Teams that monitor ESG controversies usually have the opposite of an information shortage. A single incident can generate dozens of articles within a few days, each covering the same underlying event, often repeating the same facts with a few new details. At a certain point, the sheer number of articles makes it hard to tell which developments are material and which are just the same story told again.

The volume is the part that breaks traditional approaches. Millions of articles are written every day across hundreds of languages, more than any team of analysts could read, let alone reconcile into a clear timeline of an evolving controversy. This is not a problem you solve by adding more people; the scale is on a different order of magnitude from human reading speed.

What changed is that language models can now read, categorize, and evaluate. They cover that volume in every language, judging whether two articles describe the same incident, whether one marks a new development, and how incidents link into a single controversy over time. Leveraging the latest AI models is the only way to structure this much material and generate daily updates.

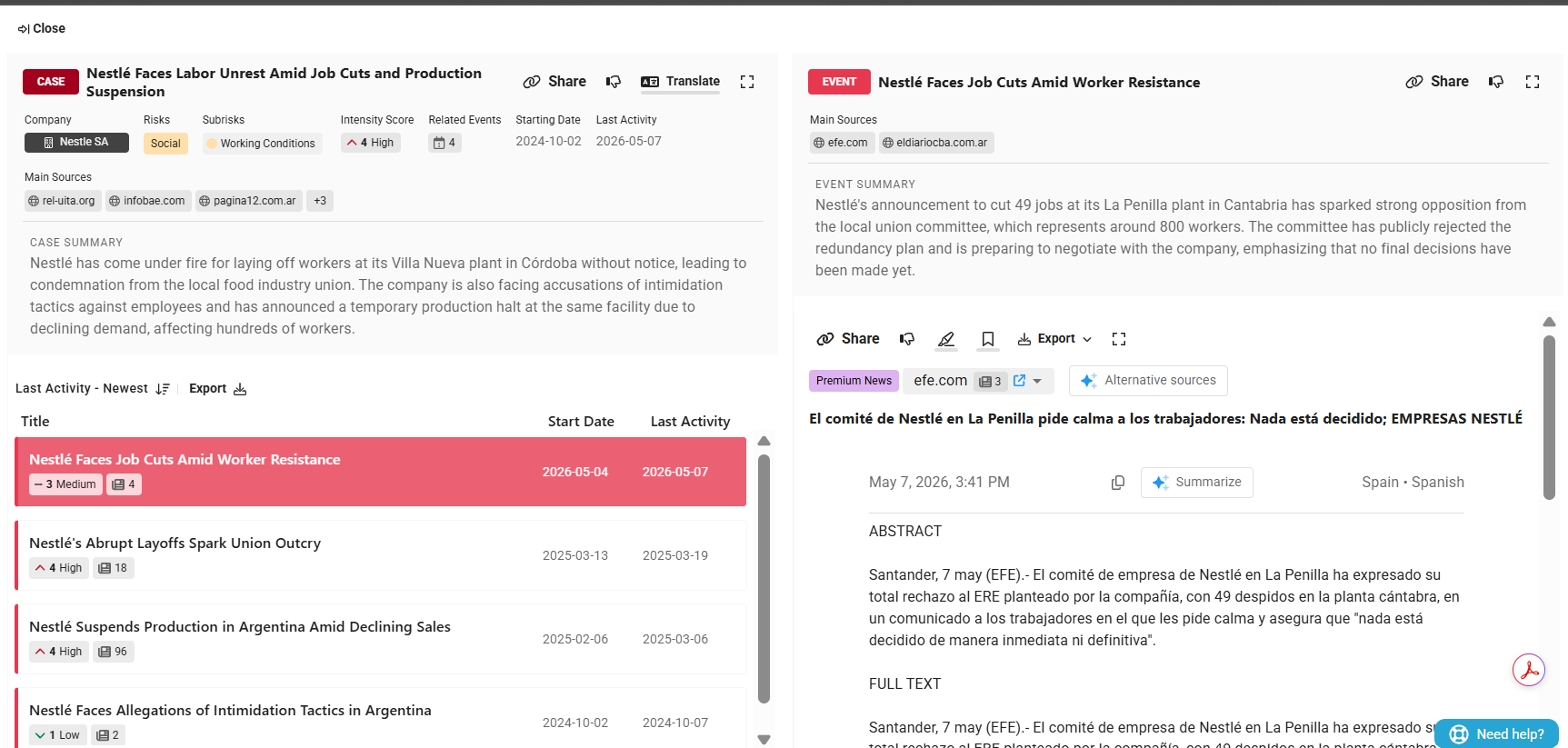

SESAMm runs this across the ten million documents it ingests each day, from more than four million sources in over 100 languages, including premium news wires, NGO bulletins, company communications, and discussion forums. The result is ESG controversies organized into three layers: articles, events, and cases.

From Articles to Events to Cases

Each layer builds on the one below it, and each answers a different question an analyst needs answered.

Articles are individual news articles or documents: the raw material.

Events group the articles that describe the same specific incident or development. When forty outlets cover the same supplier labor issue, those forty articles become a single event, with the underlying coverage attached. Articles published close together in time and describing the same development are grouped; an article describing a genuinely new development, even on the same broader topic, forms a separate event. A strike in 2022 and a similar strike in 2024 at the same supplier are recorded as two events, because they are distinct incidents rather than a continuation of one.

Cases sit above events. A case ties together the events that belong to the same underlying controversy as it unfolds, with no fixed time limit. An oil spill, the regulatory investigation that follows it, and the settlement that closes it months or years later are three separate events but one case.

Articles tell you what was written, events tell you what happened, and cases tell you how a controversy is developing. All three sit in the same view: one entry per controversy, with the chronology of events nested inside it and the source articles a click below that.

Why the Underlying Data Matters

A three-layer structure is only as good as the data underneath it. To capture a controversy from start to finish, that data has to include the early signals that appear in regional press, NGO bulletins, or non-English sources before larger outlets report them, sometimes days later.

SESAMm's coverage spans more than 100 languages and extends well beyond mainstream news wires, so its cases are built on a wider base than most monitoring platforms screen. A controversy that starts in a local-language outlet, moves through regional media, and reaches the international press is captured as a single continuous case, rather than surfacing as disconnected alerts or being missed altogether in its early stages.

What Does This Change in Practice?

Three things change in day-to-day work.

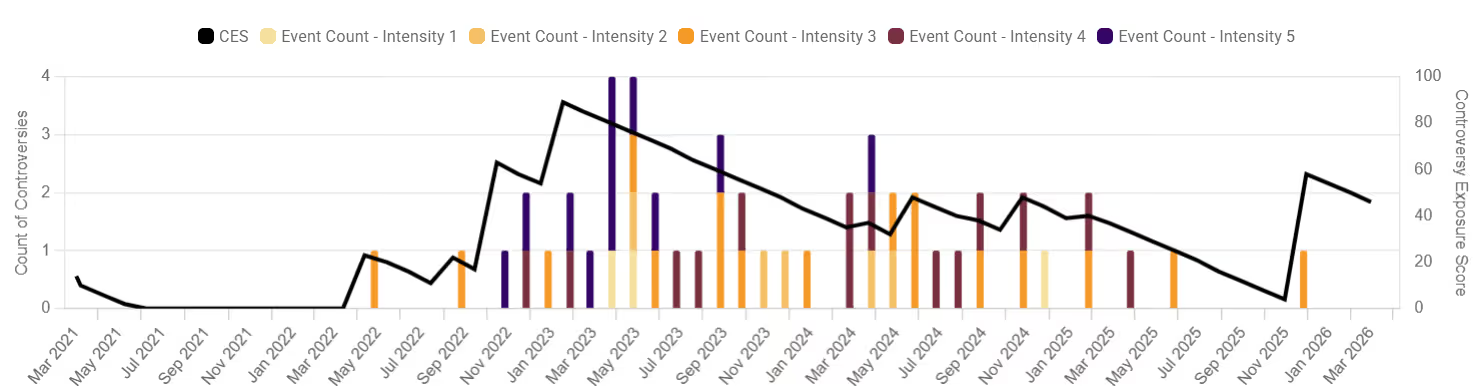

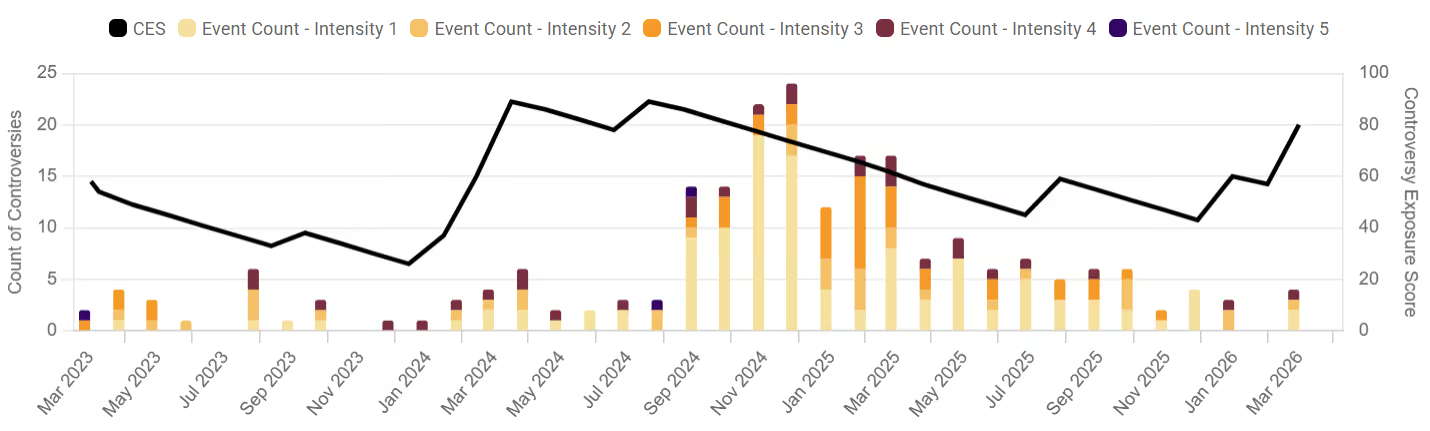

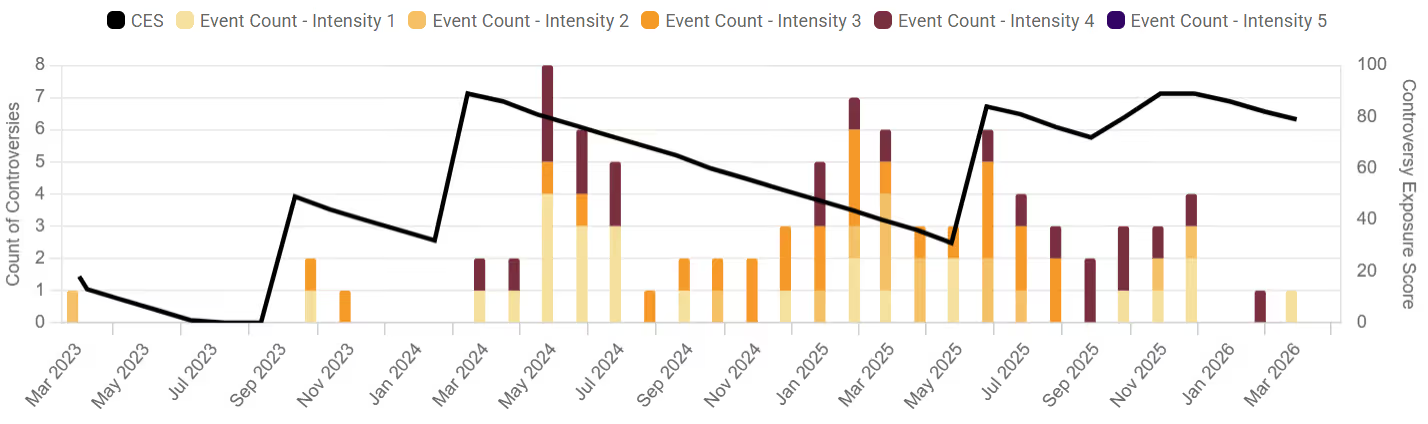

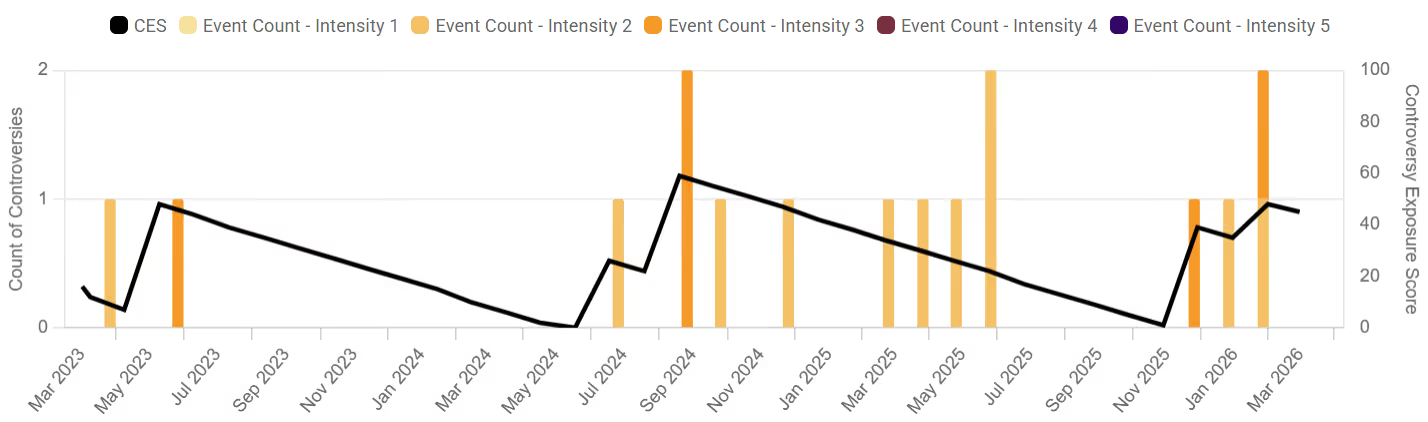

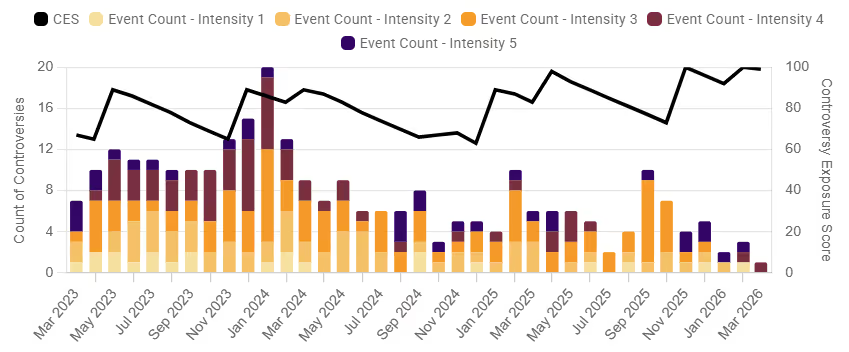

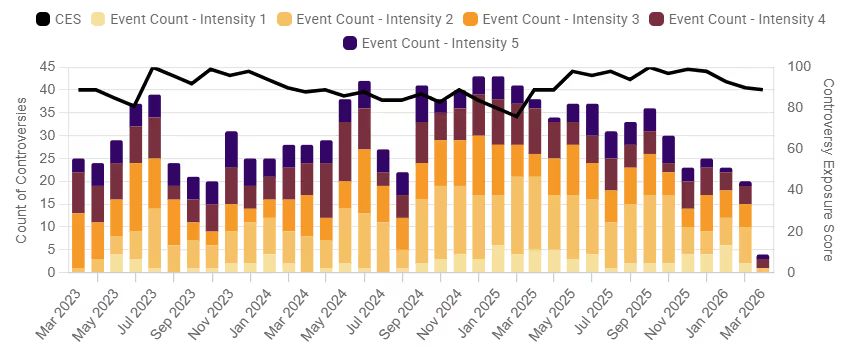

The count starts to mean something. A rise in the number of cases reflects new controversies emerging, not an old one being picked up by more outlets.

Trajectories become visible. As a case accumulates new events over the months, the progression from complaint to investigation to hearing to settlement is easy to follow, rather than being buried in hundreds or even thousands of articles.

Analysts spend their time differently. Less of it goes to clearing duplicate headlines, and more to the important judgment calls.

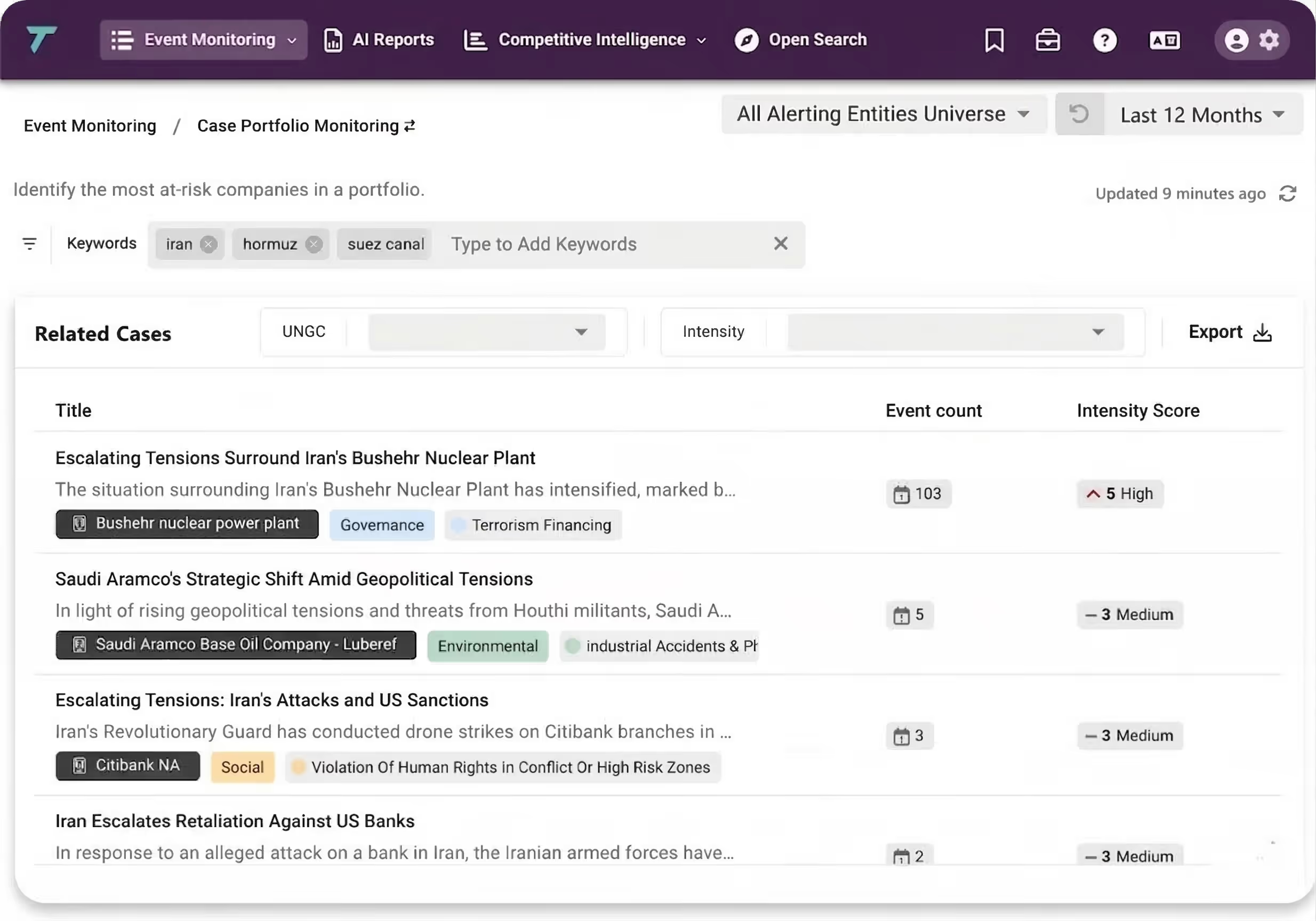

What This Looks Like in the SESAMm Dashboard

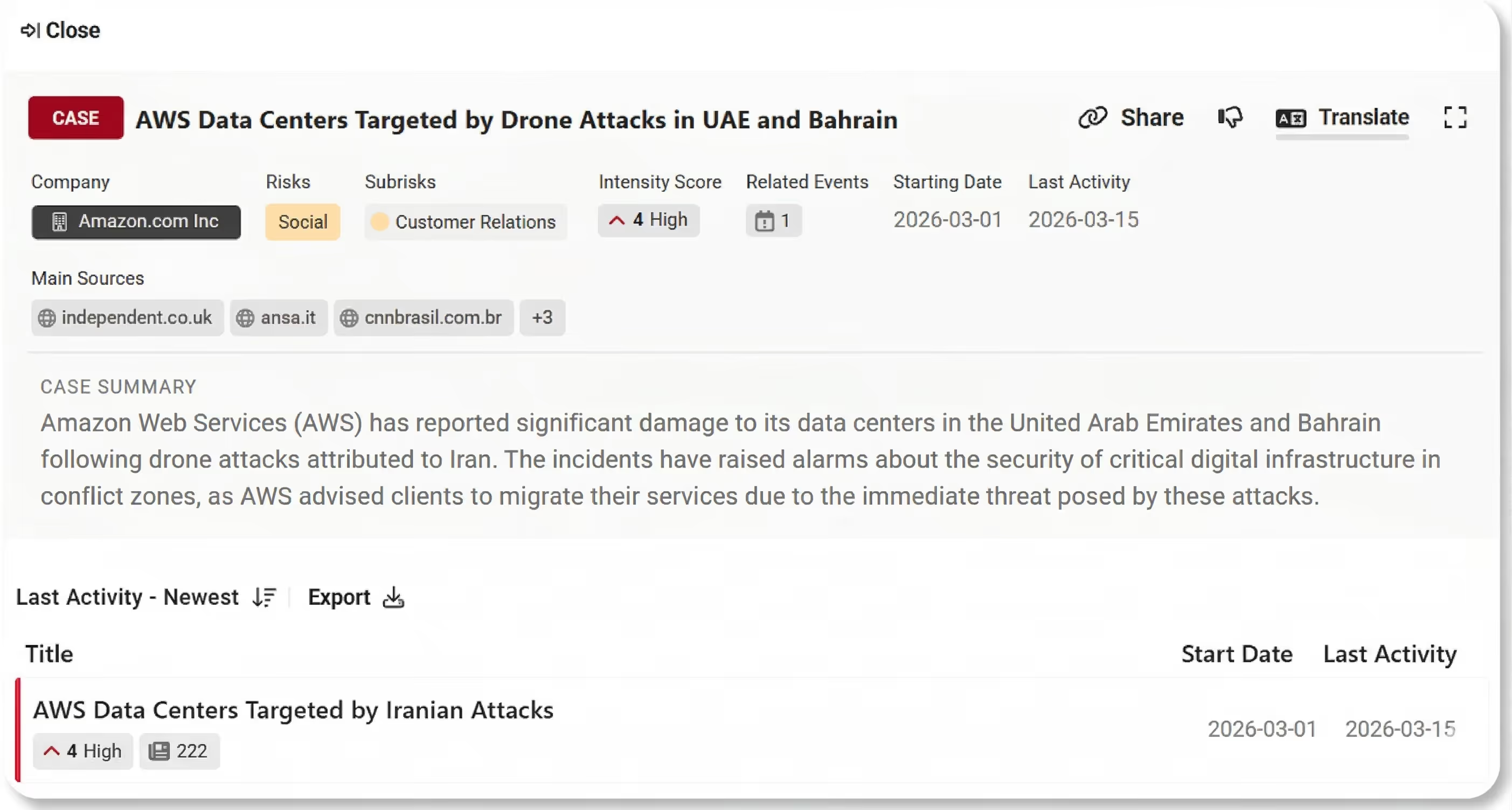

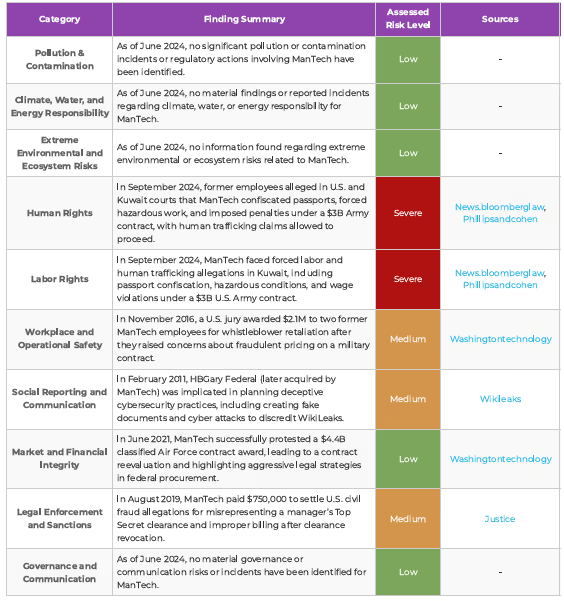

In the dashboard, a company appears as a single entity with its related cases listed beneath it. Each case includes a controversy summary, an ESG risk classification, and an intensity score, with related events nested underneath and the original source articles just a click away. A case that draws on hundreds of articles becomes a short, readable list instead of hundreds of separate incidents.

Every case is fully traceable. Analysts can drill from a case down to its events, and from any event to the articles that produced it. The time period is set from the top of the dashboard, so older incidents do not crowd the view when the focus is on recent activity.

Reducing Noise in Adverse Media Monitoring

In practice, those forty articles collapse into one event, and that event sits inside a single case that is still developing, caught early and drawn from sources most platforms never see.

Grouping articles into events removes duplication caused when many outlets cover the same incident. Grouping events into cases keeps a controversy intact as it develops, rather than scattering it across months of separate alerts. Because this runs across ten million documents a day in more than a hundred languages, it holds up even for controversies that start far from the mainstream press.

The result is a view where the numbers carry meaning, the direction of an issue is clear, and the underlying articles stay one click away for full validation.

.png)

-converti-depuis-png.avif)

-converti-depuis-png.avif)

.png)