A single number is a powerful thing. It can summarise months of reporting across dozens of sources into something a risk team can act on in seconds. It can also hide more than it reveals, if no one explains how it was built. When the same company receives very different ESG scores from different providers, the usual reason is not bad data. It is undisclosed method.

SESAMm has published the full methodology behind its Controversy Exposure Score, free to access, following the entry into force of the EU ESG Rating Regulation on 2 July 2026. This article walks through what the score measures, how it is constructed, and the two design choices that most distinguish it.

What the Score Measures

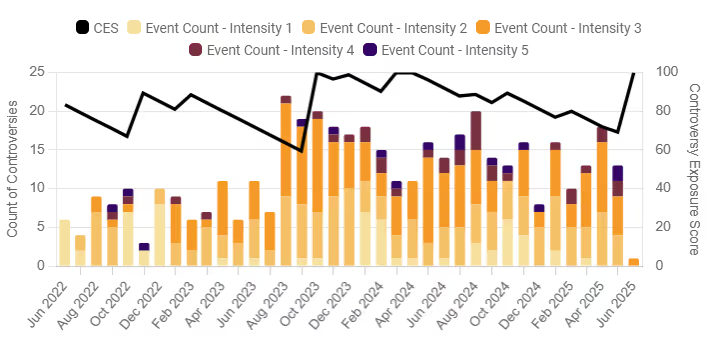

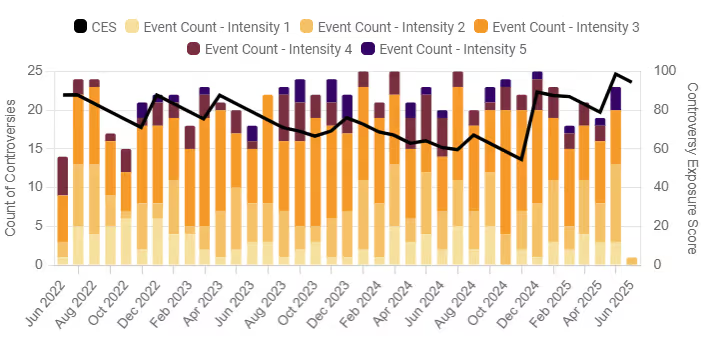

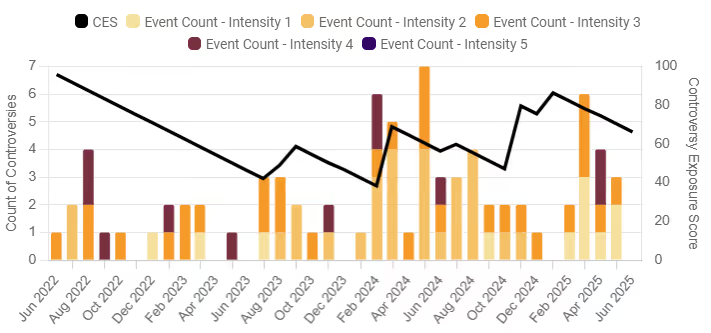

The Controversy Exposure Score, or CES, runs on an absolute scale from 0 to 100 and is grouped into five risk bands, from Very Low to Very High. It has a single, deliberately narrow objective: to measure an entity's exposure to ESG controversies, meaning adverse events and conduct attributed to that entity as reported in public sources.

Three points define its scope from the outset. The CES is an impact-materiality measure. It looks at the negative footprint of an entity's activities on people and the environment, not the financial effect of ESG issues on the company itself. It is backward-looking. It reflects controversies that have already been reported, over a rolling 24-month window, rather than forecasts or transition pathways. And it is built only from public and licensed public-domain information, never from private, confidential or self-reported data.

From Millions of Articles to a Single Case

Before any score can exist, raw coverage has to become structured information. This is where most of the engineering sits.

SESAMm's pipeline first attributes each document to the right entity and screens it for genuine ESG relevance against a multilingual taxonomy, removing low-quality, duplicate or non-editorial content. It then addresses a problem familiar to anyone who monitors the news: media echo. A single real-world incident can generate dozens of near-identical articles. To prevent that from inflating the picture, related documents are grouped into Events, and related Events into Cases, so that a controversy unfolding over time is tracked as one continuous case rather than many separate items.

A validation step then confirms that each candidate event is a genuine ESG controversy concerning the entity, acting as a control against false positives before anything enters the score. Only after this sequence does scoring begin.

Design Choice One: Severity Before Volume

The most important question about any controversy is not how many articles it generated. It is how serious it is. SESAMm assesses severity first, through a feature called Event Intensity, scored on a 1 to 5 scale.

Severity is judged on two axes. The first is reversibility, the permanence of the harm, from a procedural or technical breach at the low end to irreversible damage such as fatalities or permanent ecosystem destruction at the high end. The second is reach, the scale of the impact, from an effect confined to a single facility up to systemic or national-level harm.

Two principles govern how these combine, drawn from the UN Guiding Principles approach to identifying severe impacts. Permanence takes priority over breadth, so an irreversible harm weighs more than a widespread but remediable one. And grave, irreversible events are designed not to slip into low-severity tiers simply because their reach was limited, so that isolated but serious events stay visible. The structured severity is then adjusted for the entity's actual responsibility, from direct involvement through its own operations to indirect involvement through its value chain.

Media coverage does play a role, but a disciplined one. The level of coverage contributes to the score as a signal of salience, and it is rebased against each entity's own historical media baseline rather than counted in absolute terms. This stops high-profile companies from looking riskier simply because they attract more press, and it keeps the engine sensitive to genuine spikes at less-covered entities.

Design Choice Two: Worst-Of, Not Average

The second defining choice is how the pillars combine. Most ESG scores apply percentage weights to Environmental, Social and Governance factors and blend them into a weighted average. SESAMm deliberately does not.

The reason is a structural flaw the company calls dilution bias, or data masking. When pillars are averaged, strong administrative compliance in one area can mathematically conceal a catastrophic breach in another. A company with excellent governance disclosures could see a severe environmental controversy diluted into a comfortable middle score.

Instead, the CES uses a rule-based maximum-severity, or worst-of, logic. The entity's most serious controversy drives the score, regardless of which pillar it sits in, and it cannot be watered down by stable metrics or an absence of alerts elsewhere. The five bands that result are fixed in absolute terms rather than calculated relative to a peer group, so a company's score is not flattered or punished by the behaviour of its sector. A score above 80 reflects critical, often irreversible breaches. A score of 20 or below reflects negligible or minor isolated issues.

A Number You Can Interrogate

Taken together, these choices produce a score with a clear logic behind every point on the scale. Severity is assessed before volume. The gravest event leads. Coverage is normalised so it informs rather than distorts. And the bands mean the same thing for every entity, in every sector, anywhere in the world.

None of this requires a user to take the result on faith. The objective, the taxonomy of 44 sub-risks, the severity model, the aggregation rule and the interpretation of each band are all set out in the public methodology. A score is only as useful as the method that produced it, and that method is now open to read.

To see exactly how the Controversy Exposure Score is constructed, visit sesamm.com/methodology.

.png)