BNP Paribas Crosses 80% Low-carbon Energy Financing Milestone

02/12/2026

•

5 mins read

BNP Paribas has passed a significant milestone in its energy financing strategy, with more than 80% of its energy production financing now directed toward low-carbon energies.

The increase marks a notable acceleration compared with previous periods. Low-carbon energy financing accounted for approximately 65% of BNP Paribas’ energy production exposure in 2023, rising to around 76% in 2024, before surpassing the 80% threshold in 2025. The category includes renewable energy sources such as wind, solar and hydropower, as well as nuclear energy, which the bank classifies as low-carbon.

At the same time, BNP Paribas has continued to reduce its exposure to fossil fuel energy production. Credit exposure linked to oil and gas projects has declined as financing volumes for renewables and other low-carbon technologies increased, reflecting the bank’s longer-term commitment to rebalancing its energy portfolio in line with climate objectives. Beyond energy production financing, the bank has also reported progress against its broader transition finance ambitions. By the end of 2025, BNP Paribas had mobilized more than €250 billion in financing supporting the low-carbon transition, exceeding its initial €200 billion target ahead of schedule. The bank has since confirmed updated objectives, including a target to reach 90% low-carbon energy financing by 2030.

While the figures relate specifically to energy production financing exposure, rather than BNP Paribas’ total lending activity, they nonetheless highlight the pace at which large financial institutions are reshaping their energy strategies. As regulatory scrutiny, investor expectations, and transition risks continue to intensify, the composition of energy financing portfolios is increasingly viewed as a key indicator of alignment with long-term climate goals.

Chinese companies face elevated ESG risk exposure as scale, rapid growth, and cross-border operations intersect with tighter regulations and geopolitical pressures. Social risks cluster around worker rights and customer harm: “996” overwork and layoffs in tech, safety failures in new technologies and EVs, and severe labor allegations in global supply chains.

Governance risks are the dominant theme, reflected across multiple jurisdictions and industry sectors: recurring regulatory enforcement and compliance failures, litigation-heavy operating models, weak internal controls, and heightened disclosure, audit, and listing pressure in overseas markets. A major amplifier is data-security and national-security risk, with allegations of illegal data collection or leaks and intensifying foreign scrutiny over potential military ties and state influence.

Environmental risks cluster around manufacturing pollution and emissions compliance, alongside chemical-product safety and carbon-intensive logistics footprints in fast fashion and e-commerce.

What are the most pressing ESG challenges currently facing Chinese companies? Read on to find out.

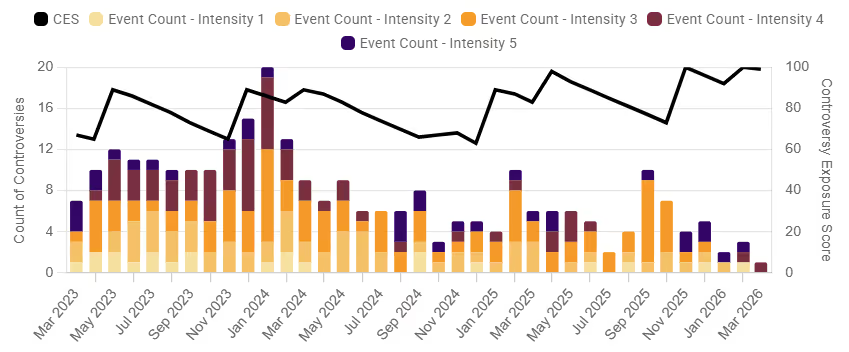

Alibaba: Navigating Controversies and Governance Challenges

In parallel, integrity and geopolitical risks heighten scrutiny, notably through a police investigation into alleged supply-chain corruption at Ele.me, U.S. probes related to data privacy and alleged military links, and a $433.5 million investor lawsuit recovery. Environmental exposure remains primarily supply-chain and footprint-driven, including a 2025 pesticide finding and emissions-related criticism in Belgium. Based on SESAMm’s UNGC screening, we found that several of Alibaba’s controversies show potential alignment concerns with UN Global Compact principles, reinforcing the need for continuous monitoring.

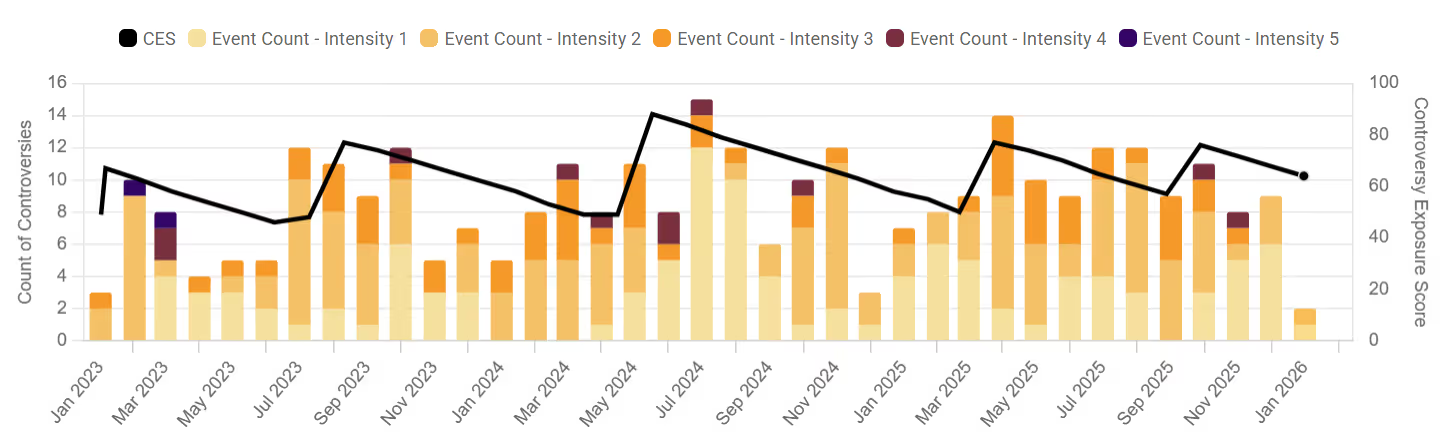

Shein: Heavy ESG Scrutiny Amid Legal and Environmental Challenges

Similarly, Shein faces sustained ESG pressures across governance, environmental, and social dimensions, reflected in its high CES of 89/100, indicating material and ongoing exposure. Social risks include allegations of exploitative factory conditions,disclosed child-labor cases, and reputational backlash linked to cultural appropriation and marketing practices, alongside integrity concerns such as reported coordinated bot activity to defend the brand online.

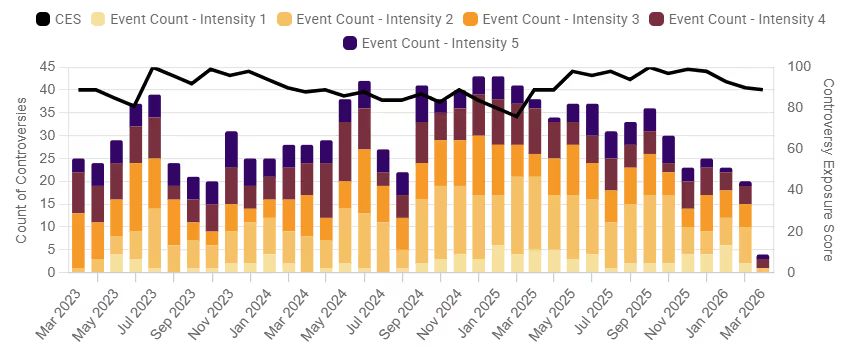

BYD: Risks and Controversies Demand Ongoing Monitoring

BYD’s ESG profile reflects sustained controversy exposure, with a CES score of 89/100, indicating material and ongoing risk. Social risks include product-safety concerns, notably the Atto 3 receiving the lowest-ever assisted-driving safety score and a recall of more than 16,000 EVs; more critically, Brazilian authorities shut down a factory site over alleged “slavery-like” labor conditions and battery mineral sourcing linked to human-rights abuses, culminating in a $50 million lawsuit.

Governance risks are cross-border and multifaceted, spanning tax-fraud allegations, IP disputes such as BMW’s “M6” trademark case, EU scrutiny over potential unfair Chinese subsidies at BYD’s Hungary plant, concerns in South Korea regarding possible in-vehicle data leakage, a securities-fraud investigation notice, and U.S. designation activity linking BYD to Chinese military-affiliated entities. Meanwhile, environmental exposure centers on factory pollution at Changsha tied to reported health impacts and heightened emissions-compliance scrutiny following accusations of emissions cheating.

From a UNGC perspective, a number of BYD’s controversies show potential alignment concerns with UN Global Compact principles, particularly around labor rights and governance, and reinforcing the importance of ongoing monitoring.

Conclusion

Taken together, Alibaba, Shein, and BYD illustrate how scale, speed, and global expansion can amplify ESG exposure when governance, labor oversight, and compliance controls lag behind operational growth. High CES scores across all three companies underscore that these risks are not isolated incidents but structural and recurring in nature.

SESAMm Welcomes Industry Expert Stéphane Besson to Its Board of Directors

SESAMm is thrilled to welcome Stéphane Besson as the newest member of its board of directors. Stéphane is a seasoned expert in the finance industry with a rich background that includes BNPP and McKinsey. He has a notable track record, most prominently as the CEO of Coalition Greenwich for more than ten years. Under Stephane’s leadership, Coalition Greenwich, part of S&P, flourished to become the leader in providing strategic insights and analytics to the financial sector across Banks and Asset Managers.

“We are absolutely delighted to have Stéphane join our team. His remarkable journey in scaling Coalition Greenwich and advisory roles in several companies make him an ideal addition to SESAMm. His insights and strategic acumen will be incredibly valuable as we continue to expand our reach, especially in the European market where we have established a strong presence, and as we aim to increase our footprint in the US market,” commented Sylvain Forté, SESAMm’s CEO & Co-founder.

In his new role at SESAMm, Stéphane will not only be a board member but also an active strategic advisor. He currently also holds positions on Accelex and Acin boards and serves as chairman at Validis. His extensive experience guiding Coalition Greenwich's growth and advising various firms aligns perfectly with SESAMm’s mission. SESAMm, having recently secured $37MM in funding, is at a pivotal growth phase. The company specializes in leveraging AI to detect ESG controversies in public and private companies,

“I am very excited to join SESAMm. The quality of the team and their vision to bring more transparency to the ESG space convinced me immediately. I am looking forward to helping them deliver on their vision for their clients and the industry more broadly.” said Stéphane.

Stéphane's addition to the board is a testament to SESAMm's commitment to excellence and growth in AI-powered ESG insights. His strategic insights will contribute significantly to guiding SESAMm's growth in the global market.

The ESG landscape for U.S. private equity firms is increasingly defined by systemic governance pressure and rising social and environmental scrutiny. Governance issues at firms such as Blackstone, KKR, Thoma Bravo, TPG, and Francisco Partners primarily focus on deal processes, disclosure practices, and investor protection. These concerns encompass settlements related to pension mismanagement, actions taken by the Department of Justice regarding pre-merger filings, as well as lawsuits and shareholder investigations examining the fairness of take-private transactions and stock buybacks. On the social side, exposure is driven largely by portfolio companies and political positioning. Housing and tenant-rights disputes sit alongside allegations of labor abuses, child labor, and unsafe conditions. Environmental concerns are increasingly prominent, with major companies facing criticism for their exposure to fossil fuels, their impact on climate change, and associated lobbying efforts.

What are the most pressing ESG challenges currently facing the U.S. private equity firms? Read on to find out.

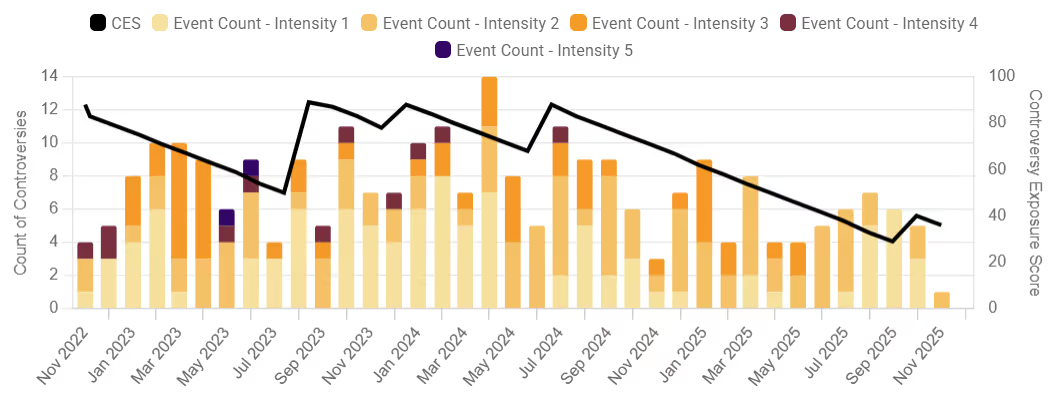

Blackstone: Governance Pressure, Social Backlash, and Climate Criticism

Blackstone is facing a wide range of ESG controversies. Governance challenges include a $227.5 million settlement related to Kentucky pension mismanagement, a $590 million lawsuit involving SPAC Recovery Co. that alleges a fraudulent scheme, and SEC fines tied to off-channel communications failures. On the social front, the firm has drawn criticism for political spending that heavily favors right-leaning candidates, child-labor incidents, and recurring safety violations at portfolio companies. Housing-related concerns also persist, with tenant protests over rent and eviction practices and university movements calling for divestment from Blackstone-linked real estate funds. Environmentally, Blackstone continues to be targeted by climate activists for its fossil fuel exposure and its perceived contribution to escalating climate risks.

TextReveal’s web data analysis of over five million public and private companies is essential for keeping tabs on ESG investment risks. To learn more about how you can analyze web data or to request a demo, reach out to one of our representatives.

Stay ahead with the latest in ESG and AI intelligence

Join our mailing list to receive new reports, event invites, and updates from SESAMm directly to your inbox.

.png)