privacy violations. The company has also restructured its workforce to streamline operations and faced concerns over its generative AI policy regarding consent and transparency among instructors. These controversies highlight the complexities faced by EdTech companies in navigating legal and ethical challenges.

Coursera: Navigating Challenges in Security, Ethics, and Workforce Dynamics

Coursera, another widely used online learning platform, has faced relatively few controversies as reflected by its Controversy Exposure Score. However, a few noteworthy challenges include security vulnerabilities, AI use, an investigation into misleading financial statements, and workforce reductions due to declining growth. The company is dealing with a class action lawsuit over subscription renewals and a data privacy lawsuit for sharing customer viewing history with Meta. Coursera also faces controversies related to AI, in this case on AI-powered tools for grading, providing feedback, and course-building, promising greater efficiency but raising questions about transparency and ethics. Finally, as part of restructuring, Coursera plans to cut its global workforce.

Each of these companies illustrates the growing ESG challenges in the EdTech sector. From maintaining data privacy and ethical AI use to ensuring sound governance, financial sustainability, and fair treatment of employees and customers, Udemy, Coursera, and BYJU’S all face heightened scrutiny. Recent controversies and operational troubles highlight the need for robust risk management as education technology firms mature on the global stage. The ESG risks – whether legal, social, or governance-related – not only threaten their reputations but also have material impacts on their long-term viability. By addressing these issues transparently and proactively, EdTech companies can work toward a more sustainable and responsible growth trajectory in the years ahead.

Reach out to SESAMm

TextReveal’s web data analysis of over five million public and private companies is essential for keeping tabs on ESG investment risks. To learn more about how you can analyze web data or to request a demo, reach out to one of our representatives.

Stay ahead with the latest in ESG and AI intelligence

Join our mailing list to receive new reports, event invites, and updates from SESAMm directly to your inbox.

_11zon.jpg)

.avif)

.png)