SEC Withdraws Defense of Climate Disclosure Rules: Impact on ESG Investing

May 9, 2025

•

5 mins read

The Securities and Exchange Commission (SEC) has voted to cease defending its climate disclosure regulations in court, marking a significant shift in U.S. corporate sustainability reporting requirements. This decision, announced on March 27, 2025, under Acting Chairman Mark Uyeda's leadership, has substantial implications for the ESG landscape.

The Decision

The SEC’s withdrawal from defending its climate disclosure rules comes amidst ongoing litigation before the U.S. Court of Appeals for the Eighth Circuit. Originally adopted in 2024, the rules were intended to provide investors with standardized information about companies' climate-related risks, emissions, and the financial impact of those risks. Uyeda justified the withdrawal by stating, “The goal of today’s Commission action is to cease the Commission’s involvement in the defense of the costly and unnecessarily intrusive climate change disclosure rules.” The regulations faced swift opposition from industry trade groups and Republican state attorneys general, who argued the SEC had overstepped its authority. The legal challenge quickly gained momentum, and with the change in SEC leadership, the agency opted not to continue defending the rules. Caroline Crenshaw, the lone Democratic commissioner, sharply criticized the move. She described it as an attempt to “unlawfully undo valid regulations” and accused her colleagues of “watching the rule’s demise while eating popcorn on the sidelines.”

Market Implications

The decision reintroduces regulatory uncertainty for companies. Many had already begun preparing internal systems and compliance structures based on the 2024 rules. Now, in the absence of a federal standard, they may be forced to rely on voluntary reporting frameworks or navigate a fragmented set of expectations from investors, states, and international markets. This lack of uniformity is likely to lead to inconsistent reporting practices and difficulties in cross-company comparisons. Investors, meanwhile, will face greater challenges in accessing reliable and comparable data on climate-related risks. Without SEC-mandated disclosures, much of the burden of transparency shifts to individual companies and third-party ESG data providers. Investors will likely need to increase due diligence efforts, adopt varied methodologies, and potentially absorb higher costs to obtain the data needed to manage climate risk effectively.

The Broader Context

This decision does not exist in isolation—it aligns with a broader trend of regulatory rollback on climate issues in the U.S. and signals a widening divergence between American and international disclosure approaches.

The divergence creates complexity for multinational corporations that must now navigate different expectations in different jurisdictions. This fragmentation may also create competitive disadvantages for U.S.-listed firms, especially those competing for capital in more disclosure-forward markets.

SEC Leaves the ISSB

In a related move that further isolates the U.S. from international sustainability efforts, the SEC recently withdrew from two key ISSB governance groups: the IFRS Sustainability Jurisdictional Working Group and the Sustainability Standards Advisory Forum. These groups are central to building alignment on global ESG disclosure standards.

The SEC’s exit from these forums signals a significant retreat from coordinated climate disclosure initiatives and weakens the U.S. role in shaping global ESG norms.

Market Response

Despite the rollback, some companies may continue voluntary climate-related disclosures. Those that have already invested in reporting infrastructure may opt to maintain transparency to meet investor expectations, mitigate reputational risk, and support long-term sustainability goals.

Simultaneously, ESG data providers and rating agencies are expected to play a more prominent role in filling the information gap. Financial institutions may also develop their own internal frameworks to evaluate climate risks, further privatizing what was once a public regulatory function.

Looking Forward

The path ahead remains uncertain. State-level legislation may introduce a patchwork of new rules. Global investors—particularly those with mandates in the EU or UK—may continue demanding robust disclosures from U.S. firms. And future federal administrations could choose to reintroduce or reshape mandatory disclosure regimes. In the interim, companies and investors will need to adapt by maintaining flexible reporting systems, monitoring evolving voluntary frameworks, and diversifying their sources of ESG data. While federal requirements may have receded, the underlying investor interest in climate-related financial risk is not going away. Climate disclosure, in one form or another, remains firmly on the radar.

SESAMm’s AI Technology Reveals ESG Insights

Discover unparalleled insights into ESG controversies, risks, and opportunities across industries. Learn more about how SESAMm can help you analyze millions of private and public companies using AI-powered text analysis tools.

Greenwashing in ESG has become harder to detect, not easier, because the corporate playbook has matured. Claims are vaguer, disclosure is more selective. Meanwhile, two adjacent problems have grown up next to it: greenwishing and greenhushing. The biggest greenwashing risk in your portfolio probably isn't the company you suspect, it's the one you don't. This guide is about all three, and how AI surfaces them at the speed your investment process needs.

Over the past decade, many organizations have improved their carbon footprints, from recyclable and biodegradable packaging and single-use plastic to planting trees and reducing their greenhouse gas emissions. However, some businesses and companies looking to boost their eco-friendly image without committing to serious changes and addressing environmental issues have been associated with false green marketing. We call this "Greenwashing."

Defining Concepts

What is Greenwashing?

Greenwashing is a practice used by businesses to represent themselves as more sustainable than they truly are. Greenpeace and the Environmental Protection Agency define greenwashing as making false and misleading claims about a product's environmental benefits or practices, services, technology, or company practices. Greenwashing typically involves companies spending more money on advertising and marketing than on implementing sustainable business practices that minimize environmental impact. These false green claims can deceive consumers into believing that a product or company is more environmentally friendly than it is, leading to increased sales and profits. As a result, false advertising, misleading initiatives, and groundless claims have increased green investors' exposure to risks emerging from potential lawsuits from activist groups, image deterioration, and heavy losses in assets invested.

Greenwashing Mentions Over Time

In recent years, new concepts have emerged alongside greenwashing:

Greenwashing, Greenhushing, and Greenwishing Mentions Over Time

Greenhushing refers to a company’s refusal to publicize ESG information. The company may fear pushback from stakeholders who would find its sustainability efforts lacking or from investors who believe ESG undermines returns.

Greenwishing, or unintentional greenwashing, describes a practice where a company hopes to meet certain sustainability commitments but simply does not have the means to do so.

High-Profile Greenwashing Case Studies

When talking about greenwashing, the usual suspects are the oil and gas industry, the food and beverage sector, and other environmentally impactful industries. However, the financial industry has also been embroiled in its own greenwashing controversies.

It’s challenging to produce an accurate assessment of environmental, social, and governance (ESG) factors, which creates opportunities for companies to hide ineffective and fake green initiatives. According to Regtank, the main challenges to detecting greenwashing include:

Lack of reporting standards – There’s no universal set of standards for ESG compliance.

Lack of transparency – Companies often don’t disclose the specifics of their “green campaigns,” making it hard for investors and consumers to verify their claims.

Limited consumer awareness – Misleading marketing can exploit consumers’ eco-consciousness and brand loyalty, reducing scrutiny of false green claims.

These gaps lead to inaccurate ESG data and scores, allowing greenwashers to avoid accountability. Ultimately, detecting greenwashing requires careful scrutiny of company claims and a deep understanding of their supply chains and operations.

How Artificial Intelligence Detects Greenwashing

As greenwashing practices become more common, activist investors, journalists, and the general public are using social media, news outlets, and blogs to highlight false claims. Artificial intelligence (AI) has become an invaluable tool in the early detection of greenwashing by analyzing vast amounts of public data.

At SESAMm, we use generative AI and LLMs to identify greenwashing risks across billions of web-based articles. Our data lake covers over 25 billion articles in more than 100 languages from four million news sources, blogs, social media platforms, and forums, analyzing data on five million public and private companies. Through our AI platform, we generate reliable, timely, and comprehensive insights to detect greenwashing, monitor ESG controversies, and identify related risks.

The CSRD significantly strengthens the requirements for companies to substantiate their sustainability commitments. Mandating standardized and detailed ESG disclosures directly addresses the practice of greenwashing, where companies exaggerate their environmental credentials in marketing without meaningful follow-through. Under the CSRD, companies can no longer rely on vague or selectively presented data—any gaps or inconsistencies in their sustainability claims will be exposed in public filings, making greenwashing much riskier. This means an end to cherry-picked data and a shift toward more comprehensive, comparable, and verifiable ESG performance for investors and stakeholders.

The CSDDD (if it stands) further reinforces these efforts by obligating companies to go beyond marketing statements and prove they’re actively managing environmental and human rights impacts throughout their supply chains. This directive closes loopholes that greenwashing often exploits, such as highlighting only direct operations while ignoring supplier practices. By requiring due diligence on environmental impacts across the value chain, the CSDDD aims to turn sustainability from a branding exercise into a legal and operational priority. If real supply chain actions don’t support a company’s green claims, it could face legal action and reputational damage.

Looking Ahead

Looking ahead, greenwashing will continue to face intense scrutiny from regulators, investors, and the public. With evolving regulatory frameworks like CSRD and CSDDD, the pressure is on for companies to ensure genuine environmental responsibility—not just green advertising. At SESAMm, we believe that the combination of regulatory rigor and advanced AI technologies will play a critical role in uncovering false green claims and supporting investors in navigating ESG risks with greater transparency and accountability.

SESAMm’s AI Technology Reveals ESG Insights

Discover unparalleled insights into ESG controversies, risks, and opportunities across industries. Learn more about how SESAMm can help you analyze millions of private and public companies using AI-powered text analysis tools.

ESG frameworks are multiplying faster than organizations can comply with them. Supply chain visibility remains the weakest link, supplier self-disclosures are incomplete, ESG data is inconsistent, and regulatory requirements conflict across jurisdictions. Yet controversy events move fast. A reputational crisis, a forced labor allegation, or an environmental violation at a tier-two supplier can cascade through your entire supply chain in hours. Organizations that win today are those using AI to detect hidden ESG risk before the news breaks, turning fragmented data into actionable intelligence that protects brand, license to operate, and investor confidence.

Key Takeaways

Timely Response to ESG Controversy EventsCritical for maintaining corporate responsibility programs amid regulatory fluctuations.

AI-Powered Risk DetectionProactively detect and mitigate hidden ESG risk across supply chains.

Real-World Case StudiesUncover ESG risk that supplier questionnaires and internal data cannot expose.

Globally, ethics and sustainability are important, but the retail industry faces intense scrutiny over supply chain integrity. This spotlight shines on SHEIN and TEMU, two giants in the fast fashion and e-commerce sectors, known for their vast reach yet marred by controversies around labor practices and environmental impacts. This article explores their supply chain strategies, examining how current and emerging legislation, like the CSDDD initiative, aims to tackle the ethical dilemmas plaguing global retail. Through a comparison of SHEIN and TEMU, we assess the effectiveness of regulatory frameworks in addressing these critical issues. By analyzing their ESG controversies and comparing their responses, we assess how well current and future legislation, particularly the CSDDD initiative, addresses ethical issues in global supply chains.

Specialized Retail: The Case of SHEIN and TEMU

SHEIN and TEMU are compelling use cases due to their past controversies and the focus on their supply chain practices. Both companies have come under scrutiny for their labor practices, environmental impacts, and ethical issues, making them ideal subjects for analysis. By studying their supply chain challenges, we aim to assess the effectiveness of current legislation and predict the potential impact of future regulatory frameworks, particularly in the context of the CSDDD initiative.

While both companies operate with a similar business model, SHEIN is an established player entangled in numerous supply chain controversies. On the other hand, TEMU, a newcomer since 2022, faces similar issues. Comparing them helps us evaluate the effectiveness of existing supply chain legislation and determine whether increased regulatory scrutiny has improved compliance or merely raised awareness of these controversies within the industry.

Note:

Size bias mitigation:

We normalized the data for both companies to ensure an equal basis of comparison, accommodating the difference in operational history—SHEIN since 2008 and TEMU since 2022— to eliminate discrepancies in web attention.

Risk analysis:

It’s worth noting that the figures presented here specifically relate to supply chain risks, as that is the primary focus of our analysis.

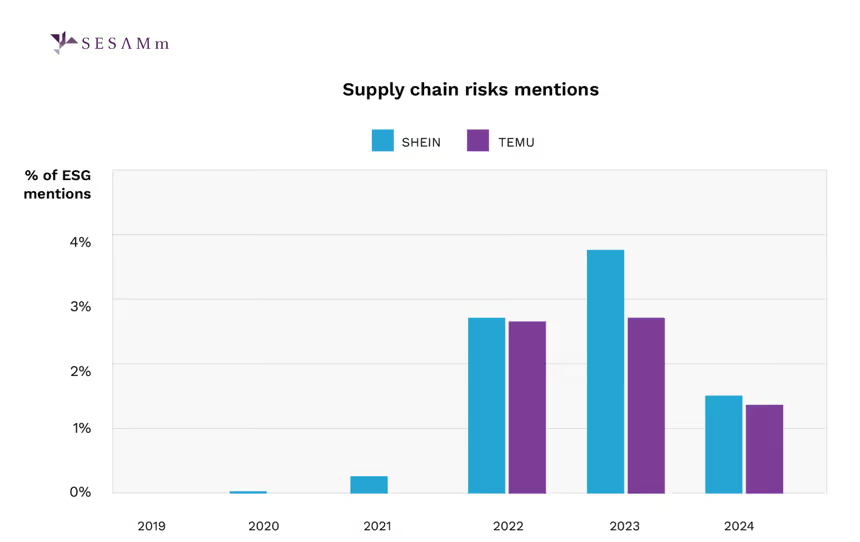

Examining Supply Chain Controversies

We analyzed ESG risks in the supply chains of SHEIN and TEMU over the past four years, adjusting data volumes for comparative analysis. SHEIN's supply chain risks have significantly increased since 2021, peaking in 2022 and continuing to rise in 2023, reflecting a growing online focus on its issues. Meanwhile, TEMU, despite only being established in 2022, has quickly come under intense scrutiny. The company faces frequent criticism for its supply chain practices, including condemnations for inaction and ongoing human rights violations.

Examining Social Sub-risks

In our analysis of social risks within the supply chains of TEMU and SHEIN, we discovered that fundamental human rights and labor rights are the most and second most prevalent issues, respectively. Notably, despite TEMU's more recent establishment compared to SHEIN, its supply chain has a relatively higher proportion of human rights controversies.

Both companies have faced serious allegations related to their supply chain practices. TEMU and SHEIN are scrutinized for using Chinese cotton potentially linked to slave labor, with insufficient efforts to mitigate forced labor risks. Allegations include child slavery, privacy issues related to sharing user data, and environmental neglect, including the use of carcinogens in products. Despite their efforts to boost their public image through aggressive marketing and influencer engagements, both companies have been criticized for their approach to environmental responsibility and labor practices.

Political calls for investigations into the use of Uyghur slave labor in both companies underscore their ethical challenges. Neither company has shown rigorous compliance with anti-forced labor laws, lacking stringent programs to audit supplier compliance. This highlights significant gaps in their corporate responsibility efforts.

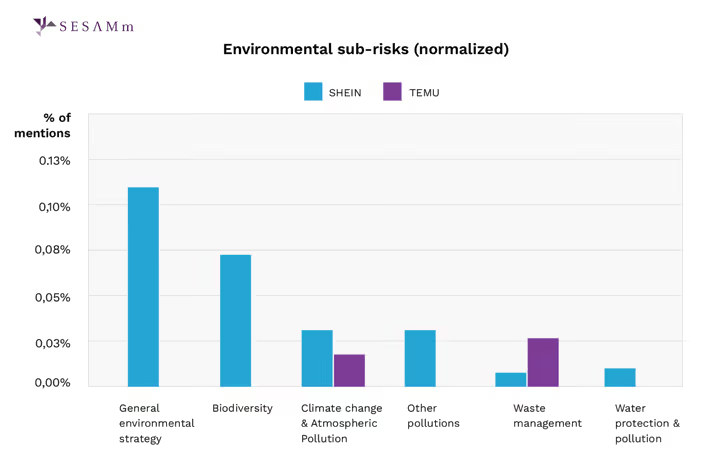

It's evident that social risks, particularly human rights breaches and labor rights controversies, have received significantly more attention than environmental risks. Despite the severity of environmental events, they represent a lower percentage in comparison. This highlights the prioritization of addressing social issues within these companies' operations.

SHEIN experiences extensive scrutiny, leading to a wealth of data on its practices. Conversely, TEMU, despite facing environmental controversies, has been less transparent about its environmental footprint, with Greenpeace reports highlighting this lack of clarity. This disparity underscores that SHEIN’s environmental impacts are more thoroughly documented than TEMU’s.

These environmental and health issues gained attention during SHEIN’s attempts to launch IPOs in the US and UK, spotlighting the company's ethical and environmental practices. Despite SHEIN's pledges to donate towards solving textile waste problems, critics label these actions as greenwashing, calling for significant alterations to its business model to address the underlying issues effectively.

Supply Chain Dynamics: SHEIN vs TEMU

While TEMU doesn't have its own brand like SHEIN, it operates under a comparable business model. It acts as an intermediary, managing shipments for products it doesn't manufacture. Despite their distinct approaches, both companies frequently engage in disputes, drawing attention to their supply chains. Additionally, policymakers often group them with similar firms, subjecting their fast fashion practices to heightened scrutiny.

These events highlight the growing scrutiny surrounding the supply chain practices of both SHEIN and TEMU. Senator Rubio's call for an investigation into allegations of Uyghur slave labor usage by both companies, additionally, mentions of Congressional attention has also focused on these companies, with reports exposing violations of U.S. tariff laws and evasion of human rights reviews on imports, shedding light on systemic issues within their operations.

Increasing Sustainability Awareness

We studied the mentions of both ESG initiatives associated with the brands and detected that over the analyzed time frame, SHEIN has been associated with significantly more initiatives than TEMU.

We analyzed the sustainability initiatives of these companies, finding that SHEIN's efforts outpace TEMU's significantly.

SHEIN focused on circular economy practices, exemplified by partnerships like that with Queen of Raw to reuse excess industry inventory and launches such as EvoluSHEIN and SHEIN Exchange, also boosting Product safety mentions, which promote recycled materials and resale of used products, respectively.

Throughout our analysis period, we noted that 2022 was a turning point for SHEIN's sustainability efforts, sparked by several mentions of breaches related to the Modern Slavery Act and child labor allegations in the previous year, which subsequently increased the company’s sustainability-related mentions. By 2023, as SHEIN prepared for potential IPOs in the US and UK and with the release of a controversial documentary, the company faced heightened scrutiny, with more allegations surfacing in its supply chain concerning various acts and legislations, such as the Modern Slavery Act, Uyghur Forced Labor Prevention Act, and others. Despite these challenges, mentions of SHEIN’s ESG initiatives also rose, although they remained less prominent than risk-related mentions due to controversies typically gaining more attention online. However, from 2024 to the present, we have observed more initiatives than risks, suggesting that, despite some acts and legislations being non-binding or not directly applicable to SHEIN, the potential reputational impacts drive the company toward positive change.

It's worth noting that we've observed discussions linking SHEIN with the recent EU Corporate Sustainability Due Diligence Directive, also referred to as CSDDD or CS3D. These discussions underscore the view that governments should refrain from incentivizing fast fashion companies like SHEIN. As the CSDDD is expected to bring about significant changes, forcing businesses to identify, prevent, or mitigate adverse impacts of their operations on human rights and the environment. Notably broader in scope compared to previous legislation, this directive will apply to all EU companies surpassing a certain revenue threshold. Consequently, fast-fashion retailers like SHEIN will face increased requirements to take action and ensure compliance.

The absence of enforceable regulations allows companies like TEMU to continue operating, but SHEIN's actions, particularly as it moves towards an IPO, raise questions about whether its efforts to improve practices are driven by the scrutiny associated with preparing for a public offering or by a sincere commitment to compliance with laws and regulations.

To conclude, our analysis underscores the dynamic landscape of supply chain regulations, ESG risks, and sustainability initiatives within the specialized retail sector, particularly in the fast-fashion industry. A focus on SHEIN and TEMU reveals a rise in both ESG initiatives and identified breaches. SHEIN's proactive initiatives suggest a response to regulatory pressures. Additionally, our findings suggest that even without binding legal requirements, companies may still choose to comply to enhance their reputation or respond to heightened scrutiny.

Reach out to SESAMm

TextReveal’s web data analysis of over five million public and private companies is essential for keeping tabs on ESG investment risks. To learn more about how you can analyze web data or to request a demo, reach out to one of our representatives.

Stay ahead with the latest in ESG and AI intelligence

Join our mailing list to receive new reports, event invites, and updates from SESAMm directly to your inbox.

.avif)

.avif)

.avif)

.avif)

.png)