The private markets secondaries space has entered a new chapter. What was once a niche corner of alternative investments, used primarily by limited partners (LPs) seeking early exits from fund commitments, has grown into one of the most dynamic segments of global private capital. The market has tripled in size since 2019 and grown by approximately 50% between 2024 and 2025 alone, reaching an estimated $230 billion in annual transaction volume and now representing around 5% of all global private equity assets under management.

This piece examines the forces behind that expansion, the structural shifts redefining the market, and the operational and regulatory challenges participants will need to navigate as the asset class continues to scale.

Market Growth and Shifting Deal Dynamics

Several converging factors have driven the secondaries market to its current size. A prolonged slowdown in IPO activity and traditional exits has created a liquidity bottleneck across private markets, leaving many LPs over-allocated to alternatives and constrained in their ability to make new commitments. The secondary market has become a primary mechanism for these investors to rebalance portfolios and free up capital.

Deal structuring has grown more sophisticated in step with market volumes. Ropes & Gray has observed a continued expansion in the use of purchase price deferrals and earnouts, and more recently, the introduction of deal-specific funding caps, limits on how much capital a buyer can be called to deploy before a specified date. These mechanisms allow sellers to achieve higher reference-date pricing while enabling buyers to manage capital deployment pacing and portfolio composition. In Q1 2026 alone, institutions initiated new secondary sales processes totaling north of $20 billion, some linked to denominator effect concerns as declines in public market portfolios pushed private allocations above target levels. Whether this proves a sustained driver of supply will depend on how institutional portfolios weather current market conditions.

The Three Transaction Types

Secondary transactions fall into three main categories:

- LP-led transactions, the original form, involve an LP selling existing fund interests, sometimes across a broad portfolio of hundreds of positions, typically through competitive auction processes with tight timelines.

- GP-led continuation funds, the fastest-growing segment, involve a sponsor transferring select assets into a new vehicle, giving existing LPs the option to cash out or roll forward. As of 2025, GP-led and LP-led volumes are roughly evenly split at around $115 billion each. GP-led buyout fund volume grew 39% year-over-year, while private credit secondaries saw nearly 300% year-over-year growth in GP-led activity.

- The third category, structured solutions, provides capital to a GP collateralized by existing fund assets and can take a wide variety of bespoke forms.

What Are the Operational and ESG Challenges in the Market?

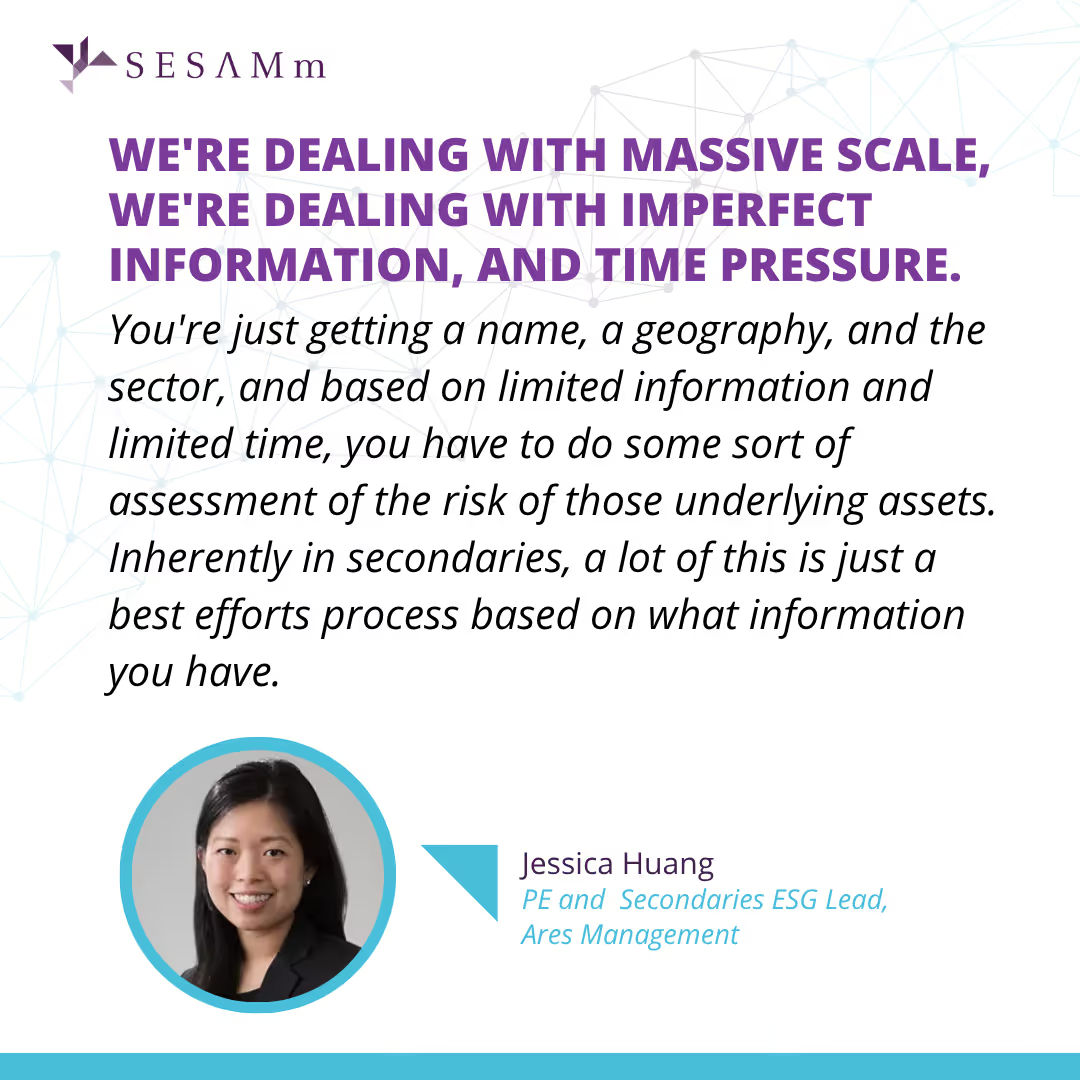

One of the defining challenges in secondaries is the speed and scale of due diligence required, particularly in LP-led transactions. Buyers may need to evaluate hundreds, or in private credit secondaries, over a thousand, underlying positions with limited information and within windows of 24 to 48 hours. As Jessica Huang, Managing Director and ESG lead for private equity and secondaries at Ares Management, noted in a recent webinar:

Against this backdrop, LP expectations around ESG integration have risen sharply. LPs are now holding secondaries to a standard closer to that applied to direct investments, with requests for Article 8-classified funds, look-through exclusion lists, and UN Global Compact compliance screening becoming more common. Main exclusion categories include fossil fuels, controversial weapons, tobacco, and gambling, though definitions and revenue thresholds vary significantly across mandates. SFDR 2.0, currently in draft form, may introduce additional mandatory exclusion categories that managers are monitoring closely. In LP-led deals where buyers are inheriting a broad portfolio of assets, highly granular opt-outs can mean missing certain large transactions, a trade-off that must be clearly communicated to LPs.

The Role of Technology and AI

Technology has become central to the scaling of secondaries operations. AI tools are now applied across controversy screening, ESG data analysis, and emissions estimation, where direct disclosures are unavailable. A particular challenge in the asset class is coverage: many underlying companies are small or mid-market private businesses not captured in conventional databases.

Market participants consistently emphasize that AI outputs serve as inputs to human judgment, not as replacements for it. At Ares, screening results are reviewed by ESG specialists before being passed to deal teams for final decisions.

What the Future Holds

Transaction volumes are forecast to continue rising as both the seller and buyer universes expand. Private credit, infrastructure, and structured secondaries all represent areas of growing specialization and regional expansion, particularly in Asia, where secondary activity has been limited but is expected to grow as investment programs mature, broadening the market further. Capital supply dynamics bear watching: while dry powder remains substantial, deal volume growth has outpaced fundraising since 2023, which could create pricing or capital constraints. The entry of retail investors through evergreen vehicles adds a meaningful new source of capital but brings different liquidity expectations and regulatory considerations.

On the operational side, the sophistication of deal terms, the complexity of ESG compliance, and the volume of data processed per transaction are all increasing. Firms that can integrate technology into their diligence and monitoring workflows, while preserving the human judgment layer, will be best positioned to manage market growth. Secondaries are no longer a supplementary liquidity tool; they have become a structural feature of how private markets operate.

.avif)

.avif)

.png)