Webinar Replay: AI in ESG Due Diligence: Best Practices from Indefi and SESAMm

July 18, 2024

•

5 mins read

We recently held an insightful webinar co-hosted by Charlotte Salmon of Indefi and Alejandro Plaza of SESAMm, titled "AI in ESG Due Diligence: Best Practices from Indefi and SESAMm." The session explored the innovative application of artificial intelligence in the ESG risk assessment process.

During the webinar, Charlotte and Alejandro discussed how Indefi's proven strategies, when combined with SESAMm's cutting-edge AI platform, can significantly enhance ESG risk management and the selection of target companies. One of the key highlights was a detailed case study on major delivery apps, including Glovo, Uber Eats, DoorDash, Deliveroo, Grubhub, and Just Eat. This segment covered industry and competitive analysis, sentiment analysis, and a deep dive into ESG controversies and positive SDG impacts associated with these companies.

Key Topics Covered:

Due diligence process for ESG risk assessment

AI integration in ESG risk management

Selection of target companies

Delivery apps case study: industry and competitive analysis, sentiment analysis, and deep dives into ESG controversies and SDG positive impacts

Don't miss out on this opportunity to learn from industry leaders about the future of ESG due diligence. Watch the full webinar replay:

Wednesday, September 14, 2022, a16z (Andreessen Horowitz), a large, well-known VC firm, funded Flow, a new startup led by a seemingly scandalous entrepreneur, Adam Neumann, the founder infamously known to have been ousted as WeWork CEO.

Why did a16z invest in Flow and, by proxy, Adam Neumann?

In his blog post about “Investing in Flow,” Andreessen acknowledges the U.S. housing crisis in the first sentence, and here’s what he has to say about Neumann: “Adam is a visionary leader who revolutionized the second largest asset class in the world—commercial real estate—by bringing community and brand to an industry in which neither existed before.” Andreessen continues, “[I]t’s often underappreciated that only one person has fundamentally redesigned the office experience and led a paradigm-changing global company in the process.”

So that gives us a clue as to what Andreessen thinks. But what does the public web have to say, and what is its overall sentiment?

In this edition of Alternative Data Trends, we dig into public web data before, during, and after a16z announced that it would fund Flow. Does the public web agree with Andreesen’s view? If not, how does it differ? And how can this information inform an investor and other VC firms?

Let’s find out.

a16z web mention volume and polarity (Nov. 2015 to Jun. 2022)

Figure 1: Andreessen Horowitz mention volume and polarity chart.

Mention volumes spike in mid-June 2021

TextReveal® uncovered 181,620 articles and messages from SESAMm’s data lake about Andreessen Horowitz (Figure 1). Mention volume remains consistent until late 2020, at which time a16z invests in a bunch of new companies and startups, such as:

Beacons

Clubhouse

Dapper Labs

Eco

Helium

Labster

Maven

Nansen

OpenSea

Skydio

SpotOn

Tackle.io

Valon

Zus Health

a16z also focused on the NFT market and, as a result, launched the world’s biggest crypto-fund valued at $2.2 Billion in June 2021. Moreover, Andreessen Horowitz launched its own media property, Future.com, in mid-2021.

Andreessen Horowitz web mentions further spike after it doubles down, announcing $4.5B crypto fund IV in May 2022. Additional news increased mention volume because of its investment in Neumann’s new startups, Flowcarbon and Flow.

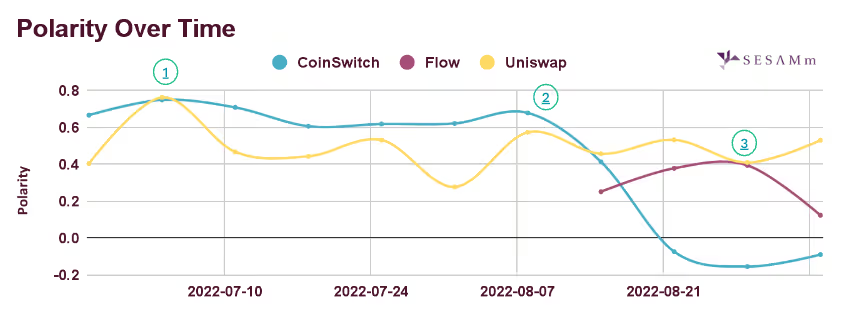

Polarity (positive and negative sentiment) dips

Sentiment toward a16z remained relatively stable over time with only minor dips until mid-2021, when it began falling, a trend driven by mentions of Flow investments news, the Uniswap related lawsuit, and suspected CoinSwitch Forex law violations (Figure 2).

Figure 2: Uniswap and CoinSwitch events affected a16z’s polarity as early as July 2022. As it rebounded, Flow began influencing polarity negatively by mid-August.

Why was Flow affecting a16z’s polarity so much?

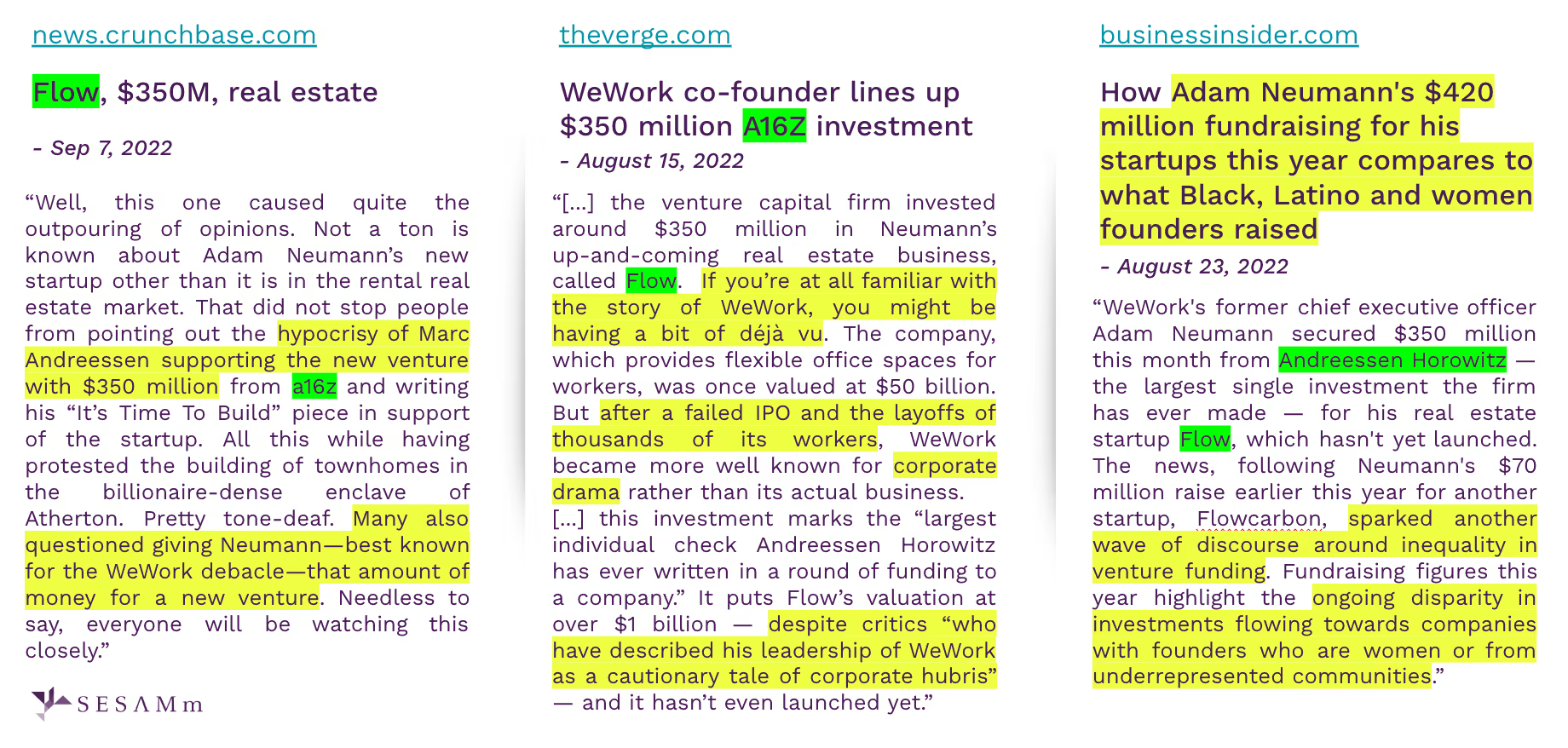

Figure 3: Newsclips about a16z investing in Flow.

Despite Andreessen’s reasons for giving Flow and Neumann a chance, the public’s opinion seems to disagree, leaning toward a negative sentiment (Figure 3). Overall, the public doesn’t seem to trust that Neumann is worth a second chance and that his choices are beyond forgiving. Moreover, the public criticizes a16z’s choice to overlook women and people of color. This The Guardian article highlights tweets of these differences in opinion:

In summary, TextReveal’s web data analysis tells us that it’s essential to keep an eye on the latent ESG risks this investment could bring to a16z’s portfolio, particularly on the social side.

Andreessen Horowitz, from an ESG perspective

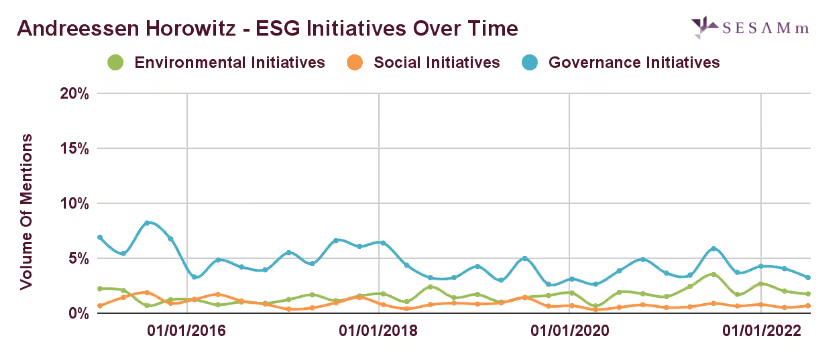

a16z ESG initiatives

Figure 4: a16z’s governance initiatives exceed environmental and social.

From a mention volume perspective, a16z’s ESG initiative numbers remain stable (Figure 4). Andreessen Horowitz has a good share of ESG initiatives shares with the highest percentage for governance driven by partnerships and collaborations, followed by the environmental aspect that has been increasing over the last two years.

ESG risks, from a portfolio perspective

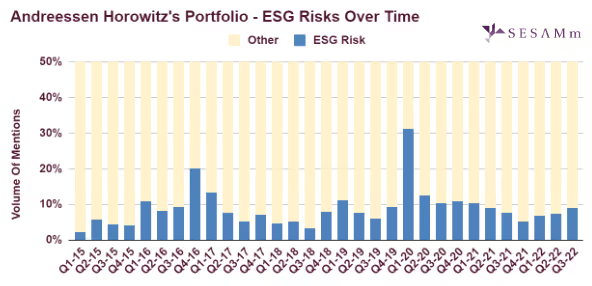

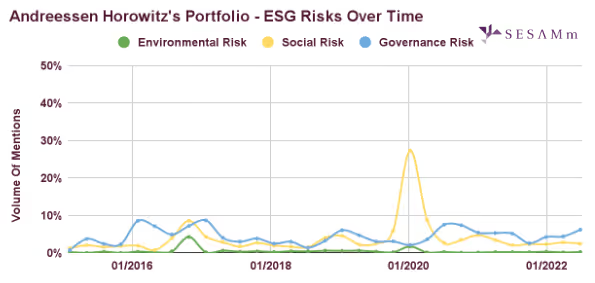

Figure 5: a16z’s aggregated portfolio’s ESG risks over time.

Figure 6: a16z’s portfolio’s social risk spikes in January 2020.

Figures 5 and 6 cover 160 companies in Andreessen Horowitz’s portfolio in the venture and growth stage. Overall, a16z’s portfolio represents a lower ESG risk (<15%) over time, except for the occasional moderately higher ESG risks score (<35%) indicated by two prominent spikes, one at the end of 2016 (Q4) and the second at the beginning of the year 2020 during the pandemic (Q1). The first spike is mainly a governance risk related to Soylent’s products being recalled and supply-chain-shortage risks. The spike is also caused by another top executive resigning from Magic Leap. In contrast, the second spike is a social risk driven by Instacart’s employees’ strike upon working conditions and safety concerns during the Covid-19 pandemic.

Note: Very low risk is <5%, low risk is <15%, moderate risk is <=35%, high risk is <=50%, and very high risk is >50%. Also, note that this scale is for demonstration only and does not indicate actual risk values.

Figure 7: A deeper look into the top companies in a16z’s portfolio generating mention volumes shows Instacart and MakerDAO in the moderate risk range. In contrast, the others are low to very low in risk in comparison.

Does the public’s view of a16z’s investment of Flow have merit?

Maybe, maybe not.

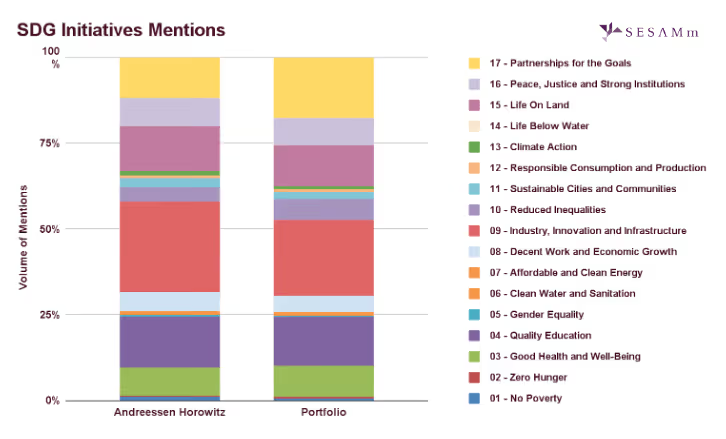

Looking at Andreessen Horowitz’s company and portfolio through the lens of web data, it is, if anything, consistent with its ESG initiatives and has experienced very few controversies. Should investors ignore the potential red flags that come with Flow and Adam Neumann? Of course not. But they should feel assured that a16z has exhibited a pattern of making sound investments. For example, if we compare the firm’s SDG initiatives to those in its portfolio (Figure 8), they are almost identical.

Figure 8: Andreessen Horowitz portfolio companies are focusing on the Sustainable Development Goals with specific attention toward goal 9: Industry, Innovation, and Infrastructure and Goal 17: Partnerships for the Goals, followed by Goal 4: Quality Education and Goal 15: Life On Land.

It’s possible that maybe Marc Andreessen and a16z et al. see something in Flow that the general public does not. After all, it’s why they’re a successful venture capital firm that consistently “backs bold entrepreneurs building the future through technology,” controversies and all.

The Sustainable Finance Disclosure Regulation (SFDR) is the EU’s framework for governing how sustainability considerations are disclosed in investment products. While designed to improve transparency and reduce greenwashing, SFDR gradually evolved into a de facto labelling system, with Articles 8 and 9 shaping how funds were marketed and perceived.

In late 2025, the European Commission put together an SFDR 2.0 proposal. It’s intended to acknowledge that this approach has created complexity, inconsistency, and confusion for investors. By shifting toward clearer product categories and simpler disclosures, the reform aims to restore credibility and usability.

A New Category-Based Framework

SFDR 2.0 introduces three product categories: Sustainable, Transition, and ESG Basics. While categorization is voluntary, funds choosing a category must meet mandatory criteria for that classification. Each category is tied to a minimum 70% portfolio alignment with the stated strategy, alongside mandatory exclusions for activities such as those involving controversial weapons, tobacco, hard coal, and severe breaches of international norms. Products outside these categories face tighter limits on ESG-related naming and marketing claims.

Sustainable products are reserved for funds investing primarily in sustainable activities or assets, including taxonomy-aligned strategies and Paris-aligned benchmarks. These products are subject to the strictest fossil fuel exclusions, including a ban on new coal, oil, and gas development.

Transition products are designed to capture strategies financing the shift toward sustainability. They rely on credible transition plans, science-based targets, and structured engagement, with tighter restrictions on fossil fuels than ESG Basics products and a clear focus on forward-looking change.

ESG Basics products integrate ESG approaches in the investment strategy but do not qualify as Sustainable or Transition. While still subject to baseline exclusions and the 70% alignment rule, this category has drawn early criticism for its relatively lenient treatment of fossil fuels.

Less Complexity, Tighter Guardrails

SFDR 2.0 removes entity-level PAI disclosures and simplifies product templates. Rather than relying on the current sustainable investment definition and DNSH mechanics in SFDR 1.0, the proposal operationalizes ‘no harm’ and safeguards through a common exclusion baseline plus product-level disclosure of principal adverse impacts, with DNSH and good governance reflected via category criteria. Disclosures are significantly shortened, with pre-contractual and periodic reports capped at two pages, and marketing rules tightened to limit sustainability claims to qualifying products.

The intent is clear. SFDR 2.0 shifts from dense, technical disclosures toward clearer categories supported by exclusions and simpler safeguards.

Timeline and Market Impact

The legislative process is expected to conclude in late 2026 or early 2027, followed by an 18-month implementation period. Until then, asset managers must continue complying with SFDR 1.0 while preparing for a full reclassification of their product ranges.

For the market, this likely means a smaller but more clearly defined universe of labelled funds. Many current Article 8 and 9 products are expected to reclassify, while Sustainable products under the new regime may be fewer but broader in scope. Asset managers face near-term transition costs and communication challenges, but also the prospect of greater long-term clarity and reduced compliance complexity.

A Reform Still Under Scrutiny

Initial reactions have been mixed. Industry groups broadly welcome the simplification and stronger fossil fuel exclusions for Sustainable and Transition products. At the same time, concerns persist regarding the scope of the ESG Basics category, the lack of a level playing field for unclassified funds, and the absence of more stringent engagement requirements for transition strategies. Organizations such as Eurosif and Morningstar have described the proposal as a step forward that still leaves room for improvement, particularly in preventing greenwashing at the lower end of the spectrum. Triodos Investment Management has also voiced similar caution.

What SFDR 2.0 Signals

SFDR 2.0 reflects a broader recalibration in EU sustainable finance policy. After years of expanding disclosure requirements, the focus is shifting toward usability, clarity, and enforceable standards. For asset managers, the message is straightforward: Sustainability claims will be more tightly defined, product positioning will matter more, and the margin for ambiguity is narrowing as SFDR enters its next phase.

As scrutiny of corporate supply chains intensifies, investors are demanding more than policy statements and third-party audits. In this webinar, SESAMm and Inrate explore two powerful lenses for evaluating risks and sustainability impacts across global supplier networks: SESAMm’s real-time controversy detection and Inrate’s impact-driven sustainability data and ratings. Together, these approaches cover both public and private companies, go beyond self-disclosures, and enable assessments across a wide range of suppliers.

Watch this instant replay to dive into:

Emerging trends shaping how investors assess ESG risks and impacts across supply chains

The expanding role of AI in identifying hidden exposures and mapping sustainability outcomes

Proven strategies for combining controversy signals, ESG ratings, and emissions data to drive more informed decisions

Stay ahead with the latest in ESG and AI intelligence

Join our mailing list to receive new reports, event invites, and updates from SESAMm directly to your inbox.

.png)